-

Who We Are

- What We Do

Series: Some Macro ThoughtsWaking Up to Affordability and Inflation

By Nohshad Shah

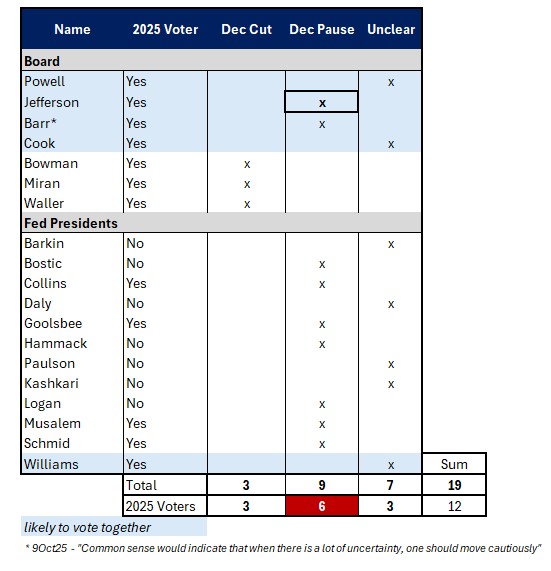

EQUITY MARKETS SLUMPED THIS WEEK AS INVESTORS GREW JITTERY ABOUT AI VALUATIONS AND GROWING QUESTION MARKS AROUND FURTHER RATE CUTS FROM THE FED. These two factors – and uncertainty around the economic outlook in the absence of data – have compounded to create an apprehensive backdrop. The market seems to be waking up to the magnitude of debt issuance required to fund ongoing AI capex…which is now estimated to be $600bn next year (up from ~$400bn in 2025), something which will have a sizeable impact on credit markets…both for hyperscaler names and beyond (with the crowding out effect). As my credit colleague Jeff Eason states, hyperscalers remain inelastic buyers of resources to achieve their AI build goals and are increasingly being seen as inelastic sellers of debt to fund this. This marks a dramatic shift in the balance sheet realities for mega cap tech firms…traditionally, these companies accumulated hundreds of billions in cash, which often ended up being used to fund share buybacks. But now, they are spending cash at a rapid rate on AI-related investments and issuing large sums of debt ($75bn in Sep and Oct for AI data centres)…with the speed of capex growth beginning to deplete excess free cash flow. The cost of debt funding remains relatively attractive…but investors are questioning the ROI from capex and scrutinizing business models – something which is starting to be reflected in differentiated credit and stock pricing. As I’ve said before, not every business will succeed in their AI ambitions…and this may well mark the beginning of the end of the ‘rising AI tide lifting all boats’. More importantly…there was a substantive shift in the Fed narrative this week – in the hawkish direction – which has been a tough pill to swallow for stock markets. As I mentioned in my last note, the primary driver of yields moving higher matters – higher rates due to higher nominal growth are very different from higher yields due to more restrictive policy. This week, the market focused on the latter…with Boston Fed President Susan Collins explicitly stating there should be a “high bar” for further easing and that the Fed should “keep policy rates at the current level for some time”, suggesting a prolonged pause even beyond December’s meeting. This followed Vice Chair Jefferson’s speech highlighting the need to “proceed slowly as we approach the neutral rate” which was “especially prudent because it is unclear how much official data we will have before our December meeting”…and WSJ’s Nick Timiraos’ article about December being a tossup. Jefferson’s speech seemed to be a nod to Chair Powell’s presser and I find it difficult to believe they would not be aligned in their messaging. Which means for December’s meeting we only have 3 voters firmly in the cut camp (Miran, Waller, Bowman)…against 6 in the hold camp (Musalem, Schmid, Collins, Goolsbee, Barr, Jefferson)…as well as 3 non-voting members on-hold: Hammack, Bostic and Logan. As my colleague Frank Flight flags, this leaves 8 out of 12 voters in favour of a hold (11 out of 19 FOMC). In my mind, the lack of economic data due to the US government shutdown has played a crucial role here…without official confirmation of a sharply slowing labour market, how can Fed officials be comfortable continuing to cut rates with inflation ~1% above target and the easiest financial conditions we have seen in years? The problem for stocks is that the shift in market expectations for rate cuts has come in the absence of data, not because of it…which implies a hawkish shift in the FOMC’s reaction function without a related positive adjustment to the economic outlook. Risk assets are uneasy about this. The best environment for equities is when the Fed is dovish and the economy remains strong (akin to what we’ve had recently…a lower real rates environment)…but now, we have a hawkish impulse in the absence of positive data, which is troubling for risk assets. The run-up in stocks has been driven by a combination of easy FCI and the AI story…markets are recalibrating on both…and if we continue to see rising real yields and tightening FCI (driven by a hawkish impulse), then we’re in for a rough ride.

