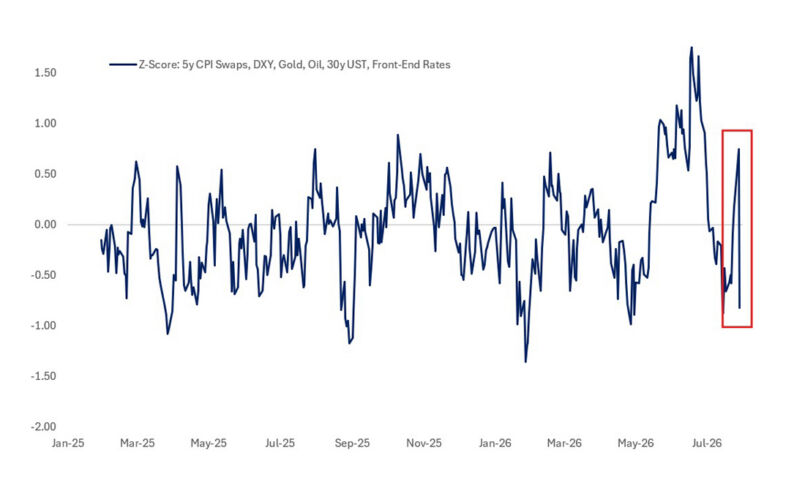

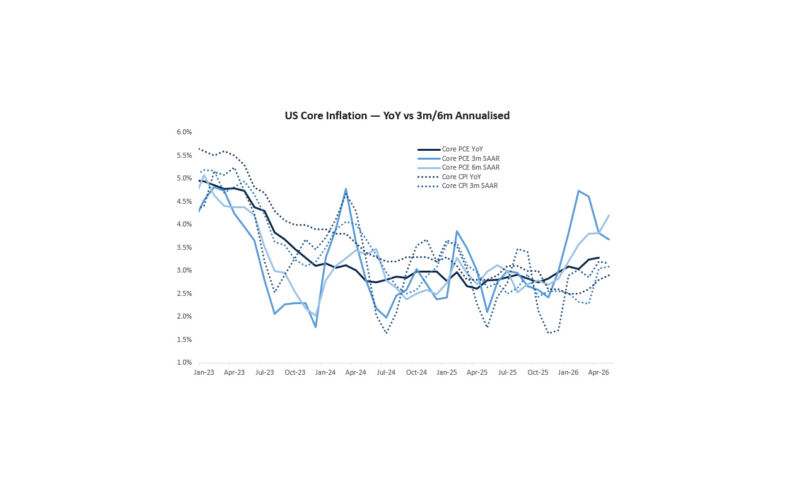

“CREDIBLE” IS THE WORD THAT MOST SPRINGS TO MIND WHEN ASSESSING CHAIR WARSH’S FOMC DEBUT. His emphasis on price stability left investors in no doubt about which side of the mandate he is currently concerned about, stating in the presser “persistently high prices are a burden for the American people” and “this committee will deliver price stability”. His hawkish tone confounded the expectations of many in the market who had predicted a ‘dovish-come-what-may’ approach and marked a substantive change from the Powell-era willingness to look through persistently above-target core inflation and (arguably) excess sensitivity to the employment side of the mandate. The Summary of Economic Projections (SEP) decidedly had the same tune with nine members signalling rate hikes this year, the majority of which (5) expect two increments. With the 2026 median core PCE projection moving up to 3.3% (from 2.7%) and the u/e rate down to 4.3% (from 4.4%) it appears that the FOMC is finally accepting a point I have been making for some time: inflation is the greatest threat to the US economy and markets. Laying the groundwork for rate hikes should not come as a surprise to anyone. But beyond the spot assessment, let’s be very clear – this is a regime change at the Fed. Warsh outlined that we should expect less forward guidance (he notably did not input a dot in the SEP), long-term adjustments to how the balance sheet is used, and changes to the way the Fed assesses the health of the economy, rightly observing that many of the survey-based measures currently used are unsatisfactory. But what does all this mean? It means a Fed that is likely to be more responsive, less predictable meeting-to-meeting, but ultimately more credible. The old regime prized predictability in the path of rates; this one seems more willing to move quickly when the reaction function demands it…but just as willing to unwind that insurance once the risk distribution looks more benign. That is why the dots showing hikes and then cuts should not be dismissed as incoherent…indeed, they illustrate the point. In a world where the central bank is proactive about future risks, the policy rate can move around more, but the underlying macroeconomic outcomes become less volatile. Credibility is not the ability to pre-commit to a smooth quarterly glidepath…it is the ability to convince markets that you will act before the problem becomes embedded. Done well, that means the Fed ultimately has to deliver less, not more. This is also why the argument that lower oil prices should mechanically take hikes off the table misses the regime shift. The near-term deviation is not about one inflation input…it’s about which side of the mandate the Committee is choosing to prioritise. Warsh made clear that inflation, not the labour market, is the dominant concern for now. That makes every upcoming meeting live…a point he underlined by noting that the next meeting is only six weeks away…and it means the market needs to get used to a Fed that does not wait for a fully priced hike or cut before acting. The price of greater credibility may be less ex-ante comfort for front-end pricing. Moreover, the asset-market implication is not simply ‘more Fed volatility = higher term premium’. If anything, a hyper-credible Fed should be good for long end rates. A central bank that is willing to adjust the policy rate more aggressively in response to the data should reduce the probability of inflation persistence, de-anchoring, or a larger macro accident. In that world, the 10y rate (which has greater factor loading to financial conditions) is more stable…the vol surface should flatten…so credibility should compress rather than expand term premium. Put simply, this is a more live, more reactive, and less hand-holding Fed…but that is precisely what makes it more credible.

