-

Who We Are

- What We Do

Series: Some Macro ThoughtsThis is Not 2024

By Nohshad Shah

FRONT-END RATES…are inconsistent with cyclically sensitive areas of the equity markets and the forward outlook for US economic growth. Market pricing for the September FOMC shows a 65% chance of a 25bp cut with a total of 50bps still priced for 2025. This looks wrong to me…in the context of stocks which are at all-time-highs (and going higher)…the easiest financial conditions (FCI) we’ve seen in 3 years…an unemployment rate that is going down…and core inflation that remains elevated – with both a weak dollar and incoming tariffs posing a further risk to this. This paradox seems to be the result of some investors’ perception that we will have a replay of the 2024 playbook when the Fed cut 50bps in the Autumn…this time, pressured by a Trump Administration that seems hell-bent on getting policy rates lower. But the economic circumstances are not the same…going into the Sep’24 meeting, the u/e rate had risen steadily to 4.2% from lows of 3.4% in Apr’23 – since then we have flatlined in the 4.0-4.2% range with the most recent print showing a decline. Similarly, Initial Claims have largely been in the 200-250k range over the last year, still far from recessionary levels (350k+). In addition, Core PCE had moderated from above 3% to ~2.6% YoY going into last September’s meeting and given the starting point for policy rates, it’s clear that the Fed felt comfortable taking out some insurance against the potential for an accelerated downturn should it have transpired. Of course…since then the biggest change has been President Trump…and we can distil his policy priorities thus far into three – tariffs, immigration and fiscal. On tariffs, we seem to be heading to an effective tariff rate of ~16.5%…which though still impactful, should not cause a recession given the broader backdrop…however, it’s still likely to induce short-term inflation with potential implications for higher inflation expectations – something that Governor Goolsbee alluded to on Friday. Then on immigration, as discussed last week, the new Administration’s policies will likely curb net migration from above +1million towards zero (or even negative territory) having a dramatic impact on tightening supply in the labour market and therefore the unemployment rate (indeed, I have long made the argument that the u/e rate is heading lower, not higher). And finally, the President’s big, beautiful bill will have a +0.9% impact on 2026 GDP, materially altering the fiscal impulse that many would have anticipated at the start of the year. Surveying the landscape that I’ve just outlined, which central banker would want to cut rates?…let alone the 50bp cut that some in the market are looking for in September. It is true to say that spot inflation has moderated in recent months with Core PCE 3m Avg. at 0.14 MoM…however, it’s the FOMC’s job to look forward over the forecast horizon to estimate the impact of these policies on the economy…so the risk here is one of a hot economy, which could potentially spurn even greater inflation, beyond still above-target levels. Whilst there’s been much discussion of President Trump’s pressure on Fed Chair Powell to cut rates and some members like Governors Bowman and Waller calling for cuts…this is only to be expected given the politicized backdrop. Make no mistake, this is still Powell’s Fed…and will remain so for another 10 months. Given the current macroeconomic environment, I cannot see him cutting rates anytime soon. My sense is he has two priorities – to protect his legacy…which means not giving up the fight against inflation at the final hurdle – and to protect the institutional credibility of the Fed…which implies not acquiescing to political pressure. There’s even some discussion that he may remain on the FOMC after giving up the Chair…a topic he has been conspicuously quiet about. We shall see…but for the time being, fade the rate cut pricing in September.

