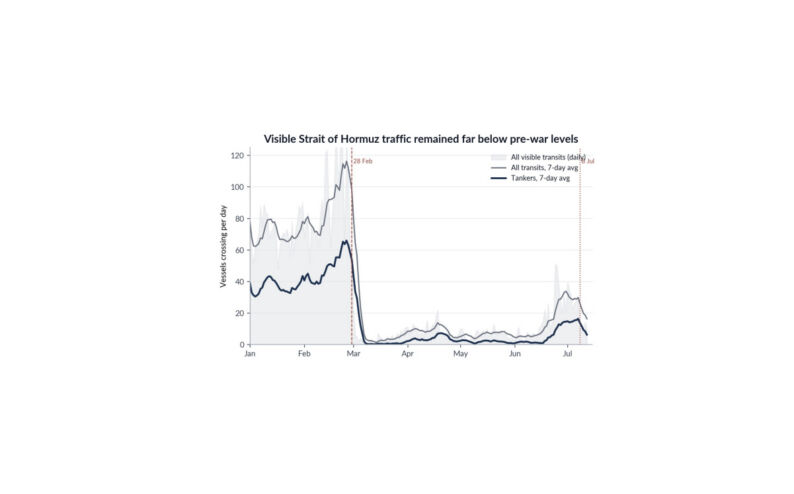

RISK MARKETS CONTINUE TO TAKE COMFORT IN THE CONTOURS OF A RESOLUTION TO THE WAR IN IRAN. Since my note of 4th April predicting a shift in the trajectory of this conflict, NDX has rallied 13% as markets have come to accept that the extreme tail-risk scenarios have receded. Despite the failure to reach an agreement thus far, it remains clear in my mind that both sides are wilfully engaging to reach a negotiated settlement – the cost of further escalation for both Iran and the US is likely too great to bear. Having stated that he’s largely achieved his objectives, President Trump seems keen to move on to domestic priorities, with only 192 days left until what will be a tricky midterm election season for the GOP. Affordability, including the recent rise in gasoline prices, will require some attention in the minds of voters. Equally, having survived external regime change, what remains of the Iranian leadership will want to rebuild their country and economy, so as not to have to face-down internally driven change – a risk with a domestic population having faced heavy bombardment for the first time since the 1980s. In simple terms, the next stage of kinetic conflict involving US troop deployment, further damage to energy infrastructure and risks to water desalination plants (the lifeblood of GCC countries) is a step too far and would cause catastrophic damage to the global economy with little further gain – the Iranian regime would still survive, as would whatever nuclear capabilities it retains. Moreover, China’s incentives are aligned for a resolution…whilst it has built substantial stockpiles of oil which provide short-term resilience, it will not be immune to persistent disruption in energy prices…and perhaps more importantly, a global demand shock would further expose its export-orientated growth model (at the same time as raising domestic input and shipping costs). Both superpowers are aligned here…and President Trump’s commitment to a prolonged ceasefire ensures that bombs will not fall and suggests we are drawing closer to a conclusion. What does that look like? Most likely a “JCPOA-minus” deal (though I doubt anyone will call it that)…with Iran agreeing to partial nuclear restraints (pausing enrichment above a certain level ~60%), avoiding further expansion of advanced centrifuges and allowing some IAEA monitoring. In return, the US and partners would provide targeted, reversible sanctions relief…for example, allowing limited oil exports, access to some frozen funds, or humanitarian channels. Importantly, a deal would likely avoid big political commitments (senate treaty, full sanctions unwind) and come in the form of letters of understanding with in-built confidence building steps like maritime de-mining. Ultimately, it will be less of a comprehensive agreement and more a freezing arrangement designed to buy time, reduce immediate escalation risk, and stabilise oil markets without resolving the underlying dispute. This is enough for markets and investors who are squarely focused on the reopening of the Strait of Hormuz.