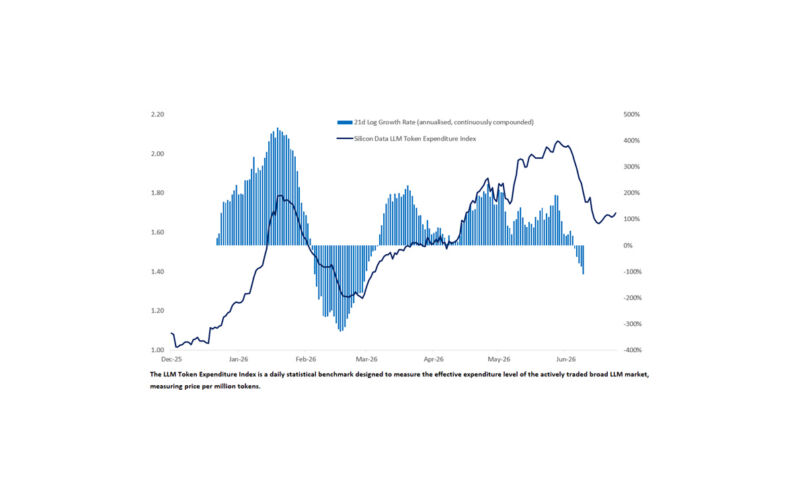

Source: Ramp AI Index, Citadel Securities, Data as of Jun-2026

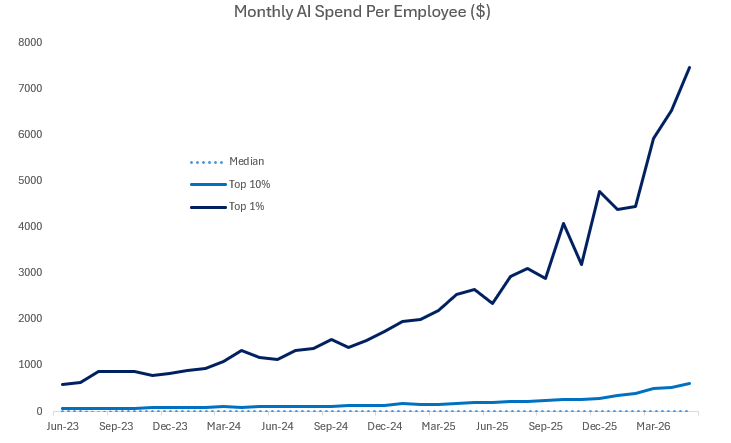

THE MORE I THINK ABOUT THE AI DEBATE, THE MORE CONVINCED I AM THAT THE FRONTIER IS NOT FOR EVERYONE. The question is not whether AI usage keeps growing – it almost certainly does – but who can afford to remain at the frontier and who is forced to optimise away from it. For firms with the data, distribution, balance sheet, engineering depth, and organisational capacity to convert expensive inference into measurable ROI, rising token usage is self-reinforcing…they spend more because the models make more of their existing business activities profitable, faster, or more scalable. But for firms that cannot deploy the technology effectively, the frontier becomes a tax rather than a tool. They either get priced out, settle for cheaper generic models that are good enough for narrower workflows, or discover that the productivity gain is insufficient to justify the inference bill. This is where the AI story becomes more Darwinian than egalitarian. To be sure, it is not a fixed pie…small firms can still benefit enormously as cheaper models lower barriers to entry and make previously uneconomic activities viable. But the distributional impact is unlikely to be smooth. The largest and best-equipped firms can use frontier AI to widen moats, automate more complex work, and compound scale advantages. The smallest firms can access tools that once required whole departments. The hardest place might be the middle…large enough to face the cost and complexity of enterprise deployment, but not large enough to amortise frontier-level inference across truly scaled revenue pools. AI is therefore not just a productivity shock; it is a magnifier of business quality. That also makes the politics more complicated. In recent notes I argued that AI increasingly risks being framed as ordinary consumers paying higher electricity costs so trillion-dollar technology companies can build hyperscale compute clusters, train models and potentially replace workers. If frontier AI is both economically powerful and access-constrained, then the political question becomes not just whether AI raises aggregate productivity, but who gets access to the frontier, who pays for the infrastructure, and who captures the surplus. The recent Anthropic episode where a US government export-control directive led the company to suspend access to its Fable 5 and Mythos 5 models is a reminder that frontier models are no longer being treated as ordinary software products, but as strategic assets. Once governments begin deciding who can access which models, and on what national-security grounds, the economics of AI become inseparable from regulation, industrial policy, export controls, and geopolitics. That does not invalidate the AI investment case…but it does make it less clean. The frontier may still produce enormous winners, but it is unlikely to be universally accessible, universally profitable, or politically neutral. Welcome, again, to the politics of AI.

