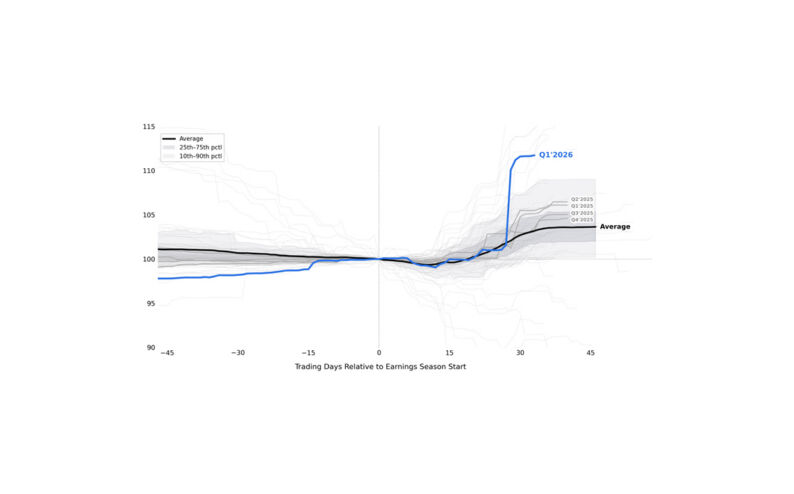

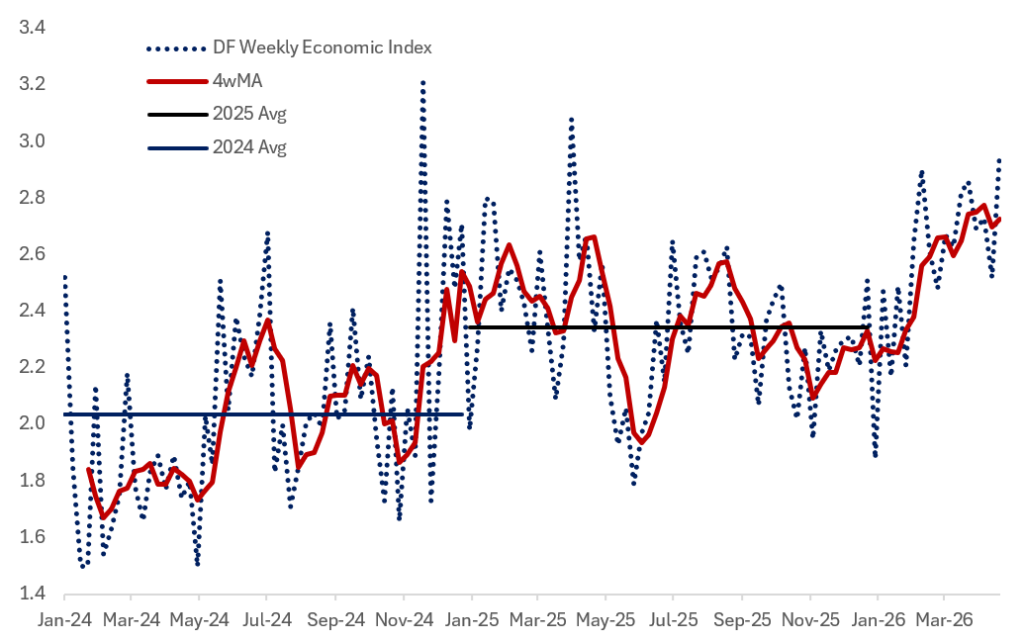

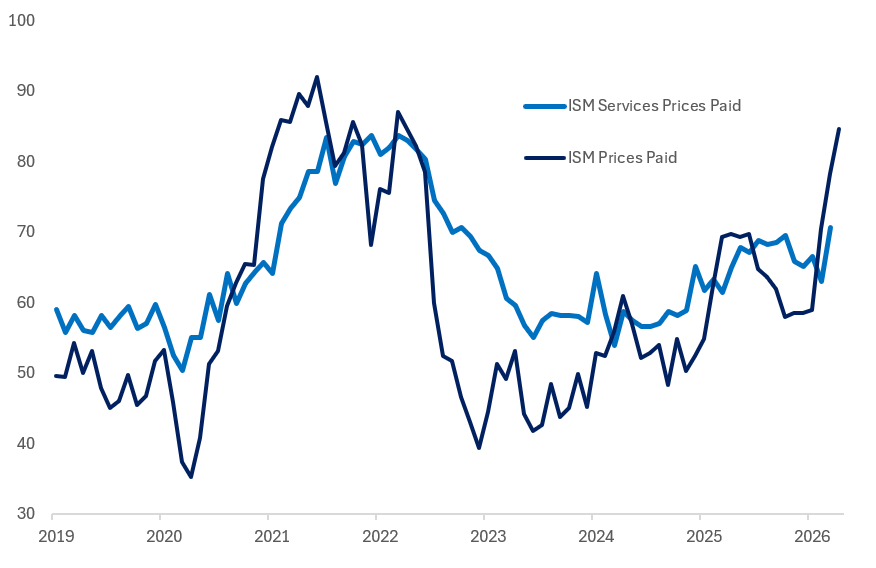

THE FUNDAMENTALS OF THE US ECONOMY REMAIN SOLID. This is the conclusion despite two months of the Iran war creating disruption to global trade and energy markets. Prior to the conflict starting, my view was that markets were underestimating the extent of nominal growth and risks to inflation. Easy financial conditions were buttressed by a positive fiscal impulse, the AI capex investment boom, and stable labour markets (albeit under a new immigration regime sharply reducing the steady-state pace of job growth). The conflict pushed financial conditions tighter and risked derailing this story with both actors caught in a classic escalation trap…but President Trump pulled back from the brink four weeks ago and since then we’ve seen FCI ease back to the lows, driven by a buoyant stock market with NDX rallying 21%(!) from the lows. The fundamentals back this up…the Atlanta Fed’s GDPNow sits at 3.5% for Q2 with PCE consumer spending estimated at a healthy 1.7%. My preferred high-frequency tracker for the economy – the Dallas Fed’s WEI, which uses around ten daily and weekly activity indicators and rescales them to align with GDP tracking – accelerated to 3%…broadly consistent also with the signal from the PMI (54.5) and ISM (52.7) both of which continue to strengthen, likely reflecting the capex boom. Moreover, Q1 reporting season so far suggests a robust backdrop for corporate profits. With 63% of the S&P 500 having reported, 84% have beaten on EPS and 81% on revenue…with the earnings growth rate for the index at 27.1%, which would mark the highest level since Q4’21 if maintained. Almost every major tech firm is leaning heavily into AI with the big four (Alphabet, Amazon, Meta, Microsoft) widely expected to exceed $700bn in capex spend, up almost 80% from last year. The market continues to become more discerning around ROI, not rewarding companies simply for “AI exposure”…they want to see monetisation and results. The strongest proof of AI demand (so far) is in cloud growth, which has accelerated meaningfully with Alphabet and Amazon the key beneficiaries. Apple also stood out by taking a more measured AI approach, with investors rewarding its discipline versus peers. The labour market also looks fine, likely because supply conditions mean the bar for