By Nohshad Shah

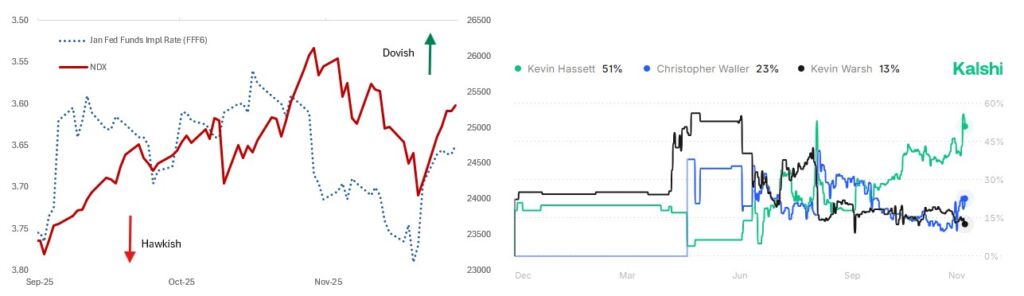

THIS WEEK’S (HOLIDAY-SHORTENED) PRICE ACTION WAS A REMINDER OF THE IMPORTANCE OF MONETARY POLICY IN DETERMINING SHORT-TERM GYRATIONS IN ASSET PRICES. Markets have become accustomed to supportive policy – both monetary and fiscal – with deviations from this norm being greeted with a nervy response…the ~8% drop in NDX from the all-time highs was predicated on (what seemed like) a hawkish pivot from Fed Chair Powell at last month’s FOMC presser, introducing uncertainty into the outcome of December’s meeting. Alas, NY Fed President John Williams’ dovish speech on 21st November has moved the probability of a rate cut back to 85% and stock markets have rallied almost all the way back. Beyond the moral hazard this engenders, it emphasizes the significance of the next pick for Chairman of the Federal Reserve. Reports suggest NEC Director Kevin Hassett has emerged as the leading candidate with Kalshi odds rising to 51% on the news, well above the nearest competitor (Waller, 23%). His front-runner status is attributed to both loyalty to President Trump and his broader reputation as a proponent of loose monetary policy. Markets currently expect the next Fed Chair to deliver more in terms of rate cuts beyond the remainder of Powell’s term with any incremental hawkishness from the current FOMC causing a re-distribution of cut premium into the next Chair’s term. Terminal rates at 3% are priced for a relatively dovish outcome already…in the context of a strong forward growth and inflation outlook in 2026. The market seems broadly comfortable with the idea of a dovish Fed chair – the dollar has stabilized; the yield curve is rangebound; 30y UST yields are anchored well below 5%; 10y breakevens are at the lower end of their range (2.25%). This makes sense…there is a credible argument for cutting rates at this juncture, which centres on the fact that there are real concerns about the health of the US labour market. Of course, one can argue the merits of further rate cuts – as well as the relative risks between the employment and inflation sides of the mandate – but the discussion is credibly grounded. In other words, the current context means that the immediate prescription is the same, regardless of the lean or credibility of the next Fed Chair. However, should the macro data start skewing towards a reflationary environment in which it’s clear that rate cuts are not warranted, then my sense is the market will start to focus on the risks associated with a loss of central bank credibility, namely a de-anchoring of inflation expectations leading to higher long end rates and a weaker currency. On paper, the combination of a dovish Fed chair and a reflationary macro outlook would still be a bullish environment for equities…but the reason why central bank credibility is so crucial is that history tells us that when credibility is lost, an over-correction is required to bring inflation back to target, likely forcing a much more severe recession than would otherwise transpire. A central bank with strong credibility (which the Fed no doubt has) needs only to administer marginal adjustments to generate its desired outcomes. This is not the case when that credibility is lost – larger moves are required to re-assert authority. Equity markets may struggle to price that initially, but a loss of central bank credibility is ultimately negative for stocks in the long term…so something which investors should be cognizant of as we approach the end of Chair Powell’s term. Whoever is the next Fed Chair must retain the institution’s inflation-fighting credentials…otherwise the consequences for global markets and the population at large could be severe.