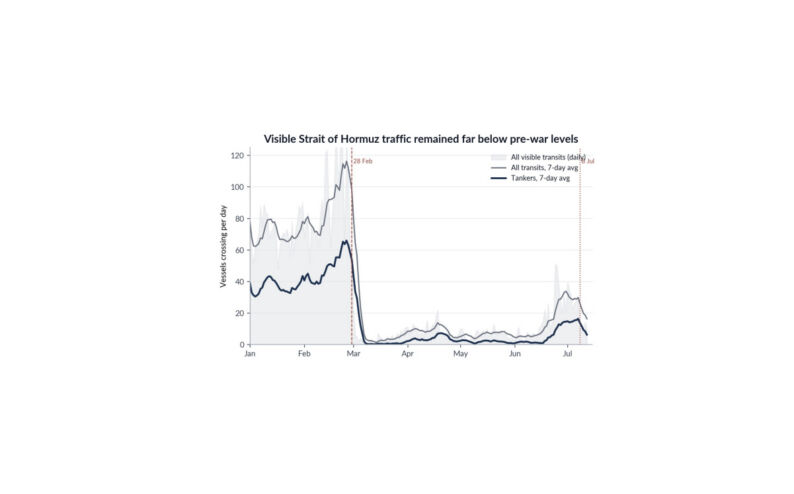

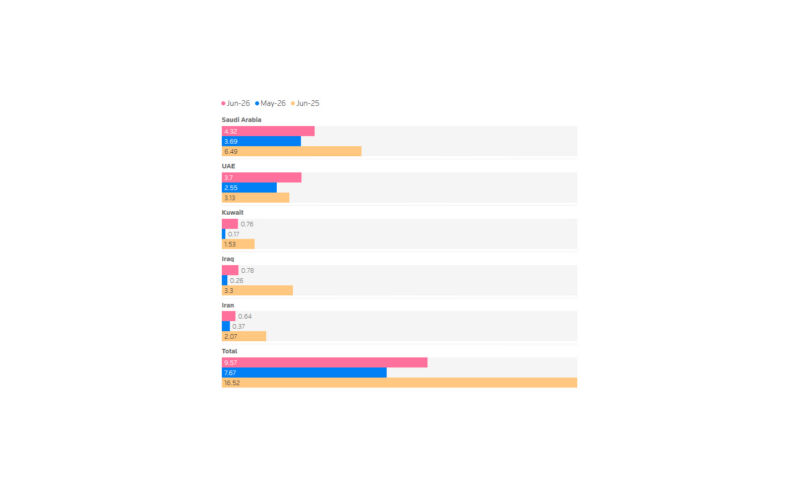

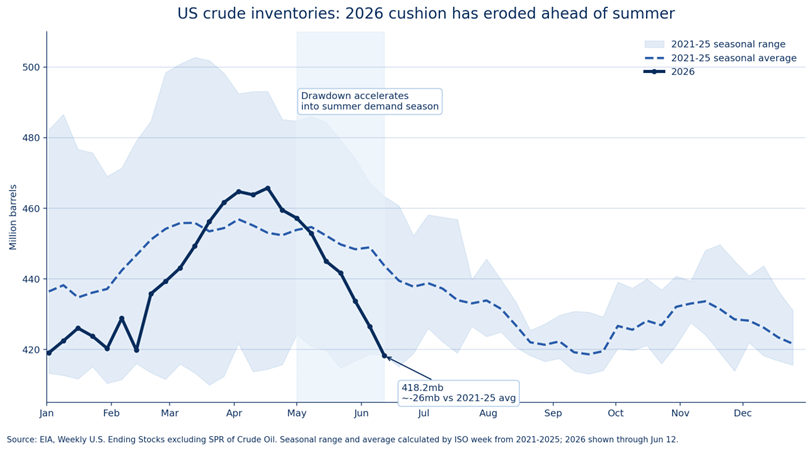

THE IRAN MOU LOOKS LIKE AN EXPENSIVE EXIT RAMP. As the dust settles, the reported framework appears to deliver a 60-day ceasefire or negotiating window, a phased reopening of the Strait of Hormuz, waivers for Iranian oil exports, a framework for nuclear talks, and the possibility of broader sanctions relief and reconstruction funding. But it does not deliver full nuclear disarmament, regime change, or a comprehensive answer on missiles, drones, or proxy capability. Nor does it remove the global economy’s exposure to Iranian leverage over the Strait. Indeed, there is implementation risk in the fine print…if Provision 5 creates even the perception of a future Iranian/Omani fee or administrative role around Hormuz, however described legally, then the market may conclude that chokepoint access has become a priced and politically contingent service rather than a freely assumed feature of the global energy system. The nuclear track is no cleaner…an interim MOU may buy time, but any durable agreement involving nuclear limits, verification and sanctions relief could still run into congressional review, leaving legal and political uncertainty around the sequencing of the deal. The conflict has incurred significant human and financial costs, with direct military expenditures reportedly reaching $29bn and scarce munitions being depleted, whilst producing a limited framework that restores portions of the pre-war energy-flow status quo and leaves key aspects of the nuclear question unresolved. The US has secured near-term de-escalation and a path to reopen a critical artery of global energy supply, but only after Iran demonstrated that relatively