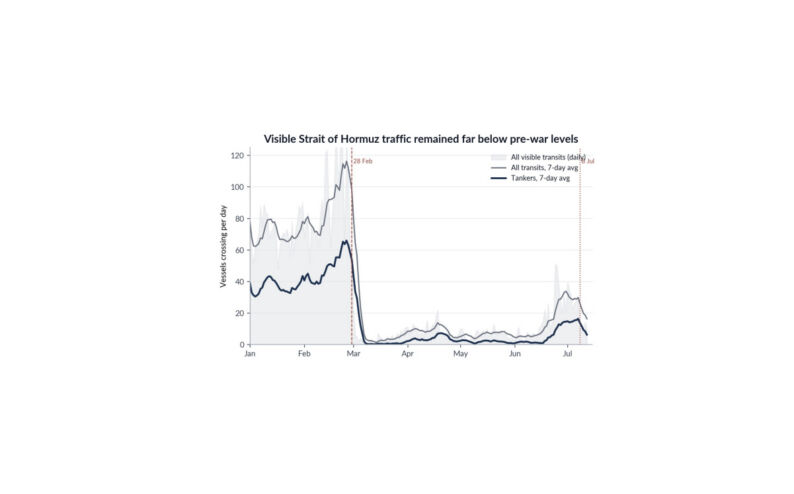

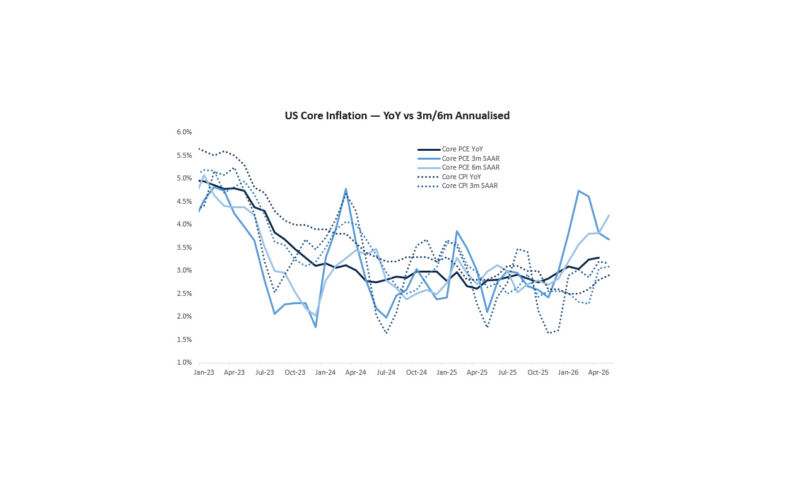

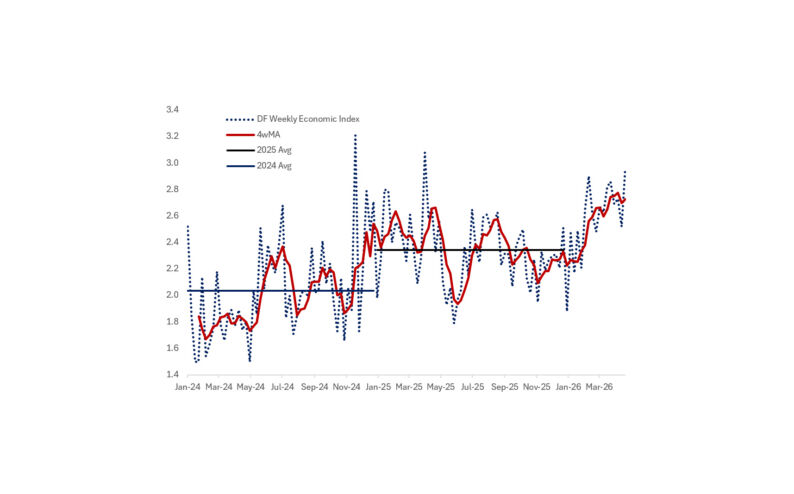

“MORE GROWTH, MORE INFLATION” HAS BEEN THE MANTRA OF THIS NOTE IN RECENT MONTHS. This was the reality prior to the Iran conflict…and is even more the case now following an energy and supply chain shock from the closure of the Strait of Hormuz and a once-in-a-generation AI infrastructure boom that has been supersized in recent weeks with commitments to spend over $700bn on capex in 2026 alone. Of course, the key difference compared to last year is that AI is no longer just a capex story…annualised revenue growth at companies like Anthropic suggests that enterprise AI adoption is translating into real economic demand. The Dallas Fed’s high-frequency tracker for US growth has GDP at 3.23% (scaled to Q4) reflecting a buoyant economy that has yet again proven resilient to external shocks. On the other side of the ledger…even if the conflict ends soon with a re-opening of the Strait, the inflationary effects are likely to persist. Inventories drawn down during the conflict will need to be replenished, creating a period of additional demand even after the immediate disruption has passed. More importantly, firms and governments are likely to put greater emphasis on energy security, maintaining larger inventory buffers, diversifying supply chains, and investing in redundant infrastructure. These measures improve resilience but also reverse some of the efficiency gains of the pre-crisis system, embedding higher costs in energy, transportation, insurance, and capital investment. As a result, I can see energy prices and broader input costs remaining structurally firmer than before the conflict, particularly when layered on top of rising electricity demand from the ongoing AI infrastructure buildout. Friday’s NFP at 172k (following 179k for the prior month) was a reminder that the labour market is starting to inflect upwards too – something I have been highlighting for some time – and is therefore less disinflationary. Today’s labour market is not overheating, but