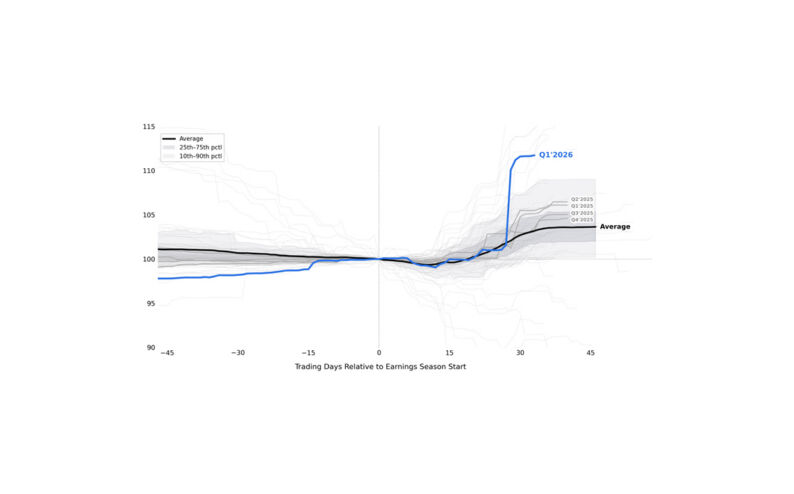

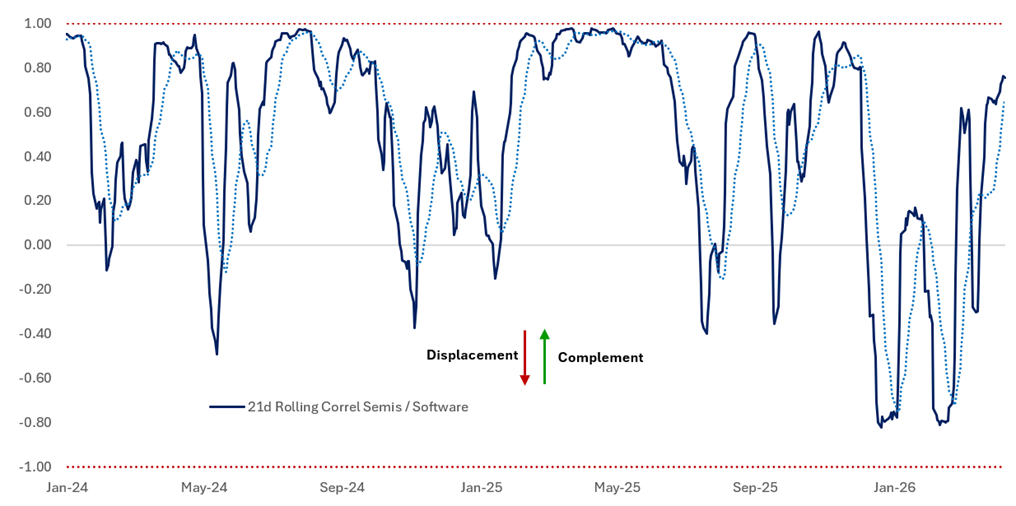

EQUITY MARKETS HAVE BEEN THE LEADING INDICATOR THROUGHOUT THE IRAN CONFLICT…sending a much cleaner signal about its likely duration, escalatory path, and ultimately the potential impact on the US growth outlook. The strong rally reflects several factors – not all of which are directly tied to the war. First, the de-escalation pathway I flagged in my note of 4th April created a clear catalyst for equities to shift their focus from the absolute level of geopolitical stress to the second derivative of that stress impulse. Once investors became comfortable that this stress impulse was no longer worsening, and that the worst-case tail scenario was unlikely to materialise, stocks were able to extend their time horizon and rally despite the war remaining unresolved. Second, technicals mattered…the initial phase of the conflict was enough to push net exposure down significantly, with the institutional community well hedged, likely through index gamma. That meant the initial relief rally was compounded by downside-hedge and index-short unwinds, taking nets back up. Third, earnings have been robust…beat rates remain elevated and price reactions have skewed positive: 84% of companies have beaten on EPS, 80% on revenue, and 49% of names have traded higher post-print. Finally, the market has refocused on the AI theme with expectations for capex spend now reaching ~$750bn, roughly 2.5% of US GDP. Capex of this magnitude is fundamentally supportive of economic activity, even if not fully captured in GDP accounting (semiconductors are intermediate goods, so do not show up directly in final-value GDP). This has been reflected primarily in semiconductor stocks with the sector up ~40% in the last month alone. More importantly, this phase of the AI cycle looks much more like a healthy macro impulse beneath the surface…the market appears to be moving away from treating AI primarily as a displacement narrative, where legacy software and labour receive a smaller slice of the pie. Instead, it is increasingly processing it as a once-in-a-generation capex cycle that can provide a near-term uplift to growth, with the potential to raise productivity and economic capacity over time – something which my colleague Frank Flight has written about extensively (Feb note, April note) arguing both that the market was underestimating the compute intensity of more complex AI technology, and that the fixed-pie / displacement narrative was the wrong focus. The 21d realised correlation between semis and software has flipped from -0.8 (when the market was pricing AI displacement) to +0.75, reflecting a more complementary relationship between AI and broader economic activity. This is a much healthier paradigm.

