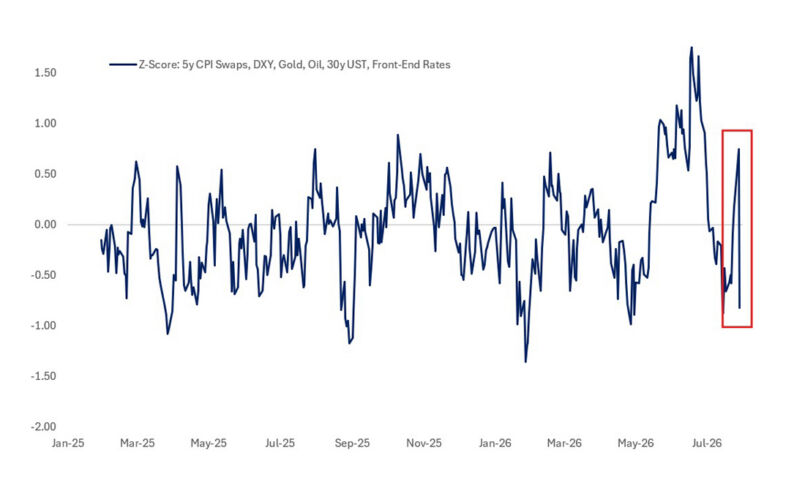

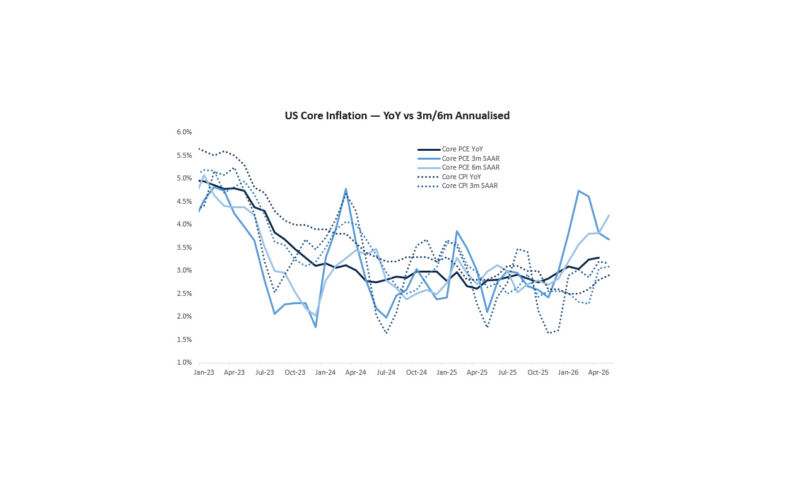

THE HEIGHTENED CREDIBILITY AT THE FED UNDER CHAIR WARSH THAT I WROTE ABOUT LAST WEEK IS NOW BECOMING VISIBLE IN MARKETS…in the shape of the yield curve, the behaviour of the dollar, and in the repricing of the front end. A more credible Fed does not necessarily mean higher yields…as evidenced by the recent rally in 30-year USTs. In fact, the broader change is that the market is beginning to understand the shifting reaction function: inflation misses are no longer going to be accommodated simply because growth is holding up or because a temporary energy shock is reversing. For most of the post-pandemic period, policy was still interpreted through the lens of insurance…if growth weakened, the Fed would ease…if risk assets wobbled, the Fed would validate easier financial conditions…and if inflation came from supply side or energy, officials would look through it. The Warsh Fed is signalling something different…inflation above target is not a communications inconvenience, it is the constraint. Markets have moved in that direction, but there is likely more room to run. The front end has started to reflect a Fed that may need to hike again, and the curve has begun to internalise a central bank that is trying to re-anchor inflation expectations rather than protect every growth scare. But the broader market still seems too comfortable with the idea that lower oil prices automatically remove the case for tighter policy. That is the wrong conclusion – oil coming down lowers headline pressure, but it does not prove that the inflation process has normalised. This week’s PCE data make this clear…headline inflation remains elevated (4.1% YoY), core inflation is still too high (3.4%), and the composition is not benign. The Fed’s preferred measure remains well above target, while income and spending are still firm. More importantly, the “supercore” categories are not behaving like an economy that has returned to a clean disinflation path…services inflation excluding housing and energy rose ~0.5% MoM. That is exactly the type of cyclical inflation pressure a credible Fed cannot ignore. The spot reality is that inflation is now being reinforced by a broader set of forces…resilient nominal demand, input-cost pass-through, tariffs and supply-chain frictions, and AI-related hardware scarcity. The latest tech hardware price increases are an important signal. As I have argued before, AI is inflationary first – before it is deflationary through productivity – requiring enormous physical investment in chips, memory, power, cooling, land, construction, grid connections, and engineering talent. Those bottlenecks raise prices before they raise economy-wide productivity. That is now showing up in the real economy…Apple price increases tied to component costs, memory shortages linked to AI data-centre demand, and reported TSMC price increases for advanced-node wafers all point in the same direction. The AI capex boom is not just a stock-market theme, it is an input-price shock…it pushes on the cost base of the technology sector and then migrates into consumer hardware prices. This is not the 1990s productivity story yet…it is a capacity-constrained investment boom…and the policy implication is straightforward. We are moving away from a world of ultra-loose fiscal and monetary policy that could be justified almost independently of the growth outlook. The Fed does not need oil to go higher to keep policy restrictive…it needs convincing evidence that underlying inflation is returning to target. In sum, the next phase is not just whether the Fed hikes once or twice…it is whether investors stop treating every decline in oil or every soft patch in risk assets as a reason to rebuild the old policy-put framework. It is too early to say Chair Warsh has Alan Greenspan’s iron grip on the FOMC…but the early signs point in that direction…a unanimous first meeting, a shorter statement, less forward guidance, and a cleaner price-stability message all increase the Chair’s control over the reaction function. Markets may not be dealing with a committee of dots anymore, but instead a strong Chair.

