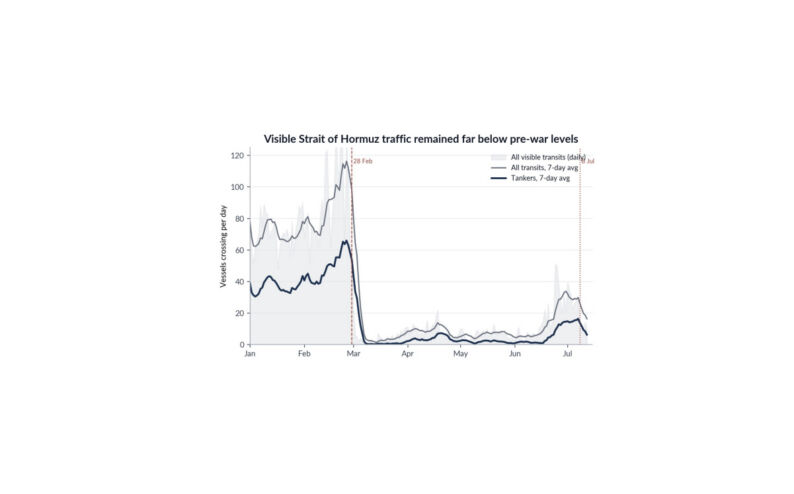

THE RE-ESCALATION WITH IRAN…appears to reflect the fragility of negotiations and the intractable positions on the key unresolved issues, culminating in attacks on commercial vessels in the Strait, including an LNG tanker and oil tankers. This, in turn, prompted the US to strike more than 80 Iranian targets, including assets in and near the Strait, revoke the waiver on Iranian oil sales, launch subsequent strikes on Wednesday evening, and led President Trump to declare the ceasefire over. This kinetic re-engagement likely stems from unyielding positions on the critical issues in the negotiations…I argued at the time that the MOU lacked substance on control over the Strait of Hormuz (paragraph 5) and denuclearisation; those issues are now resurfacing. At the time of the MOU, the prospect of even a partial normalisation of energy flows through the Strait was enough for the market, given how much risk premium was still embedded in energy futures. However, the precipitous decline in oil prices since May, driven by a quicker-than-expected rebound in tanker traffic and estimated Persian Gulf flows (h/t Frank Flight), has likely raised the bar for how much bad news the market can overlook. That helps explain why the earlier flare-ups were largely faded, while the events of this week were enough to drive Brent briefly back toward, and at points above, $80/bbl. My sense is that markets are underestimating the risk that Iran digs in on the two key issues of control over the Strait and maintaining a nuclear program, mainly because its ability to assert asymmetric leverage by disrupting the Strait has now been proven. As a result, these tit-for-tat kinetic frictions may steadily climb the escalatory ladder, especially given President Trump’s clear frustration in dealing with the Iranian regime. This should raise the floor on oil prices over the next few months, as markets naturally embed more risk premium, but also have to reconcile with the idea that flow through the Strait of Hormuz may now run permanently below pre-war levels – given elevated crossing risks – unless the US administration is willing to capitulate on Iran controlling the Strait and maintaining its nuclear program…two issues I doubt anyone in DC will find acceptable. The US decision to revoke the waiver on Iranian oil purchases matters because it removes a channel that had provided Tehran with meaningful financial relief by allowing it to monetise energy exports. But that leverage has limits…Iran may have constrained funds and degraded military infrastructure to re-escalate directly against the US, but it still retains comparatively low-cost ways to impose pain: disrupting traffic through the Strait or using cheap drones to threaten GCC energy infrastructure.