Source: Bloomberg, Citadel Securities

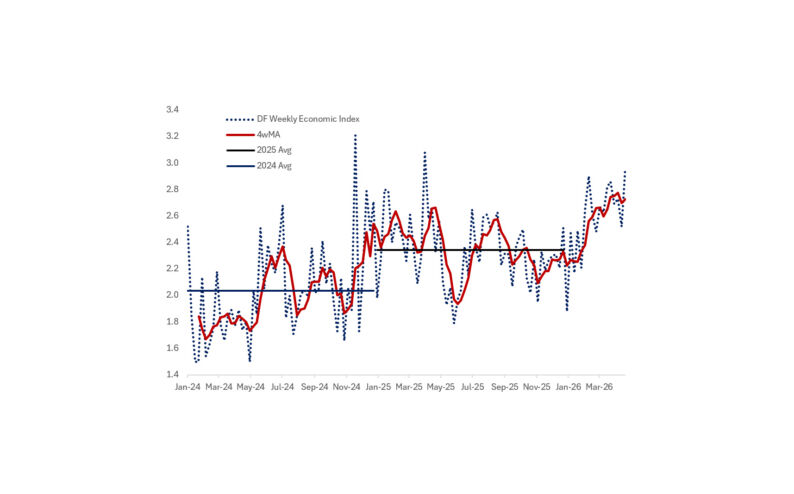

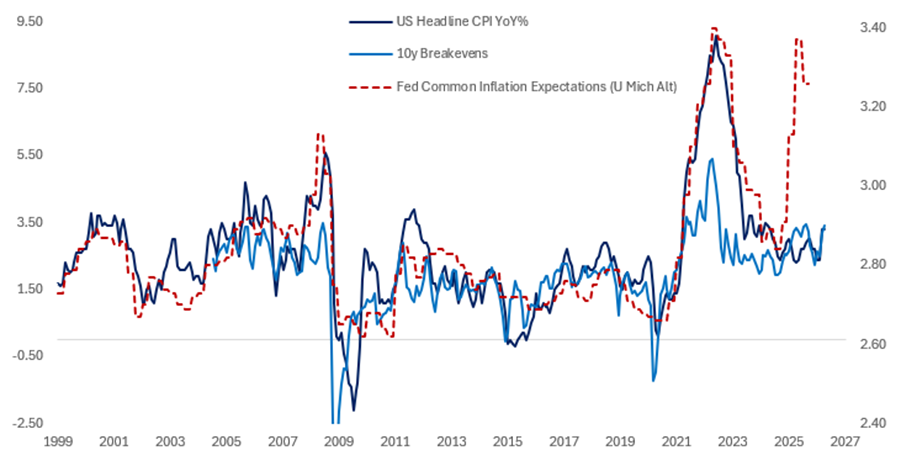

AS THE AI DISPLACEMENT NARRATIVE HAS EVOLVED, SO TOO HAS THE MARKET’S PRIMARY SOURCE OF CONCERN. I have been of the view that “everyone is short the inflation tail risk” and that is now truer than ever. The rally in risk assets has pushed broad financial conditions to levels that are now easier than pre-conflict, reflecting a highly accommodative environment for growth. This is despite spot oil prices ~50% higher than their pre-conflict level and 1-year inflation swaps being 75bp higher, implying headline inflation of around 3.2%. Furthermore, cyclicals versus defensives, the market’s growth proxy, is ~5% higher YTD, having rallied 15% from the lows of the Iran war. This all suggests that markets now see BOTH more growth and more inflation than they did pre-conflict. This also comes alongside increasingly clear evidence of stable labour markets with a pick-up in hiring across NFP (+115k this month, +185k last month, and a 6m avg. of +55k running around or above the breakeven rate), an ongoing improvement in ADP and Revelio alternative hiring data, a stabilisation in the JOLTS quit rate (2%), and continued very low initial claims (4wk avg. 203k). In sum, what we’re left with is a strong US growth outlook buttressed by easy FCI and a once-in-a-generation AI capex boom…plus labour market fundamentals that are improving, but with the context of much reduced immigration…which boosts the probability of second-round effects on core inflation from the conflict-induced headline shock. This is the true risk for the Fed and markets. “Do not bet against the US economy” remains my core tenet of global macro investing…and yet again the resilience shown by US growth and consumption has confounded expectations. For now, the Fed is not standing in the way of this…