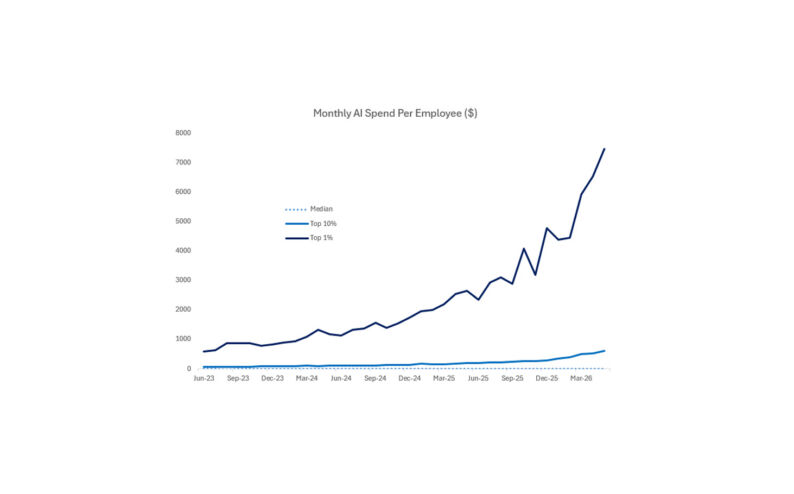

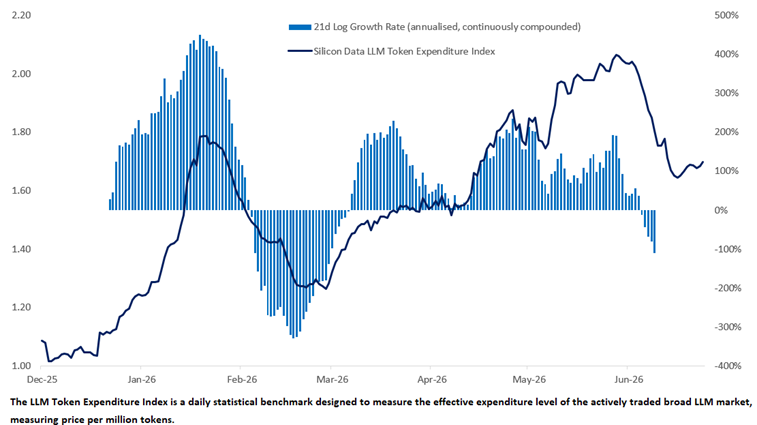

MICRON’S RESULTS OFFERED A TEMPORARY REPRIEVE FOR AN AI THEME THAT, LOCALLY AT LEAST, LOOKS LIKE IT MAY BE RUNNING OUT OF STEAM. The growing focus on token costs, harder questions around the ROI on capex, and the decline in token expenditure indices are all beginning to challenge the durability of the investment thesis. The decline in GPU rental costs tell a similarly concerning story. It is hard to be precise about what is driving the deterioration in the data, but my instinct is that it’s another sign that end-user demand for AI is becoming more price sensitive. If that is right, then the bottlenecks the market has been so willing to treat as bullish may no longer be quite so helpful at this stage of the cycle. That said, Micron’s results were clearly strong at the headline level, with Q3 adjusted EPS of $25.11 ($20.78 expected), revenue of $41.46bn, and Q4 guidance well ahead of expectations on AI-driven memory demand. The most interesting part was the ~$100bn of customer agreements…binding, multi-year take-or-pay contracts for DRAM and NAND memory with pricing bounds and supply volumes locked-in with strategic clients. That clearly improves revenue, margin, and cash-flow visibility…but in my mind the structure contains some hints of a more concerning signal. By giving customers protection against higher future memory prices in exchange for downside support, Micron is arguably selling away some upside in its own business model, which points to a management preference for certainty over complete confidence in a much stronger forward pricing environment. To be clear, it is hard to argue this does not show very strong customer demand today, but investors may look back on it as an early warning sign if the cycle does turn from here. Relatedly, the Apple price rises sit in the broader bucket of concerning news-flow in an AI-adjacent space. This is the other side of the bottleneck…supply-chain pressure and consumer price increases large enough to create some demand destruction. The market seemed to recognise that, with Apple down ~6% on the news. Hyperscaler capex may be price inelastic (for now), but consumers and end users are not. That is the problem for a market that, for the last few months, has treated shortages as a clean positive demand signal, with very little attention paid to what they eventually mean for the end customer. Moreover, hyperscalers are being punished by the market for their capex spend, whilst semis are being rewarded as recipients. But at some point, the leadership of hyperscaler companies may take this signal and retreat…which would have a dramatic impact on this entire investment complex given how heavily positioned it is.

THE POLITICS OF AI ARE GETTING WORSE…which should not come as a surprise. The market sees AI as operating leverage, but workers see it as jobs risk. Consumers see higher hardware prices, rising electricity bills, more surveillance, and very little immediate upside in their daily lives. That is a dangerous political mix. Prior technology cycles had an obvious consumer story before the labour-market, political and regulatory costs came to the fore. AI is different…the consumer product exists, but the gains so far are mostly at the enterprise level. The capex is in data centres, the leverage accrues to corporations, and the anxiety goes to workers. Danielle Li’s work is useful here because it makes the worker-agency problem precise. AI adoption is not just a question of whether firms can deploy models, it is a question of whether workers will continue supplying the tacit knowledge those models need. Firms