hiring is relatively low in order to keep the unemployment rate steady…this is best captured by the San Francisco Fed’s labour market stress indicator, which is currently running at 2/50. Our own aggregate measure of labour market conditions, compiled by my colleague Frank Flight, is similarly constructive suggesting that the jobs recovery is continuing gradually, with our composite indicator running at +0.3 standard deviations (positive reading is consistent with sequential expansion). If that expansion were to turn more convincingly higher, the obvious concern would be that the US economy is growing at a pace that risks generating second-round effects from the energy price shock. That concern is only reinforced by the fact that ISM prices paid printed at 84.6 on Friday…the highest level since May 2022.

Source: Dallas Fed

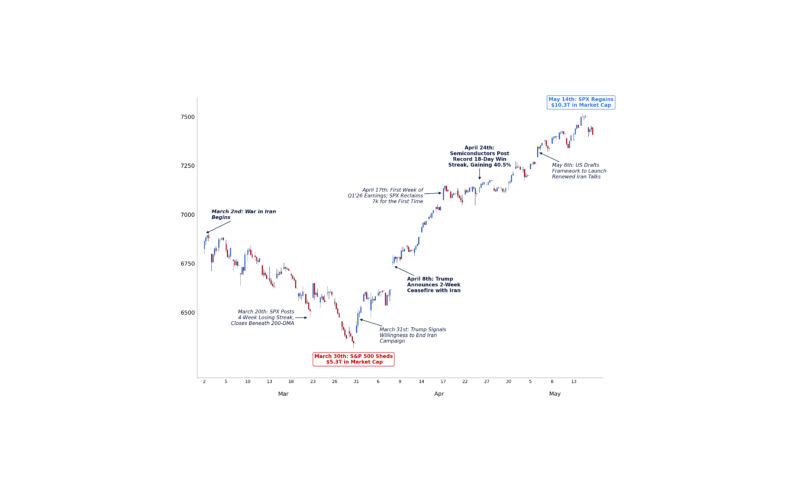

ON THE CONFLICT ITSELF…I stand by the principle set out in my note of 4th April – both sides are unwilling to take the next step of escalation…and both superpowers are keen to find a resolution. Does that mean we won’t see further kinetic action? No…it’s certainly plausible that we have another flare up, but critically, it’s unlikely to involve ground troops…something which POTUS has shown no desire for recently…especially prescient given the murmurings in Congress – important in the context of us being on top of the 60-day War Powers deadline since the conflict started. In the absence of ground troops, another round of air strikes is unlikely to change the Iranian’s mind on the nuclear program or other remaining issues. And I also expect any retaliation to be limited in nature, without risking escalation into energy infrastructure or water desalination plants. Spot crude oil prices remain ~50% higher than pre-conflict and Dec-26 futures are trading ~$85/bbl. indicating concerns around persistence. I cannot see President Trump risking a further increase with little further to gain through escalation…especially with average gasoline prices at the pump well above $4.00. So, the greater issue is now this: the conflict subsiding leaves US growth fundamentals intact…but with a higher starting point for inflation. The potential for a de-anchoring of inflation expectations and second round effects that feed through into core from a classic demand-induced inflation process is real. That is a problem for the Fed.