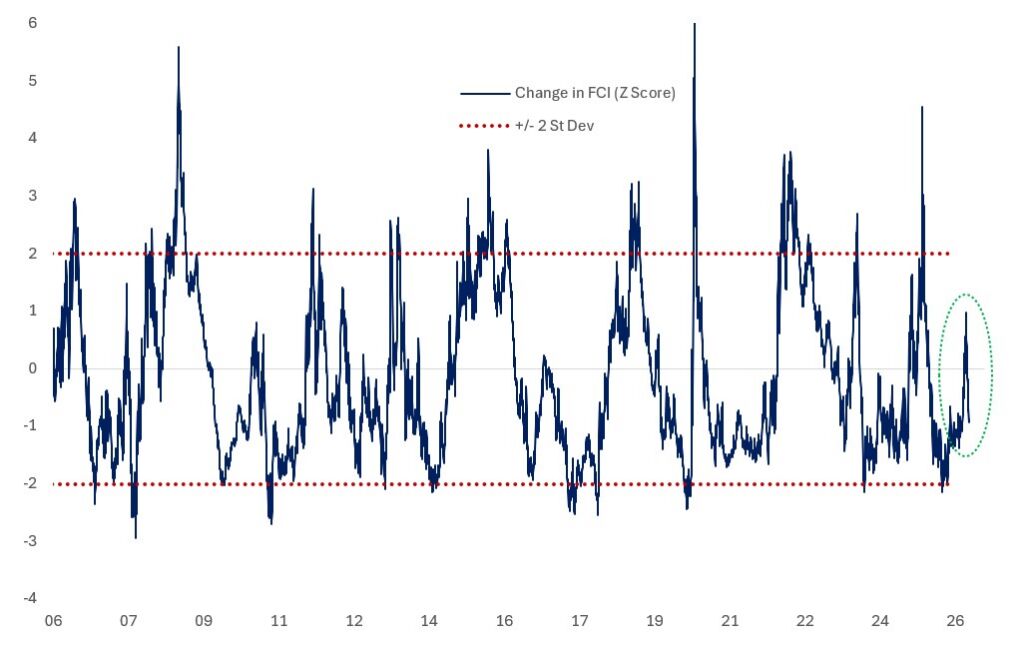

WHAT DOES THIS MEAN FOR CENTRAL BANKS? My baseline view remains the same, that they will likely under-deliver the forwards…but the hike premium may persist for some time until the Strait reopens fully. Communication from Fed speakers, most prominently Governor Waller, skew to on-hold, but the BOE and ECB path is more complicated. The April meetings are likely to be holds, meaning that we have until June to see the Strait reopen before central banks are pushed into delivering some tightening. My sense is the bar for the ECB to hike in June is much lower than for the BOE…not just because the policy rate is lower…but also because the missives from the MPC have suggested markets are pricing too much whereas the ECB have been flagging risks of hikes. Should a hike indeed be delivered, then the term structure of the front end will have to adjust to reflect a greater probability distribution of a series of upward moves given central banks rarely make a singular 25bp adjustment. As a reminder, the scenario of the ECB hiking while the Fed is on hold is extremely rare. One must go all the way back to 2011, in the aftermath of the GFC, when Trichet raised rates twice while the Fed remained at the zero lower bound – moves widely seen as a policy mistake, tightening into a fragile recovery. Incoming President Mario Draghi rightly reversed course by the end of the year. One of the more concerning dynamics for the inflation process is that the performance of equity markets has pushed FCI back to much easier levels. At the point of peak stress, changes in asset prices implied FCI tightening was likely to detract roughly 75bp from 2026 US GDP growth vs pre-conflict…that impact has now largely evaporated. This offsets some of the negative growth implications and hence implies somewhat higher risks of second round effects onto core inflation. Nowhere is that truer than in the US, where the underlying inflation process was already quite volatile and core has been accelerating in recent months. The valuation structure of the US front end is underpinned by the idea that Kevin Warsh will be dovish. That is a fragile equilibrium given the current backdrop, where even Scott Bessent now acknowledges near term rate cuts are inappropriate, having previously been calling for the Fed to move rates lower.