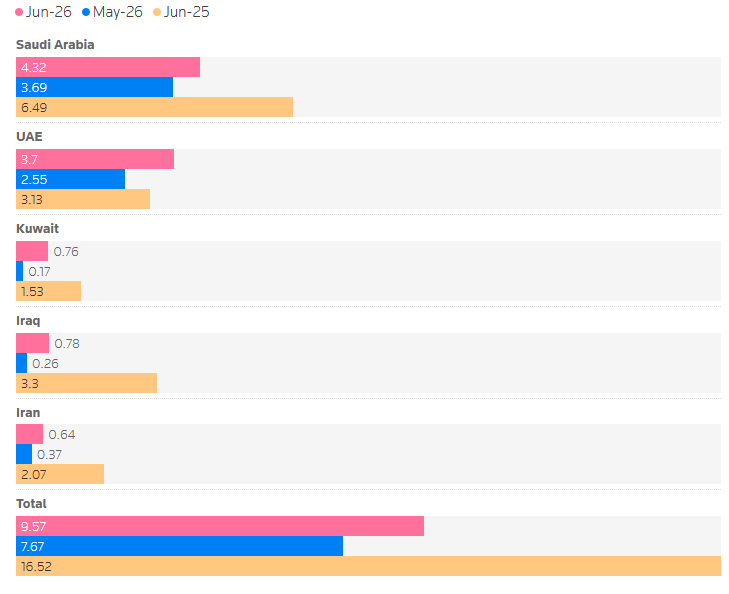

Gulf Oil Exports: Crude and Condensate Exports

Source: https://www.reuters.com/business/energy/gulf-oil-exports-jump-june-record-uae-flows-2026-07-03/

