We continue to see two rate hikes this year. We retain the baseline of those hikes likely coming at the September and December meetings, but think that the market is underpricing the probability of a July hike. Investors still appear anchored to an inertial framework, in which the Fed is assumed to move gradually and only once the data have fully forced its hand. We think the pivot from inertial to adaptive policy-making is likely real and underappreciated. In an adaptive policy-making framework, the optimal strategy for a central bank would be to respond quickly to deviations from the dual mandate before that deviation becomes entrenched, thereby signaling to economic agents such deviations will not be tolerated. This means that wage and price-setting behavior is more likely to embed a 2% inflation expectation, which in turn would make realizing that target more likely, and ultimately would require less forceful action than tightening later, as would be implied by an inertial policy framework. We think the market reaction to the June FOMC meeting, which saw breakeven inflation decline (albeit alongside oil), the curve flatten, the dollar strengthen, and the dip in risky assets quickly unwound, represents an A+ grade for Chair Warsh’s first meeting from a markets perspective. It should embolden the shift from inertial to adaptive policy-making by demonstrating that delivering a short, sharp succession of credibility hikes is digestible for markets, even if they are not fully priced ahead of time. Passing up the first opportunity to “do as you say you will” risks making Chair Warsh’s June presser look performative, and could see the market unwind some of the new found credibility-premium.

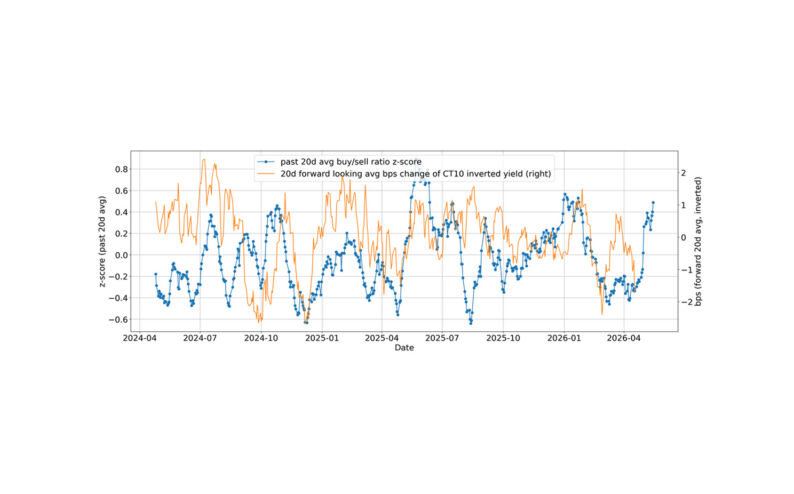

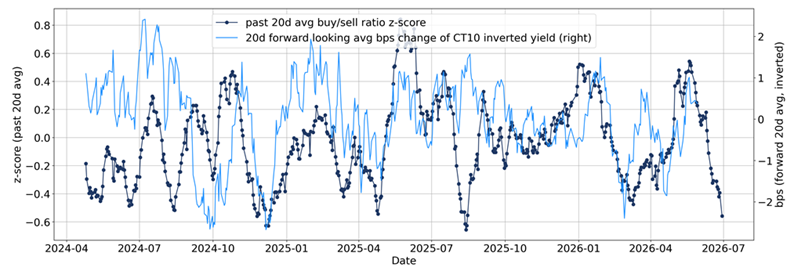

UST Flow Analysis Implies Net Selling and Upside Risks to Yields

20d Average Buy/Sell ratio Z score and CT10 20d Avg Change in Yield (Inverted)

