American exceptionalism is rooted in a deeply embedded culture of innovation, adaptability, and optimism. This entrepreneurial spirit is most visible in America’s small-business sector, which accounts for nearly 44% of GDP and employs more than 60 million workers. It may also become a unique advantage in the age of AI enablement. America’s entrepreneurship is more than a cultural abstraction; academic research has linked optimism to measurable economic behavior. Self-employed workers are more optimistic than wage earners, while more optimistic individuals tend to work harder, expect longer careers, and take more idiosyncratic risk in their investment portfolios. Thus far, the AI theme has been framed around frontier labs, hyperscalers, and bottlenecks in compute. We think an equally powerful focus is what AI does for the builders, founders, and small businesses that drive such a large share of the economy. By reducing minimum efficient scale, AI can allow smaller companies to unlock economies of scale earlier, expand with less friction, and compete in markets dominated by far larger organizations. Automation can reduce the labor intensity of certain tasks, but in an economy with unusually high entrepreneurial velocity, it can also broaden the range of viable enterprise. That dynamism is an important counterweight to AI displacement risk. In fact, AI may pay its greatest dividend by compounding America’s hustle culture: lowering the cost of business formation, increasing founder leverage, and turning the country’s instinct for innovation into new economic activity. To be clear, productivity gains take time to accrue, and the market is right to ask hard questions about capex ROI and Tokenomics. Over time, however, we think AI-enabled entrepreneurship will be one of the most durable themes in the space.

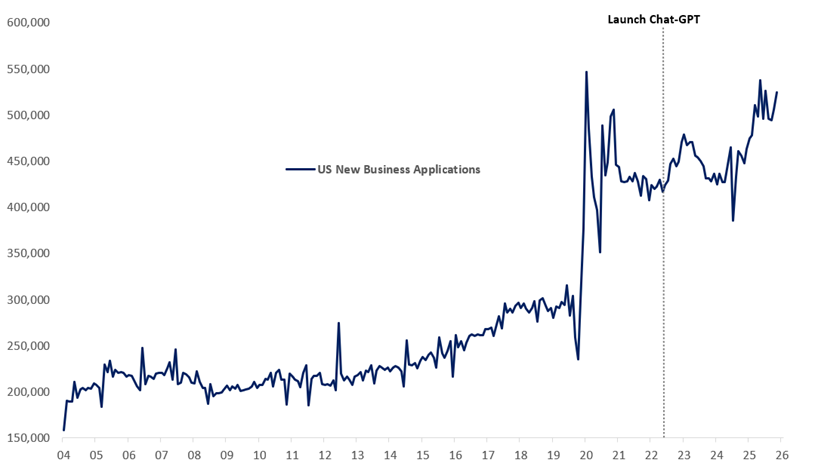

New Business Applications Are Surging Higher

New Business Applications: Total for All NAICS in the United States

Source: FRED, US Census Bureau, Citadel Securities

Nothing underlines this more clearly than the surge in new business formation in recent years, which is up 24% since the launch of ChatGPT. Indeed, when business formation is split by sector, there appears to be a positive correlation between new business creation and sector-level AI exposure. In other words, the sectors most exposed to AI are also seeing some of the strongest formation impulses, suggesting that AI is lowering the barriers to business formation and compounding what America does best: innovation.

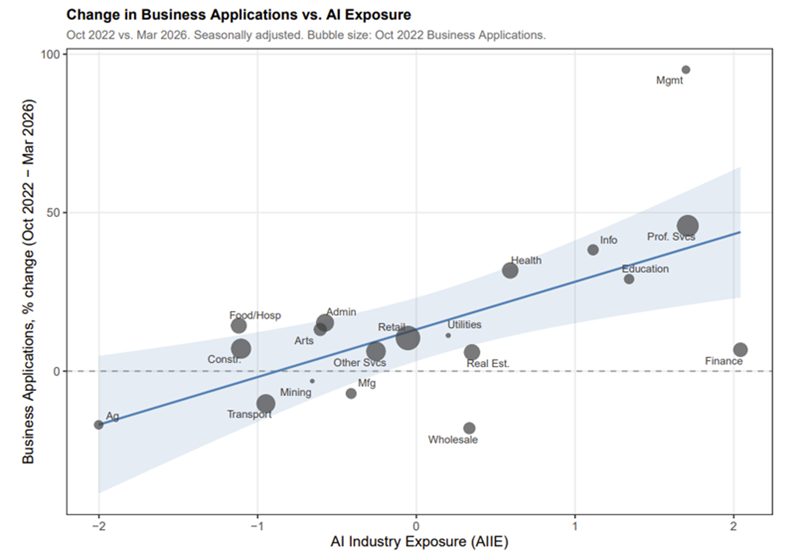

New Business Formation Appears Positively Correlated with AI Exposure

Change in Business Applications vs AI Exposure, Oct-22 vs Mar-26

Source: Guillermo Gallacher’s calculation based on Census Bureau Business Formation Statistics and Felten, Raj & Seamans (2021), paper link