Source: Bloomberg, Citadel Securities

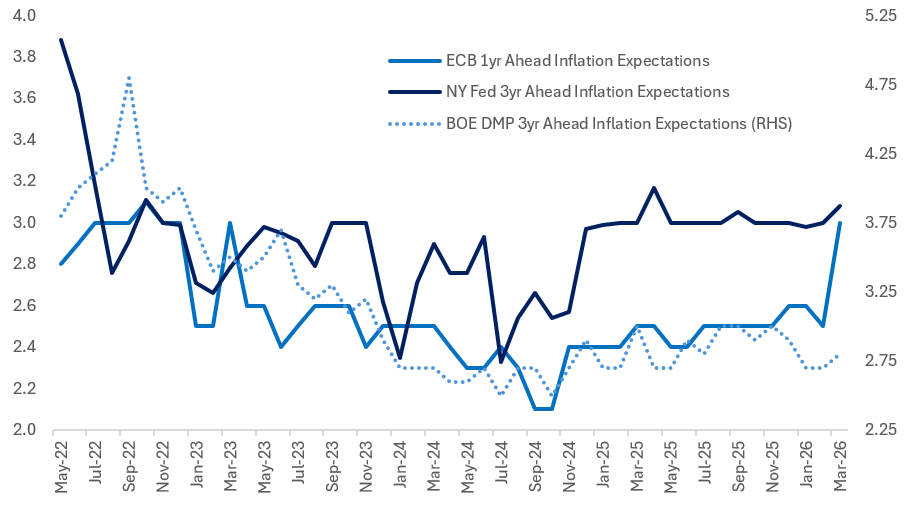

I HAVE ARGUED THAT CENTRAL BANKS WOULD LARGELY LOOK THROUGH THE INFLATION SHOCK…since the backdrop is very different from 2022. That view seems broadly consistent with the message from the major central banks this week with the headline takeaway from the Fed, ECB, and MPC essentially being ‘on hold for now’. The ECB still looks set to hike in June, which makes sense given that it has the lowest policy rate of the three and has been clear that policy is not yet in restrictive territory. The BOE, by contrast, is already restrictive, which limits (though does not eliminate) the risk of further hikes…with Governor Bailey seemingly less concerned about second-round effects in the context of a weak labour market. The Fed also leaned towards a clearly on-hold policy path but retained an implicit easing bias, which drew dissents. Those dissents were focused specifically on the easing bias in the statement reflecting concern from Beth Hammack, Neel Kashkari, and Lorie Logan about guidance that still implied the next move would be a cut. In general, the Fed typically moves from easing, to easing bias, to neutral, to hiking bias, and then to hiking. This looks like the first step on that path towards a more hawkish stance and suggests a committee that is increasingly worried about the inflation outlook, more relaxed about unemployment, and unlikely to be pushed into cutting rates by a new Chair. Powell’s decision to remain on the Board also matters, because it anchors the FOMC in the status quo approach to policymaking…and even if he keeps a relatively low profile, should provide some counterweight to Kevin Warsh’s influence if it starts to pull policy in a direction that appears disconnected from the data or from an appropriate reaction function. More broadly, I was struck by a consistent message across these central bank meetings: the sense that policy rates are already at least somewhat restrictive, and that tighter financial conditions are doing some of the work of monetary policy. I think that is a mistake. Financial conditions are not imposing additional restraint relative to pre-conflict levels largely because risk assets have performed so strongly. That matters because the inflation outlook has clearly worsened, and in recent days energy futures have moved higher alongside risk assets. This is a major problem for central banks because it reinforces the demand side of the economy and points to a robust growth outlook in the middle of a headline inflation shock. A strong demand environment combined with a headline inflation shock raises the probability of second-round effects feeding into core inflation. Inflation expectations, at least as measured by the major central banks, are already beginning to rise. On that front, I think both central banks and markets still look too relaxed.

Source: Bloomberg, Citadel Securities

WHAT DOES THIS ALL MEAN FOR ASSET PRICES? An environment of easy financial conditions, a supportive fiscal impulse and robust corporate earnings is generally bullish for stocks. This is especially true given institutional investor sentiment has not yet peaked and de-risking around the Iran war likely means equities remain under owned. For now, labour market conditions remain sanguine enough not to warrant concerns around wage growth…ECI data for Q1 had wages and salaries at 3.4%, still far off the peaks of 2022 above 5%. Upcoming jobs data in coming months will determine if this changes enough to justify a more hawkish shift that would put a spanner into the works for risk assets. Bonds remain caught between inflationary risks and de-escalation. My view remains that we can continue to see a supportive environment for both fixed income and equities in the short-term because I’m optimistic on the end state of the conflict. However, the balance of the economic data will determine if risk-parity can perform in the medium-term.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/