Source: Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

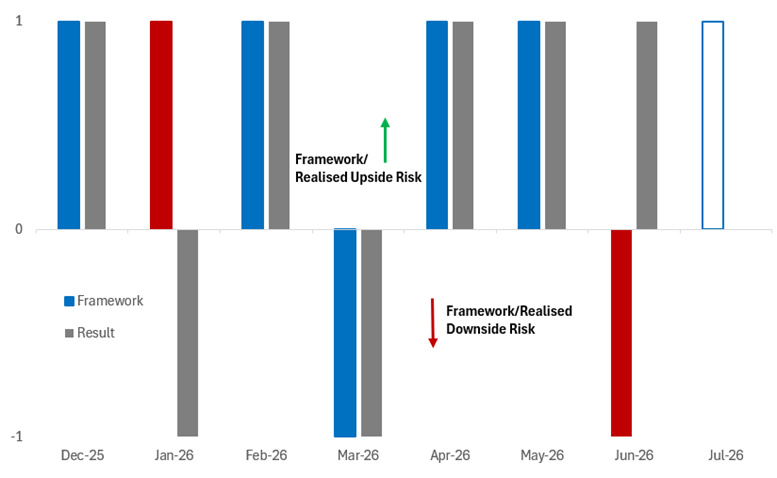

We see upside risks to the June employment report. This reflects both a perceived upside skew in our framework for the payrolls print, which has a 71.4% out-of-sample directional hit rate (flattered by short sample lookback), and the relatively low bar for the unemployment rate to round down to 4.2% from 4.296%, given the strong run of US labor market data over the past three months, and the lagging nature of the unemployment rate. Relatedly, we think consensus assumes that part of the strong May jobs number reflected one-off World Cup-related hiring, and hence will not be repeated in June. However, looking at the leisure and hospitality sector data on a non-seasonally adjusted basis suggests the strength hiring in May appears to have been driven by calendar factors, as it was broadly in line with an average May print in recent years and implies limited excess hiring from the World Cup. As a result, we expect the World Cup boost to show up in the June print, which aligns more closely with the start of the tournament.

We See Upside Risks to June Employment Report

Directional Lean of Our NFP Framework, Historical Performance vs Realised Outcome

Source: Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

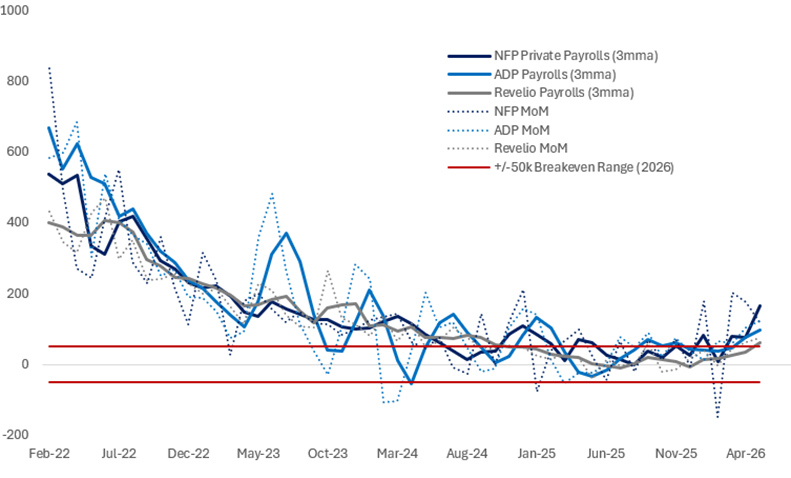

Labor Market Tracking Points Shows Rebound in Hiring

3mma of NFP, ADP, Revelio Payrolls

Source: Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

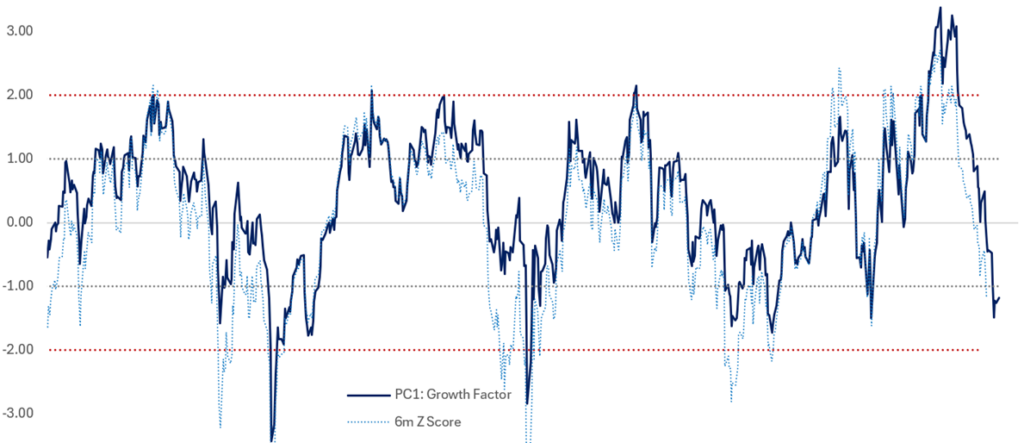

On 19th May, we wrote that there were risks of a snap richer in global duration because of the confluence of two factors in our macro framework. First, our cross-asset decomposition had flagged an apparent unstable equilibrium between equities and rates, based on the valuation of its PC1 growth factor, which had reached the >+2 sigma reversal threshold, implying downside risk to yields. Second, our UST cash flow data showed a material increase in net buying intensity in fixed income. The 19th May marks the year to date peak in yields, however both bullish duration factors have now fully reversed (see charts above and below). The PC1 in our macro framework has moved over 3 sigma in recent weeks to its current -1.17 sigma reading, while our UST cash flow data now points to a step-up in net selling intensity, as demonstrated in the first chart. Together, these signals may imply upside risk to yields from here.

The Growth Factor in our Macro Framework Has Normalized as Yields Have Rallied

First Principal Component of our Cross Asset Macro Framework

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results. *Note we have tweaked the specification of our cross-asset framework to include inflation products since our latest update, the above charts reflect that improved specification.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.