Subjective assessment of how FOMC voters may lean at December’s meeting

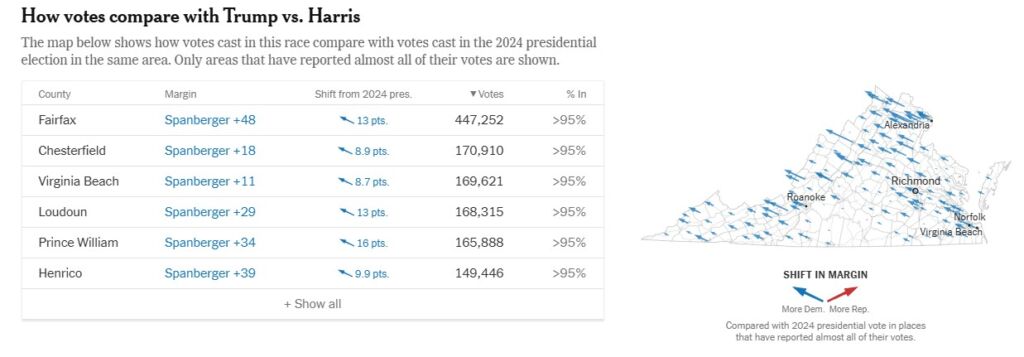

WHILST MARKETS HAVE BEEN WILLING TO IGNORE INFLATION, IT’S NOT LOST ON THE AMERICAN PUBLIC THAT WE’VE BEEN RUNNING ABOVE TARGET FOR NEARLY 5 YEARS. Public anxiety around the cost of living is high…reflected in both opinion polling and voting patterns. Much digital ink has been spilled on the policies associated with Zohran Mamdani, New York City’s Mayor-elect…but there’s no doubt that “affordability” was the decisive issue that won him the election. Whilst Mamdani’s campaign has had the most focus, Democrats also substantially outperformed with much more centrist candidates on the ballot in Virginia and New Hampshire…even with traditional, less high-profile campaigns. The results of these elections show a significant swing towards the Dems relative to the 2024 presidential margin – the statewide swing in Virginia was 9% and 8% in New Hampshire. This comes at a time when the Administration’s net approval ratings have declined to -18% according to The Economist’s approval tracker and a recent Reuters/Ipsos poll suggests that the most important factor for the 2026 midterm elections will be the cost of living, taking 40% of the vote. President Trump has taken note…and appears to be pivoting to focus on the affordability issue, most clearly highlighted by broad exemptions to reciprocal tariffs that are driving food inflation. By extension, it seems reasonable to assume that POTUS and Treasury Secretary Scott Bessent may be less dovish when it comes to setting monetary policy (and relatedly, pressuring the Fed) as we approach next year’s elections. The recent results also serve as a timely reminder to Fed policymakers that the public cares about inflation…and perhaps it’s not too far of a stretch to think that their most recent pivot might have been inspired by the re-emphasis of affordability in the political discourse…especially in the absence of economic data. As I’ve repeated many times in this note – underlying inflation is 2.75-3.0% on all of the Fed’s models – so there is little room for error should tariffs prove more durable…or the combined impact of fiscal and monetary stimulus in 2026 drive a classic wage-price inflation process if the US labour market picks back up in tandem with the cyclical growth outlook. Inflation is already in the psyche of US households. Markets and policymakers are awakening to inflation and affordability concerns.

Virginia 2025 Vote Swing vs 2024 Presidential Election

Source: NYT https://www.nytimes.com/interactive/2025/11/04/us/elections/results-virginia.html

THE PATH FORWARD FOR ASSET PRICES IS RELATIVELY COMPLEX. In the near term, the market will need to internalise the risk that the Powell Fed may be done with cutting rates, with the FOMC themselves perhaps forcing that conclusion ahead of the market becoming comfortable with the pathway due to lingering concerns over the incoming official data. This is the reality of a central bank that appears to be now placing a more equal weight on its inflation mandate rather than focusing single-mindedly on employment. Ultimately, I do expect the data to vindicate the Fed’s pivot, but the sequencing is going to be challenging. In the week ahead there are two key pivot points…the (likely-to-be-released) September employment report and NVIDIA earnings. If these two break in a growth friendly direction, it should be enough to put a floor under risk assets…but both have elevated uncertainty bands around them. Moreover, it’s important to acknowledge that risk assets have faced the additional headwind of a fairly significant liquidity drain from the combination of the government shutdown, TGA rebuild (from ~$300bn to $1tn in Oct), heavy bills issuance and ongoing QT. All these factors represent a private sector reserve drain, which has in turn reduced liquidity in the US financial system. As we approach the end of November, bills supply will ease somewhat…the TGA will be spent down towards the target balance…and QT will pause. Taken together, this should start to ease pressure in funding markets and may also provide some support to the more liquidity-sensitive elements of the risk assets complex (e.g. Bitcoin). Whilst the path ahead for equities is more complicated, to my mind the more dislocated asset is US rates, which continue to look rich versus my view of the cyclical outlook, inflation risks and the Fed’s refreshed monetary policy perspective.

Nasdaq, Bitcoin; vertical line start of US government shutdown

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/

Explore

Market Insights - What We Do