it may be approaching an inflection point…with unemployment still low, layoffs historically subdued, and labour supply constrained (due to changes in immigration policy), any acceleration in growth – from a combination of AI investment, supportive fiscal policy, and easy financial conditions – could tighten labour markets more quickly than expected. In that scenario, wage growth could accelerate well above levels consistent with the Fed’s inflation target, contributing to persistent services inflation even if energy and goods inflation do moderate. Bottlenecks in the delivery of data-centre capacity represent another potential source of inflationary pressure…the rapid AI buildout is running into constraints around power availability, grid connections, transformers, construction labour, cooling equipment, and specialised engineering capacity. As demand outpaces the industry’s ability to expand supply, costs are likely to rise across the data-centre value chain. Whilst these pressures may initially be concentrated in a narrow set of sectors, I would expect them to spill over into broader construction, industrial, and energy markets, reinforcing inflationary pressures and delaying the supply response needed to meet growing AI-related demand. A few weeks ago, the headline for this note was “Don’t get behind the curve” reflecting a concern that the Fed was not focused enough on these risks. This now appears to be changing…policymakers such as Governor Waller and Dallas Fed President Logan appear increasingly concerned about upside inflation risks…Waller has shifted from advocating cuts to arguing that the Fed should abandon its easing bias altogether, while Logan has openly discussed the possibility that rates may need to rise further. In sum, strong AI-driven investment, energy-market tightness, improving labour-market conditions, and infrastructure bottlenecks suggest upside risks to nominal growth and inflation. The next move from the Fed is most likely a hike…perhaps soon. You can’t have your cake and eat it too…a tightening of FCI is the next big risk for markets.