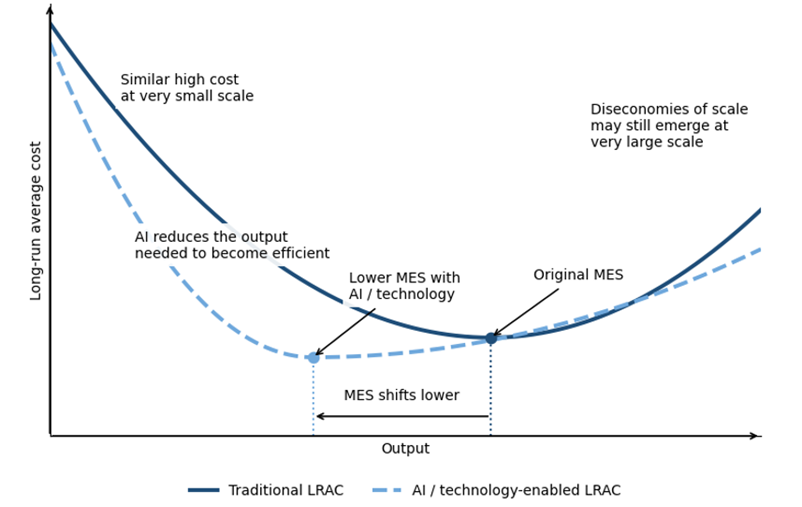

Efficient, cost-effective AI can derisk the process of business expansion by making previously uneconomic work and hiring decisions economically viable. In economics, minimum efficient scale is the smallest level of output at which a firm can operate at low average cost. AI can lower that threshold by allowing small teams to pool capabilities/resources across functions that previously required separate hires, systems, or departments, from coding and marketing to customer service, analytics, compliance, and administration. Rather than being forced to take on leverage to grow quickly, small businesses can expand organically because new projects that were previously non-economic become viable via resource pooling. For example, a small business that needs but can’t afford an accountant, supply chain manager, and office administrator may be able to pool hiring across roles because AI allows workers to be more productive and expand the range of the tasks they perform. Expanding the scope of a role may make a hiring decision that previously didn’t add up, economically viable.

AI Reduces Minimum Efficient Scale Unlocking Economies of Scale Earlier

Long Run Average Cost vs Output, Traditional and AI/Tech Enabled, Theoretical Diagram

Source: Citadel Securities

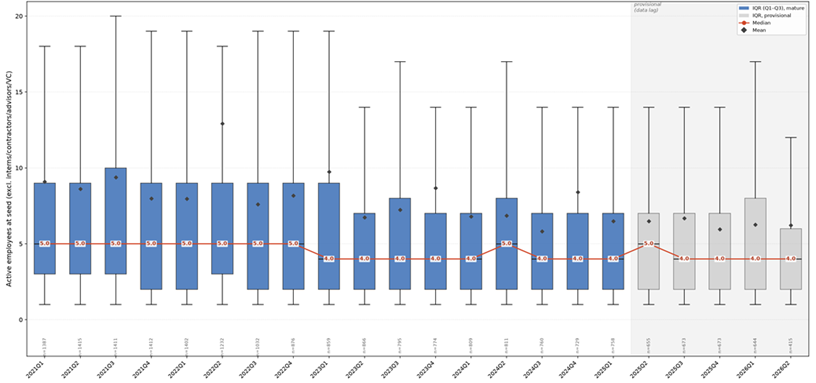

To understand this theme further, we turned to our largest external shareholder and partner Sequoia to gain insight into the median number of employees at start-ups at seed stage. The Sequoia data implies that the median number of employees at seed round declined from five to four in Q1 of 2023, just one quarter following the launch of Chat-GPT. Naturally – this was also a period in which interest rates were rising and metrics of overall hiring demand were softening, but we think AI likely plays some role here in providing founders with more leverage and eventually driving the increase in new business formation we now see in the economy wide data.