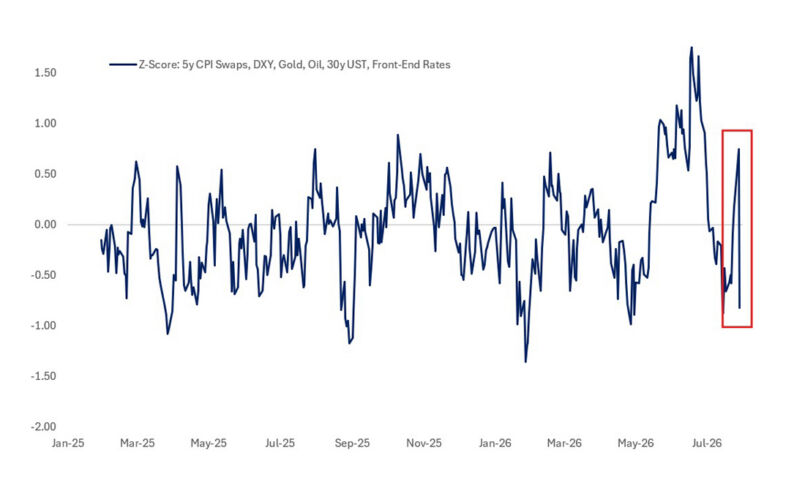

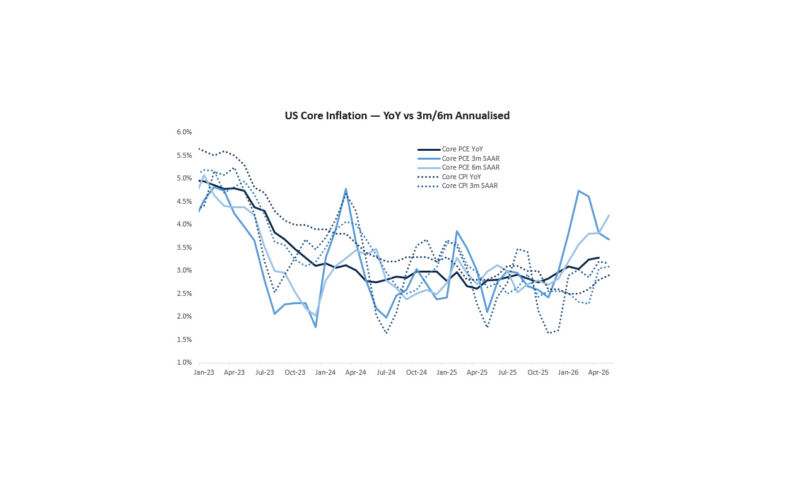

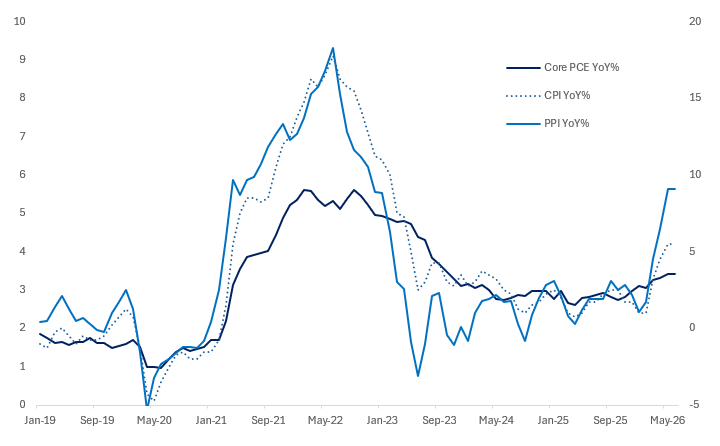

THE FORWARD PATH FOR FINANCIAL CONDITIONS LOOKS SKEWED TOWARD TIGHTENING…either because risk assets come lower of their own accord or because the Fed is forced to tighten policy in response to higher oil prices and renewed inflation risks. The key point is that this Middle East re-escalation is hitting a market that looks more vulnerable than it did at the start of the war. The AI theme…and semis in particular…is now pricing a much more optimistic scenario, which means the ability of semis to support broader risk sentiment through geopolitical tension may be more limited this time around. That matters even more given the technical backdrop in tech…the Nasdaq is trading right around its 50d MA, with a 7.5% gap down to the 100d MA, while the KOSPI is down 20% from its highs. At the same time, higher oil prices raise the risk that central banks turn more hawkish again, particularly if the oil shock proves more durable than it appeared a couple of weeks ago. Chair Warsh’s first meeting was a clear shock to a market that had assumed the Fed was unwilling to tighten, and markets still seem too relaxed about the risk of a July hike, especially given that Warsh went to great lengths to emphasise that he would not be providing forward guidance. The speed with which the market has been able to price hikes back into the European and UK front end looks increasingly at odds with its resistance to engage with the idea that the Fed could hike twice over the next two meetings…something that does not sound unreasonable from my vantage point, given the renewed focus on the inflation mandate and a core inflation profile that looks likely to sit around 3% for the rest of the year. In sum, this leaves me thinking that the risk asset backdrop is less about whether geopolitical shocks can be ignored, and more about whether markets are underpricing the likelihood that financial conditions tighten from here.