Source: Bloomberg, Citadel Securities

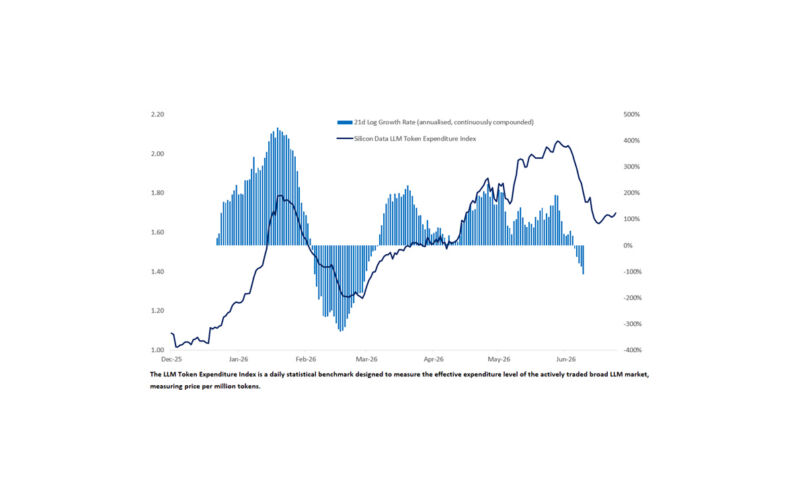

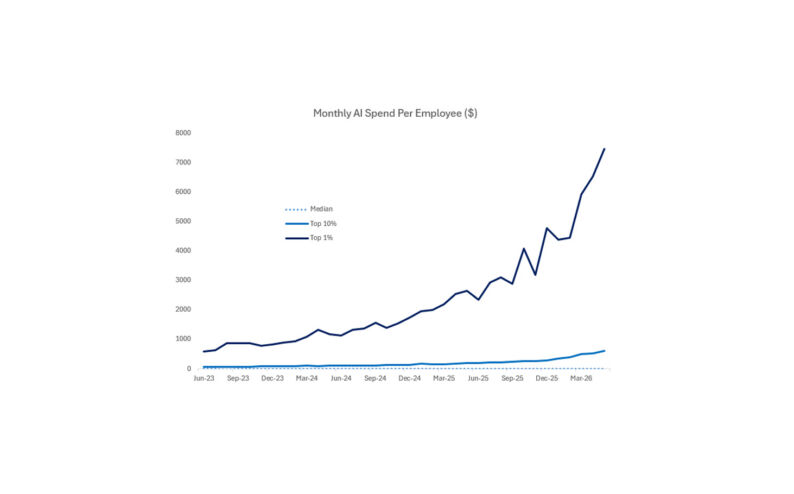

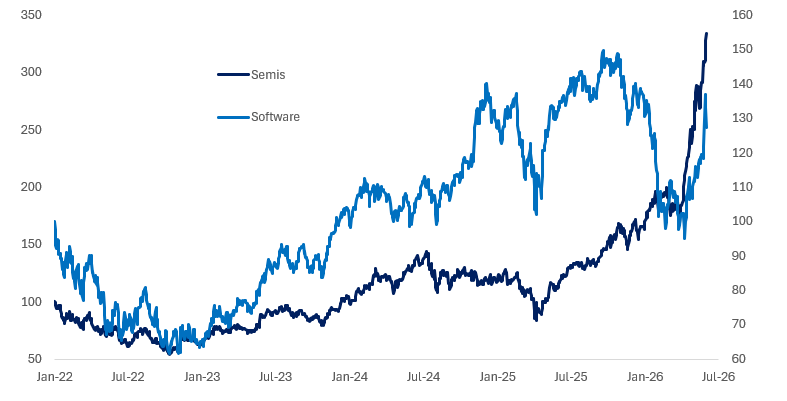

“NARRATIVE FRENZY” RATHER THAN “BUBBLE” IS HOW I WOULD DESCRIBE THE CURRENT FOCUS ON ARTIFICIAL INTELLIGENCE. Dramatic upward revisions to capex have been the key driver of momentum in this theme, but it’s worth asking why. The answer is that there is still insufficient compute to meet demand for increasingly capable and compute-intensive models. Investors should not underestimate the implications of this for the demand side of the equation. The market has largely focused on what rising compute requirements mean for semiconductor demand and infrastructure spending, but less attention has been paid to what they mean for the economics of adoption. More capable models undoubtedly create greater value, but they also consume more compute. The key question is whether productivity gains scale faster than the cost of generating them. As Frank Flight has consistently argued, the primary constraint on AI may not be model capability but the physical availability and economic cost of compute. Those constraints are likely to influence the pace of adoption. Unlike traditional software, where the marginal cost of serving an additional user is close to zero, AI carries a meaningful and ongoing compute cost. The economics therefore depend not simply on what the technology can do, but on whether the productivity generated is sufficient to justify the resources required to deliver it. This distinction matters because the market has largely treated greater compute intensity as an unambiguously positive development for the infrastructure layer. Yet if the cost of deploying increasingly sophisticated AI systems rises faster than the value they create, adoption may prove more gradual and selective than current expectations imply. The rerating of software stocks alongside the continued strength in semiconductors provides a useful illustration of how the market’s perspective is evolving. Investors appear to be revising down the speed of AI adoption and the disruptive impact of the technology, while continuing to reward the infrastructure layer. What has not yet been fully debated, however, is what increasing compute intensity means for the revenue trajectories of AI labs and other AI beneficiaries. If AI proves significantly more expensive to deploy than initially anticipated, adoption may increasingly be constrained by price. As the cost of inference and agentic workflows becomes clearer, firms are likely to become more selective about where they deploy AI capital, particularly if returns on investment prove less compelling than current expectations suggest. To be clear, revenue growth across the AI ecosystem is real and substantial. Anthropic’s ARR is reportedly approaching $50bn, while Dell’s AI server revenues have increased more than 750% YoY. This is not a sector that can be dismissed as a purely speculative bubble; the earnings are already material. The question is whether current revenue trajectories can sustain the expectations embedded in valuations once we move beyond the phase where every management team feels compelled to have an AI strategy, budget, and narrative. There are already tentative signs that cost is becoming a more important consideration. Large enterprises are beginning to scrutinise AI spending more closely, reports of unexpectedly large token bills are becoming more common, and several industry anecdotes suggest that enthusiasm for agentic workflows may not always survive contact with the economics. Whether these examples prove significant remains to be seen, but they point to a question that markets have not yet fully grappled with. Investors have enthusiastically embraced the compute-intensity argument on the infrastructure side of the ledger, rewarding semiconductor and data-centre beneficiaries accordingly. Less attention has been paid to the other side of the equation: if AI is more expensive to use, what does that imply for the pace of adoption and the durability of revenue growth? If adoption ultimately falls short of expectations, forward earnings estimates may prove too optimistic, leaving valuations more stretched than they currently appear. In that scenario, today’s strong revenues may come to be viewed as a function of an extraordinary adoption cycle driven by competitive pressure and fear of missing out, rather than a reliable guide to long-term demand.