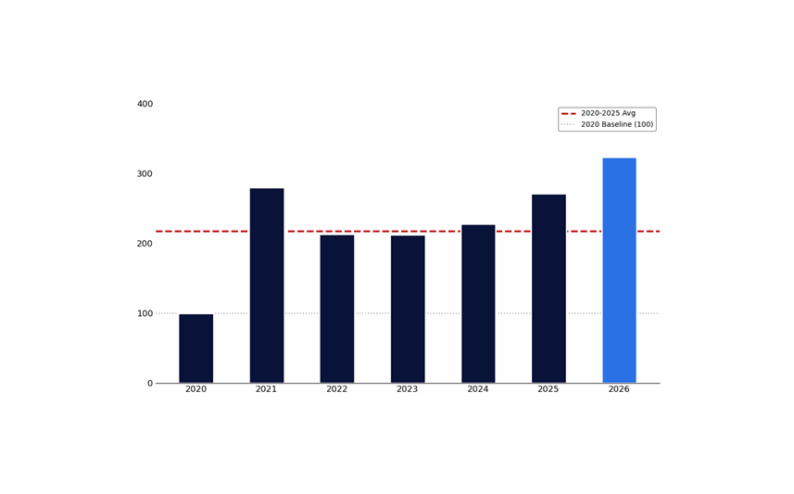

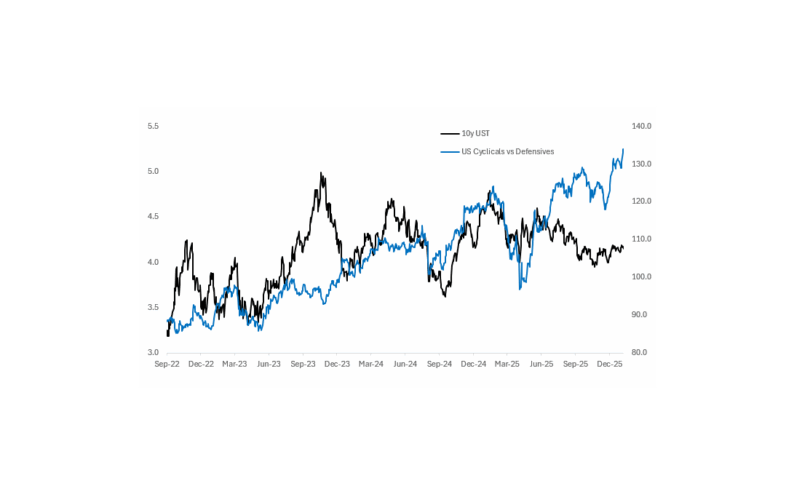

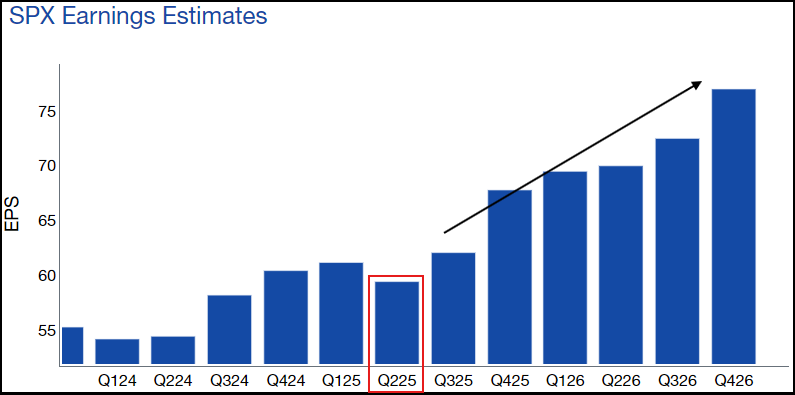

IN THE MEANTIME, THE ALWAYS-PRESCIENT EQUITY MARKETS CONTINUE TO FORGE AHEAD MAKING NEW HIGHS. As I’ve been flagging in this note for the last few months, conditions have been ripe for a melt-up in stocks as, one by one, tail risks have been reduced, FCI has eased, and the AI investment boom and expansionary fiscal policy come to the fore. Expectations for nominal growth are being revised up rapidly…bond yields remain controlled (for now)…which is essentially the perfect environment for stocks. This week saw important consumer bellwether Delta Airlines re-instate it’s 2025 profit outlook citing a stabilization in bookings and expectations of a strong summer travel season. This is in stark contrast to April, when Delta led a host of other airlines in withdrawing full year guidance due to economic uncertainty. In my mind, this represents an early signal for both Q2 earnings and the sentiment of US consumers which is rebounding sharply, consistent with much of the survey data we’ve seen in recent weeks. As a side note, the chart below plots Delta stock and 1y1y US swap – though clearly not causal, the strikingly high correlation affirms my view above about how front-end rates appear to be mispriced relative to cyclical equities. Speaking of earnings, Wall St consensus expects only a 4% Q2/Q2 YoY rise with reporting season beginning in earnest next week – that is a very sanguine outlook, somewhat justifiable given this period covers the “tariff tantrum” of April. But it also represents a very low bar for beats – something which I can see happening quite easily – the chart below shows how much of an outlier Q2 forecasts look. My sense is that if companies miss, the market will overlook it as backward looking…and if they beat, it provides further evidence that the outlook is rapidly improving and growth in earnings (especially with a post COVID lower cost base) can start to match the rally in prices. Remember, WATCH THE RIGHT TAIL.