Sequoia Data Implies a Decline in Median Number of Employees at Seed Raise

Active Employees at Seed Raise, US Companies

Source: Sequoia Capital

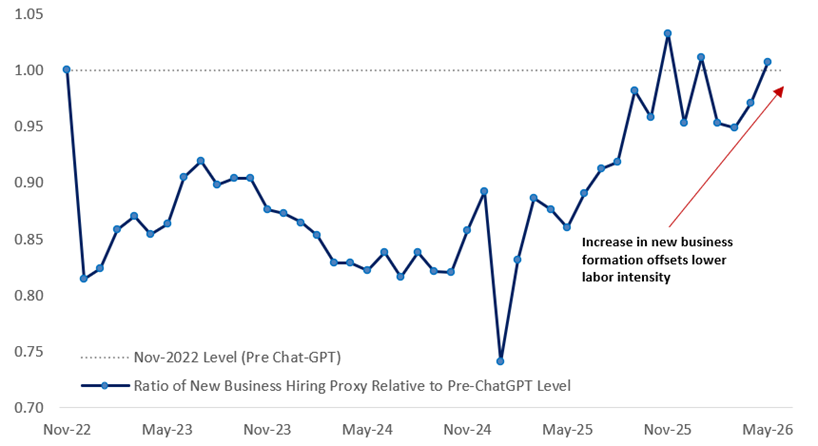

The natural next question is therefore – does this imply broader risks of labor market displacement? We think not. If we use the Sequoia median employee data as proxy for the labor intensity of economy wide new business formation, we can then calculate a rough approximation (median employees x new business formation) of the net employment impact of lower labor intensity vs more new business formation. This *rough* approximation implies that the expansion of new business formation may now fully offset lower labor intensity and implied new business hiring slightly exceeds its level Q4-2022 level, following an initial dip.

More New Business Formation Now Offsets Lower Labor Intensity

New Business Formation x Median Employees at Seed Round

Source: Sequoia Capital, US Census Bureau, Citadel Securities

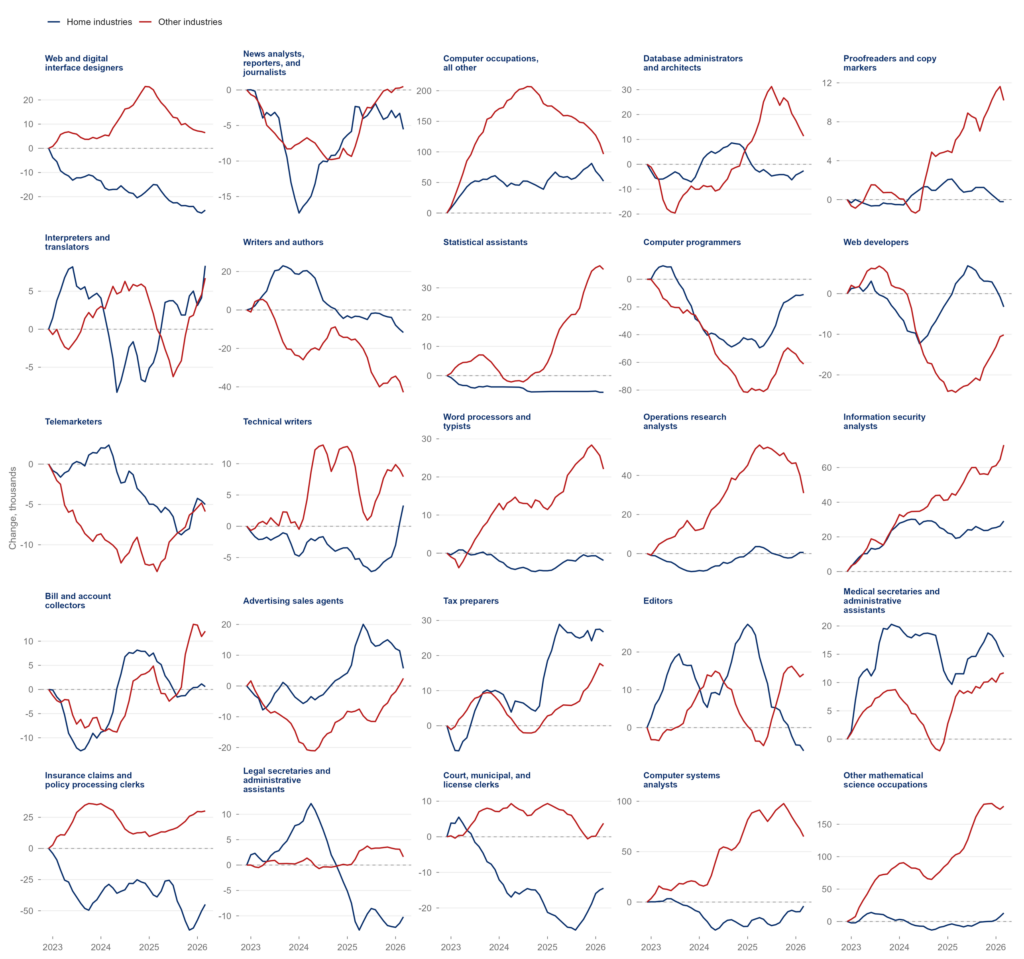

To understand the prevalence of this cross hiring/resource pooling dynamic in the broader economy,