US Inflation

Source: Bloomberg, Citadel Securities

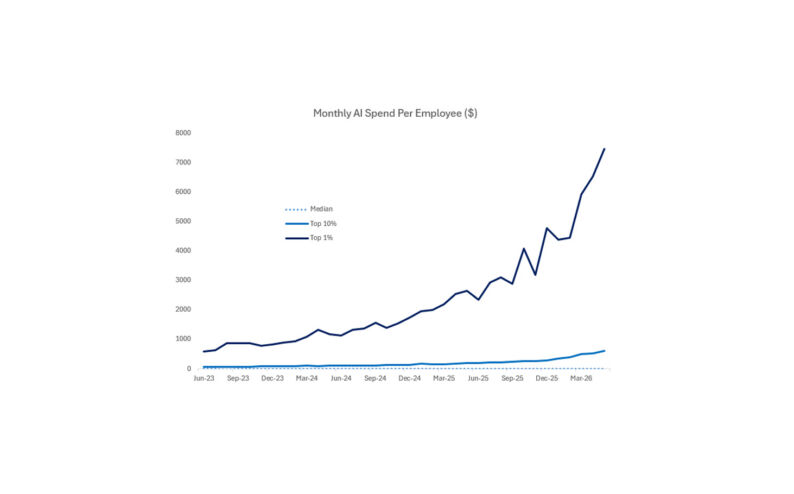

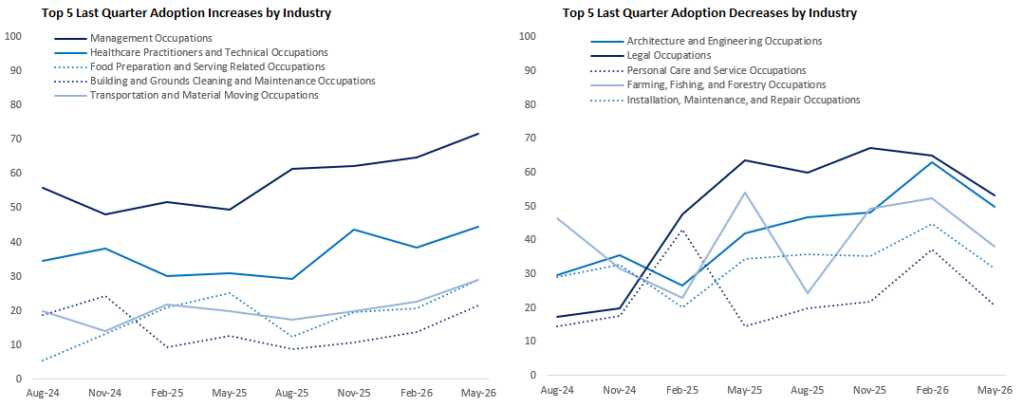

MEANWHILE, THE NEWS ON AI CONTINUES TO BE PROBLEMATIC…not because the technology is failing, but because the path from capability to monetisation is becoming more contested. The market still wants to treat AI as if better models mechanically translate into more capex, faster adoption, and ultimately operating leverage. The incoming data increasingly suggests a messier political economy. On infrastructure, Data Centre Watch found that local opposition successfully blocked or delayed 75 data centre projects nationwide, with a notional value of about $130bn, in the first quarter of 2026. This equates to an annualised block rate roughly four times the 2025 pace, and the report framed the surge as a structural shift rather than a cyclical spike, as communities internalise the opposition playbook and state-level regulatory uncertainty rises. More than 300 state data centre bills were filed in the first six weeks of 2026 alone, with statewide moratorium proposals introduced in 14 states from both sides of the aisle, while Maine came within one House vote of becoming the first state in US history to impose a statewide data centre ban. This is exactly the kind of friction that markets have been too willing to ignore…AI may be digital at the point of use, but it is intensely physical at the point of production, and the physical footprint is now becoming politically constrained. The adoption data is not especially comforting either. The latest cut of the Real Time Population Study suggests that, whilst regular AI use for work continues to rise in aggregate (39.2% of working-age adults using AI for work at least once per week), the occupational and industry-level data paints a much less linear picture. Adoption continues to rise in some sectors but is now rolling over in others. Some of this is not surprising…as I’ve stated before, the “frontier is not for everyone”, and it is altogether reasonable that more physical industries – farming, fishing, forestry, installation, maintenance, and repair occupations – would see adoption plateau or decline after an initial experimentation phase. What is more concerning is the outright decline in AI adoption in legal and architectural occupations, down 12% and 13%, respectively in Q2 versus Q1. These are exactly the types of knowledge-work verticals where the market has been most comfortable assuming rapid diffusion. The focus for investors should therefore be less on whether aggregate adoption is still rising, and more on whether adoption is tracking relative to expectations. On that basis, I would argue AI is underperforming. This also fits with the regulatory turn…the AI debate is moving beyond the old consumer-protection frame of bias, privacy, copyright, and misinformation, and into a state-power frame focused on release protocols, access controls, national security, and US-China competition…which is a very different political regime from the one embedded in AI valuations. Once models become autonomous agents, and once governments start asking who gets access to frontier capability, AI starts to look less like ordinary software and more like strategic infrastructure. That raises the risk of audits, reporting requirements, release approvals, export controls, energy restrictions, workplace rules, and a much more uneven regulatory landscape. Some of those interventions may be individually defensible, but collectively they raise the cost of turning capability into earnings and make the monetisation path more fragile. This is the broader point I keep coming back to: AI does not need to disappoint technologically to disappoint financially. It only needs capex to become politically contested, adoption to undershoot expectations, and regulation to arrive suddenly, unevenly, and all at once. Builders want to live in the future. Local communities, workers, regulators, and governments are increasingly asking who pays for it, who gets to build it, who controls access to it, and who gave the industry permission to set the speed limit.

Source: Real Time Population Survey, Generative AI Tracker, Citadel Securities

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/