low-cost asymmetric capabilities could impose meaningful economic and market costs. The Strait may reopen, but the strategic risk premium around energy, shipping and asymmetric warfare is unlikely to disappear. Of course, Washington retains overwhelming conventional superiority, but the conflict has reinforced a broader lesson…weaker states can create leverage by disrupting strategic resource flows through global chokepoints. The future of warfare increasingly looks like low-cost unmanned systems, distributed strike capacity and asymmetric disruption forcing expensive defensive responses, with leverage coming from the ability to impair logistics, raise insurance premia, disrupt energy flows and transmit geopolitical risk into inflation-sensitive consumer and asset prices. From here, I also see two-sided risks around oil. Historically, supply shocks can be followed by overproduction, inventory rebuilding and eventually a glut…headlines that Gulf producers can restore supply as Hormuz reopens point in that direction. But the physical market also proved more adaptive than the initial panic implied…and China’s product-export flexibility helped cap the upside, which may in turn limit the downside from reopening. Chinese refiners and strategic reserves may need restocking, whilst the market is reopening into depleted inventories, summer demand, US crude stocks below seasonal norms, Cushing near operationally tight levels, and gasoline prices that, while lower since the deal, remain above pre-war levels. The optics could therefore remain challenging if consumers are left with higher gasoline prices…depleted munitions…no definitive nuclear settlement…and a clearer understanding of the coercive value of asymmetric warfare.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/