we combine over 2.3 million individual-level employment records from the CPS survey’s monthly microdata, spanning from January 2022 through March 2026, with Budget Lab’s PCA composite AI exposure scores assigned across 541 occupations. We use these data to explore shifting employment patterns across industries and geographies. The analysis is weighted throughout by CPS sampling weights, reconciles a mid-sample industry classification break, and interpolates the October 2025 data that are missing due to a government shutdown. Ultimately we use this data to understand whether AI-exposed occupations show observable reallocation of employment across industries and geographies. We characterise this is as home vs non home hiring – an example of which would be a law firm hiring a software engineer, or a media firm hiring a cyber security analyst rather than the software engineer working at a tech firm or the cyber analyst working at an information security company. We find that there are strong home/non-home effects among the most-exposed industries, but not in all of them, validating the idea of cross hiring as a function of AI, and a real time example of Jevons Paradox, whereby a productivity boost results in more hiring in AI exposed sectors. Using the same micro data, we also find that AI-exposed employment growth is happening in areas with the lowest concentration of AI-exposed workers, again indicative evidence that AI may make whole swathes of previously unviable work economic.

Evidence of Cross Hiring in AI Exposed Occupations

Change in Employment since Dec 2022 (’000s), Home vs Non-Home (Other) Industries

Source: IPUMS CPS, Budget Lab, Citadel Securities

We conclude that, despite legitimate anxiety around AI displacement risk, the US economy’s extraordinary capacity to innovate, augment, and adapt leaves it uniquely well positioned to capitalize on the gains from artificial intelligence. Those gains may accrue most powerfully to the bedrock of the American economy: small businesses and entrepreneurs. The acceleration in new business formation, particularly in AI-exposed sectors, is a material counterweight to declining labor intensity and underscores the economic importance of a growing, rather than fixed, pie. Our findings of significant hiring in AI-exposed roles outside their traditional home industries is consistent with both Jevons Paradox and the resource pooling that AI facilitates. In effect, AI allows businesses to access scale economics before they have fully scaled, pooling capabilities across functions and lowering the output threshold at which expansion becomes economic. Never bet against America.

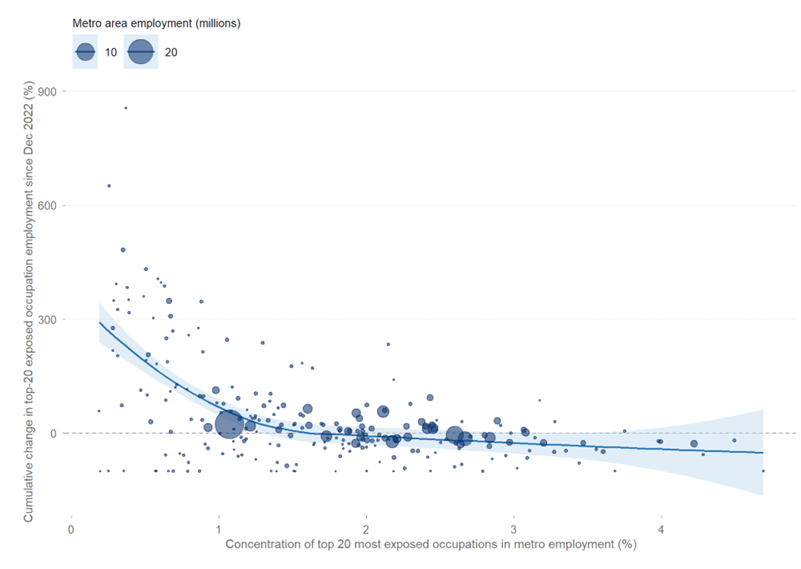

AI Employment Growth is Happening in Areas with Lower Concentration of AI-Exposed Workers

US Metros, Top-20 Exposed Occupations, Dec 2022 to Latest 12m

Source: IPUMS CPS, Budget Lab, Citadel Securities

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.