Source: UMich, Bloomberg, Citadel Securities

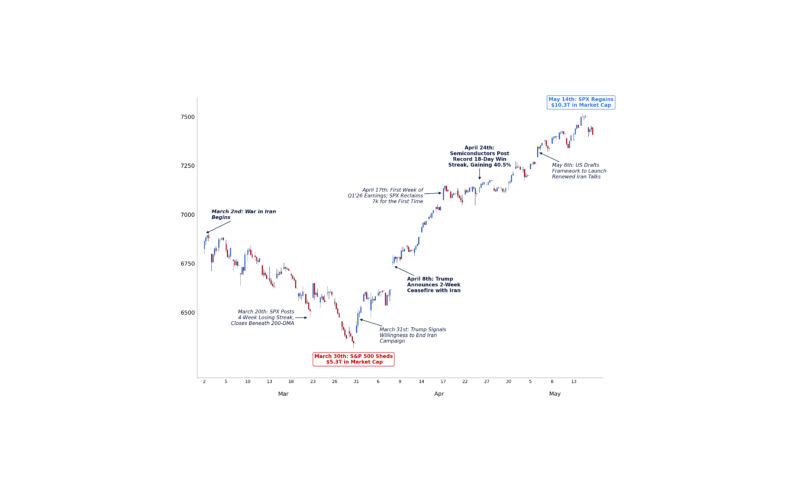

THIS WEEK’S FLARE UP IN THE MIDDLE EAST WAS A REMINDER THAT THE CONFLICT IS NOT QUITE OVER. The exchange of fire involved strikes against an Iranian oil tanker, attacks on US naval destroyers and drone and missiles salvos directed at the UAE. Whilst troubling for the nascent ceasefire, the comments from both President Trump calling it a “love tap” insisting that the ceasefire remains in place…and from President Pezeshkian that Iran remains ready to negotiate despite “mistrust”…suggest that we are still moving towards some form of interim negotiated settlement. As I’ve stated for the last five weeks, my firm belief is that President Trump is keen to move on from this war…and his measured response to this rise in hostilities – even compared to just a couple weeks ago – confirms in my mind that we’re on track to re-open the Strait of Hormuz soon with a combination of sanctions relief for Iran (and release of some frozen assets), a potential cap on uranium enrichment, and a conditional cessation of hostilities on all fronts with perhaps soft guarantees against a resumption of attacks. The current status quo cannot persist for much longer, and whilst we could certainly see another round of kinetic activity, the balance of probabilities lies with an agreement, rather than a full-scale resumption of war – especially in the context of the upcoming Trump-Xi summit scheduled for 14-15 May. One shouldn’t underestimate the importance of this gathering between the world’s only superpowers and the potential it has to reset US-China relations. Both Presidents will not want this conflict to overshadow broader discussions on trade and rare earths. If anything, this week’s events have accelerated timelines. Stepping back, the long-term consequences from this war are likely to be profound… higher geopolitical risk premia, more expensive energy security, weaker confidence in global trade, and persistent pressure on food-importing countries will be felt across the globe for some time. International relations, even amongst NATO allies, are ruptured…and alliances in the middle east (c.f. Saudi and UAE) look set to re-align meaningfully. The disruption in energy markets puts even greater emphasis on stockpiling, investment in renewables/nuclear power and friend-shoring broader supply chains…and even the current pain is uneven: energy importers like India, Korea, Japan, Europe, and parts of Africa are suffering much more than oil exporters. The burden from the impact on fertiliser and food, whilst not meaningful in the West, falls hardest on poorer food and fuel importing countries. Higher fertiliser costs reduce application rates, lowering yields months later and higher diesel and freight costs raise farm-to-market costs meaning second-round food inflation could persist even after oil stabilises. The bottom line is that whilst the aim of nuclear disarmament in Iran may be a worthy goal, the ramifications of this war are far-reaching and will be felt unevenly across the globe, with substantive shifts in alliances that have the potential to change the world order.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/