Change in US Financial Conditions

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

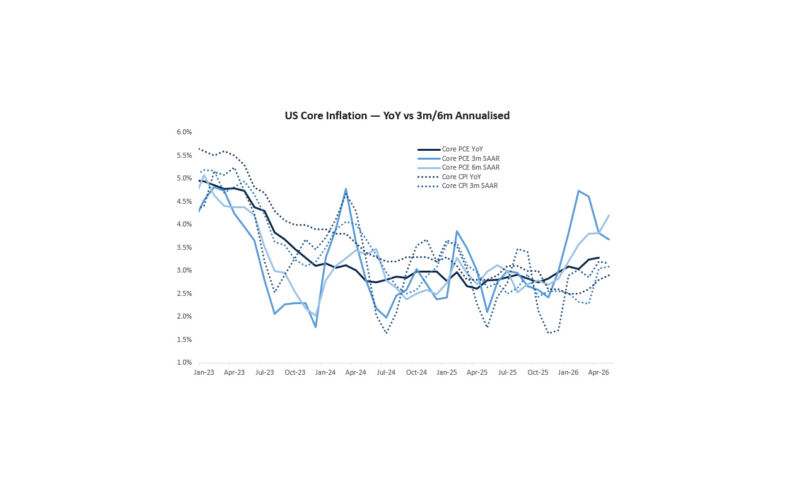

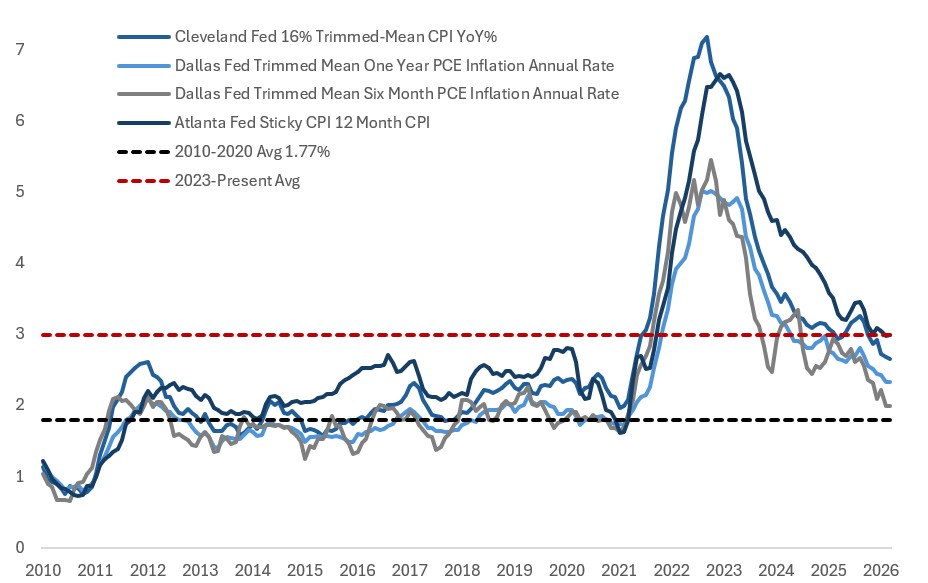

FOLLOWING NEWS THAT THE DOJ IS DROPPING THE INVESTIGATION INTO CHAIR POWELL, I EXPECT KEVIN WARSH’S CONFIRMATION TO BE IMMINENT…so his Senate hearings are worth considering. I’d highlight four relevant takeaways. First, he argued that a path for rate cuts existed via the productivity channel. His argument is grounded in the idea that productivity gains from AI will boost the supply side of the economy, generating disinflationary pressure. Second, he implied a preference to emphasise alternative measures of inflation, such as trimmed means and pushed back on the idea that tariffs had driven up inflation. Third, he suggested that the Fed should look to reduce the size of its balance sheet, although his framing implied that this would be a long process that would be communicated well ahead of time. Finally…he pushed back on the concept of forward guidance, suggesting that he will communicate policy intensions less frequently. For markets, this is largely in line with expectations and offers little imminent challenge to current policy pricing, mostly because the energy shock will dominate any near-term disinflation from AI, and various FOMC speakers have already opposed the idea that AI disinflation can be relied upon for making near term policy decisions. I agree with my colleague Frank Flight that in the first-order AI is likely inflationary, in the context of a once-in-a-generation capex boom with the backdrop of easy financial conditions and pro-cyclical fiscal stimulus…combined with an immigration-driven decline in labour supply weighing on trend growth…and tariffs creating a vulnerable starting point. Moreover, there are risks that if Warsh pushes the FOMC to focus on underlying inflation that the Fed may be too slow to react to a shift in inflationary pressure…inflections generally appear in the tails of the inflation distribution…exactly what gets missed by trimmed mean measures. If one averages across the trimmed inflation/sticky CPI measures from the Dallas, Atlanta and Cleveland Fed, they are running at 2.7%, about 1% above their pre-pandemic average…although in recently months they have conveniently trended lower despite traditionally measured core inflation picking up. Warsh is picking a measure of inflation that suits him, and that directly contradicts his criticism of the Fed’s slow response to the pandemic inflation episode, which he this week characterised as the greatest policy error in 40-50yrs.

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

WHAT ABOUT ASSET PRICES? Forward-looking equity markets have taken the view that if the implications of this crisis don’t affect future earnings, it doesn’t matter. Q1 beats so far have been meaningful with financials leading the way (the big six US banks delivered ~$50bn profits)…and as we head into big tech earnings week, my colleague Scott Rubner notes that valuations remain attractive with the S&P 500 Information Technology forward P/E sitting near its 10-year average and below the 5-year average. An environment of easing financial conditions combined with robust earnings growth should be supportive for continued equity market performance…especially in the absence of any imminent hawkish tilt from the Fed whilst they await clarity on the persistence of pass-through to inflation expectations and core inflation. Bond markets, as ever, remain concerned about the spot outlook and are caught between inflationary risks and concerns around demand destruction from the hit to consumer sentiment. As mentioned last week, my view is that we continue to be in an environment where both stocks and bonds can rally together…at least for now.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/