have historically rented expertise from workers…but AI allows them to record, codify and scale that expertise as capital. Once workers understand that their documentation, chats, decisions, and process knowledge can be used to train systems that replicate their work, they have an incentive to withhold, bargain, litigate or demand a share of the gains. For now, the benefits of AI are being sold as productivity, but the costs are being experienced as disruption. If a company uses AI to reduce headcount, monitor workers, compress wages, or extract tacit knowledge, that may be good for margins…but it is not obviously good for the median voter. And in a democracy, that distinction is crucial. My fear is that the next populist movement will be anti-AI. Indeed, the political argument almost writes itself…why should companies get to train models on workers’ knowledge, automate their tasks, monitor their performance, and keep the surplus? That is where the tacit-knowledge problem becomes political…much of what makes firms work is not written down…it lives in relationships, judgment, shortcuts, process knowledge, institutional memory, and the unspoken means by which outcomes are actually delivered. AI wants to synthesise that knowledge and codify it. But codification requires either consent and incentives…or extraction (which could be politically challenging). This is already where the politics are moving…the debate is no longer just about existential risk or model safety…it is about workers’ rights, privacy, automated decision-making, surveillance, bias, copyright, energy use and who owns the productivity gains. Once AI becomes a labour issue, it stops being a Silicon Valley story and becomes a median-voter story…which could become a problem for AI valuations. The game theory for politicians is obvious…there are votes in being tough on AI…but there are very few votes in defending model providers, hyperscalers and corporate efficiency programmes. That does not mean AI goes away, but it means the cost of deploying it rises. Some of that cost will be explicit…compliance, audits, disclosure, licensing, compensation, energy regulation, copyright settlements, and limits on workplace monitoring. Some of it will be implicit…slower adoption, worker resistance, reputational risk, political scrutiny, and a higher probability that the most profitable use cases are regulated before they fully scale. This is why the politics matter for markets…AI does not need to fail technologically to disappoint financially…it only needs the path from capability to monetisation to become more contested. The Iran deal is a useful reminder of the broader political backdrop – even a President’s own party can turn quickly when voters believe an agreement is expensive, weak, or unfair. AI has the same vulnerability…if the public comes to believe that AI is a bargain in which companies get the upside and workers get the downside, the politics will turn very quickly. And unlike the early internet, AI does not yet have a broad consumer-level dividend large enough to offset that resentment. That is the key point…the technology is undoubtedly extraordinary…and the economics may be real…but the politics are deteriorating. The industry should address this sooner rather than later. As I’ve stated before, markets are usually most vulnerable when the secular story remains compelling, but the macro backdrop turns against the equity narrative at precisely the moment when valuations require continued earnings upgrades, benign discount rates, and investor willingness to look through near-term cyclicality. The landscape may be shifting.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/