Source: Brookings Metro

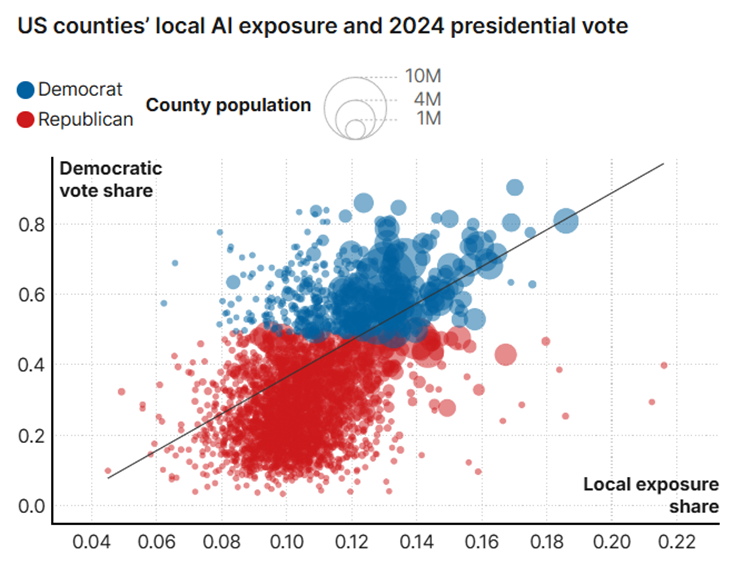

THE “POLITICS OF AI”, SOMETHING I FLAGGED IN AN EARLIER NOTE, CONTINUES TO GATHER STEAM. AI is increasingly unpopular with the general public, and this is starting to spill into the DC agenda and broader political conversation…President Trump this week signed an executive order that increases the scope for government oversight of frontier models, albeit on a voluntary basis. This represents a material step up in the AI regulatory framework and comes alongside significant focus from Democrats on concerns around the impact of data centre buildouts on local energy costs. A number of potential candidates on both sides of the aisle have also called for data centre construction moratoria in various states. None of this is particularly binding, but as we approach the midterms (and beyond) I expect there to be increased focus on the AI regulatory framework. Given the starting point, the trajectory is clearly skewed towards more regulation, not less. It makes sense for politicians to focus on this issue because it is a significant source of concern for voters, particularly among young people…polling from Pew Research suggests that half of US adults say the increased use of AI in daily life makes them feel more concerned than excited, according to a June 2025 survey. People do not like AI because it is associated with risks to jobs, national security, financial infrastructure, and broader disruption. An interesting study from Mark Muro at Brookings notes “AI exposure – and related potential political anxiety – concentrates in Democratic-leaning places: Sixty-two of the 100 most AI-exposed U.S. counties went blue in the 2024 presidential election. This partisan correlation reflects occupational sorting rather than ideology, but even so, workers in blue counties whose jobs are most exposed to AI are potential flashpoints for AI-related economic anxiety heading into the midterm elections”. This implies that Democrats may be the beneficiaries of concerns around AI displacement. Importantly, this theme also intersects with the Iran war through the lens of higher energy prices. AI is unpopular, inflation is unpopular…so politicians who focus on addressing these issues are likely to outperform…not just in the midterms, but for years to come. Unfortunately for markets, a policy response to either or both issues may result in somewhat less exuberance around the AI theme, as well as a broader tightening of financial conditions.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/