Source: Bloomberg, Citadel Securities, Kalshi

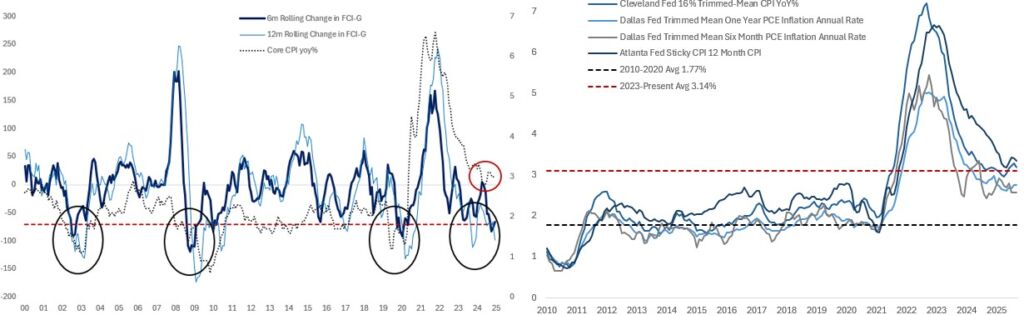

SO, WILL THE 2026 OUTLOOK PROVE A CHALLENGE TO THE DOVISH MONETARY POLICY NARRATIVE? I’ve been bullish on the forward growth outlook for some time, and it’s worth framing this in the context of financial conditions and the fiscal impulse. Smoothing through the average change over the last four quarters in FCI-G (the Fed’s measure of financial conditions) suggests FCI will add roughly 50-65bp to quarterly annualised growth next year…which comes alongside a fiscal impulse that implies an additional 50-100bp tailwind next year. Conservatively, this means ~100bps of stimulus relative to trend growth in 2026. Long-term estimates of US trend growth centre on 1.9-2.0%, but with a more restrictive immigration policy it’s reasonable to think this is around 1.75% for 2026…which would suggest real GDP growth next year in the region of 2.75% (a bottom-up economic forecast would add in various offsets from tariffs and uncertainty). A survey from the National Association for Business Economics of 42 professional forecasters suggests “the median outlook was for [US] growth of 2%, up from 1.8% in a prior October survey and in contrast to a growth rate of only 1.3% projected in June”. Consensus expectations of economic growth are clearly moving in the right direction, but I continue to think they’re behind the curve with respect to the improvement in the outlook since April’s tariff shock, especially given the performance of risk assets. The FOMC dot plot assumes 2.6% inflation (core and headline PCE) in 2026, which still implies a nominal GDP outlook of 5.35% (2.60%+2.75%). But…with stalled progress on underlying inflation which sits ~1% above the Fed’s target, and a 100bp positive output gap, I struggle to see a disinflationary impulse in the pipeline next year. If my outlook prevails, then we could see a world in which inflation simply stalls (or moves higher) and ends up around 3.0%. The consequence of this is 5.75% nominal GDP…exactly the kind of environment that would cause markets to test an overly-dovish Fed…an inability to price rate hikes (or indeed more rate cuts below 3%) in the face of higher growth and inflation would likely see the market find an alternative equilibrium in financial conditions – namely some combination of higher 10y yields and lower equities – to offset the inappropriate monetary policy stance. It’s difficult to weigh how much FCI tightening would be required should the market decide that Fed policy had become non-credible and the specific sequencing in stock / bond correlations. Indeed, it’s very possible that the initial move in risk assets would be positive as markets perceive pro-cyclical easing as good for forward earnings prospects…but that would simply mean that rates ultimately need to sell off more to offset this. Of course, any rapid move higher in bond yields would quickly become a headwind to stocks as 10y UST yields approach 4.5-5%. Furthermore, equity markets would need to account for the fatter left-hand tail of a more sizeable future policy tightening being required to get inflation back under control, should inflation expectations become truly de-anchored. In sum, it’s not clear to me that financial conditions will continue to ease should my 2026 outlook become consensus, regardless of how much the next Fed chair tries to ease. Markets – as ever – can act as a powerful speed brake to poor policy decisions.

Financial Conditions (FCI-G), Inflation measures

Source: Fed, Bloomberg, Citadel Securities

FOR ASSET PRICES, THE PATH FORWARD REMAINS BALANCED. A positive growth outlook, combined with easy monetary and fiscal policy and (still) loose financial conditions implies a supportive backdrop for stocks. But the recent volatility is here to stay – both because of increased uncertainty around the monetary policy response function and concerns around extended valuations in the AI sector. As I’ve mentioned in recent weeks, investors are becoming much more discerning around the extent of debt issuance from some hyperscalers…and the competition for leadership in AI innovation is only getting fiercer by the day – as evidenced by this week’s news on the race for chip dominance between Google and NVIDIA…with the market valuation gap tightening sharply. It will be the job of investors to differentiate the winners from the losers…the phase of the ‘rising AI tide lifting all boats’ is over. The normalisation of positive growth expectations since April’s tariff shock has meant volatility in most asset markets has remained subdued…something which I expected. As we look forward, the risks on the horizon are…i) reflationary growth with rising inflation (aka “affordability” in politico-speak)…ii) extended labour market weakness leading to recession…and iii) a substantial unwind of AI optimism, which causes a dramatic shift in the outlook. It feels like the tails are getting fatter, which means as markets price a wider range of outcomes, implied volatility should rise.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/