Delta Airlines Share Price, USD 1y1y forward swap

Source: Bloomberg

Source: Haver, Bloomberg

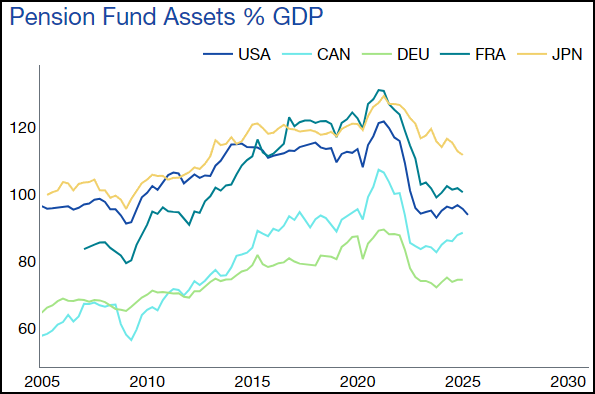

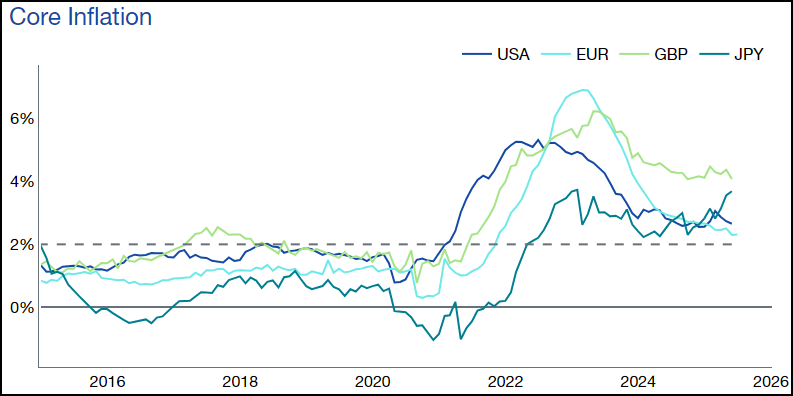

ZOOMING OUT, BOND MARKETS WILL REMAIN A CONCERN OVER THE MEDIUM TERM. The last few months have seen sharp spikes in 30y bond yields across all the major markets – US, EU, Japan, and UK. This represents a confluence of factors, namely that no central bank has gotten inflation fully under control (chart below)…most major economies are deploying expansionary fiscal policies regardless of deficits…whilst at the same time structural demand for long-dated fixed income assets is waning. Post COVID we have seen more retirement and withdrawal from the workforce out of choice, drawing down investments…if this trend continues, we could see a greater drop in pension savings (chart below)…the largest natural source of demand for 30y bonds. Treasury officials have responded to this challenge by shortening WAM (weighted average maturity), something we’ve seen most recently from the UK DMO and the US Treasury. Secretary Bessent has clearly stated that he has no desire to increase long-term debt issuance in a u-turn from his prior criticism of his predecessor Janet Yellen for issuing short-term debt. Whilst successful in the short-term, this is simply another form of financial repression, which will only create greater problems down the line…by shortening the debt profile, they are simply making the economy more exposed to the level of rates. This is a problem because when the next inflation shock hits – whether from an external shock like COVID or just an overheating economy – it will be a disaster for the public finances. In simplistic terms, nobody is fixing the roof whilst the sun is shining…exposing the house to a storm when it inevitably hits. The spikes in yields we have seen this year are warning shots…not to be ignored, in my experience. If governments continue to ignore these signals, they will ultimately pose a risk to financial stability (both bond and equity markets selling off sharply with risk parity most vulnerable) and fiscal sustainability (ballooning debt servicing requirements). Ultimately, it is only bond markets that can serve to police this situation…and whilst these are still warning rounds, they will eventually force the hand of governments and rein-in investor exuberance. Which brings me back to why I am less excited than the market on Fed rate cuts despite the pressure from President Trump…even a new dovish Fed Chair would be punished by higher long-end yields if they cut policy rates into a hot economy…which may be the straw that breaks the camel’s back in 2026. But for now…stay long stocks.

Source: Haver, OECD

Source: Bloomberg

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do