Recent price action reflects a realization that the market has undersized the compute requirements of AI adoption. This aligns with the argument we introduced earlier this year that the constraints on AI were likely to be physical in nature, centering on compute and power scarcity, rather than model ability as the limiting frontier. We sense early incremental shifts away from the heavy consensus of AI displacement towards a more nuanced understanding of how AI will affect the economy. We see four key components of this: 1) compute demands scale quadratically with task complexity 2) which in turn may limit the likelihood of generalized labor displacement but instead makes 3) AI more likely to be a complement to labor and existing workflows (/software) which in turn may imply that 4) the theoretical and historical grounding that technological enhancements are generally good for growth, hiring, wages and living standards – as demand is generally elastic. We see the more significant challenge to the AI theme as one of front loaded and massive investment requirements, which sit juxtaposed to a payoff structure that accrues over decades in terms of true adoption and productivity gains. Ultimately, many iterations of technological innovation have kept real-per-capital GDP growth at around 2% for the last 125yrs, and we’d hope AI is powerful enough to extend that trend further, despite aging populations (material displacement offset) and deglobalization.

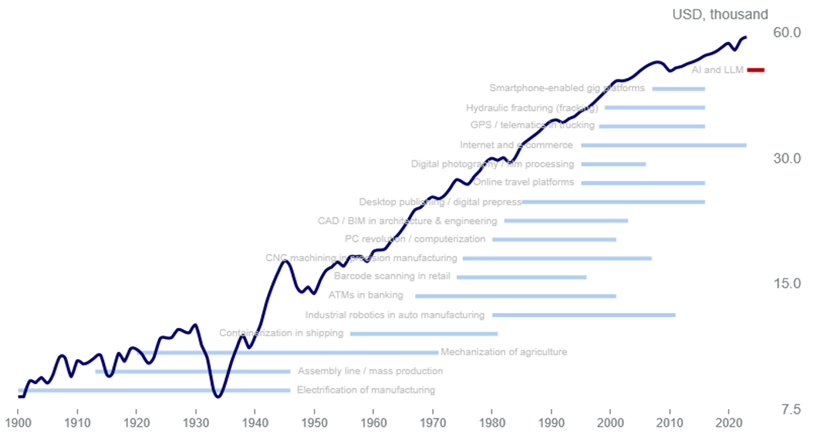

Decades of Technological Innovation Has Kept Real-Per-Capita Growth Around 2%

United States, GDP per Capita, log scale vs historical productivity shocks

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Compute Intensity is a Limiting Factor

As models improve, agentic workflows are deployed, adoption increases and tasks become more complex, token usage and inference demand could increase significantly. The higher total token cost is becoming a much more salient focus for investors, and should further challenge the generalized displacement theme in labor markets, but the same too applies for software. Agentic workflows require long-running, multi-step workflows that preserve state, call tools, branch, backtrack and operate over very large context windows. These processes scale compute intensity in a non-linear manner because AI models work via inference, the process of generating each next token by running a forward pass through a very large neural network over the full active context. In practical terms, the model must repeatedly read, score and transform all relevant prior inference steps while also deciding what to do next, which tool to call, whether to revise an earlier step and how to maintain coherence across the workflow. As context windows expand and reasoning chains lengthen, both memory use and compute per task rise materially, often more than proportionally, because the system is not just producing an answer but continuously reprocessing a growing history of instructions, intermediate outputs and retrieved information. That means more capable, more autonomous systems sharply increase compute demand, pushing token consumption and inference costs higher as model quality improves.

This dynamic is most obviously captured by suggestions (link, link) that upcoming models could be multiple orders of magnitude more compute intensive than current generation models, largely because the tasks they undertake are so much more complex. This happens despite the fact that frontier models appear to achieve improved efficiency on a per-token basis – performing reasoning with significantly fewer tokens than predecessors, yet this gain is fundamentally eclipsed by the sheer scale of the tasks it is designed to handle, because new models are built for multi-hour autonomous missions rather than brief chat interactions, they operate within massive, high-entropy context windows where the computational cost scales aggressively. Consequently, the move from simple queries to deep, agentic problem-solving drives a massive spike in resource requirements.

There are risks that firms are making strategic decisions with an unrealistic understanding of how expensive AI-augmented workflows will be to deploy and this may lead markets to focus not simply whether models are getting better, but whether the cost of supplying frontier intelligence is falling fast enough relative to the cost of labor to make large-scale substitution economic. To illustrate the point on compute intensity, consider the Uber CTO’s remark: “I’m back to the drawing board because the budget I thought I would need is blown away already.” Those comments were reported on April 14. Even with incomplete information, a simple back-of-the-envelope calculation is suggestive: if the budget had effectively already been exhausted only 28.5% of the way through the calendar year, that would imply a spending run rate of roughly 3.5x the pace originally expected, assuming the budget was set on a calendar-year basis.

Jevons Paradox: Economic Theory Leans Against Displacement

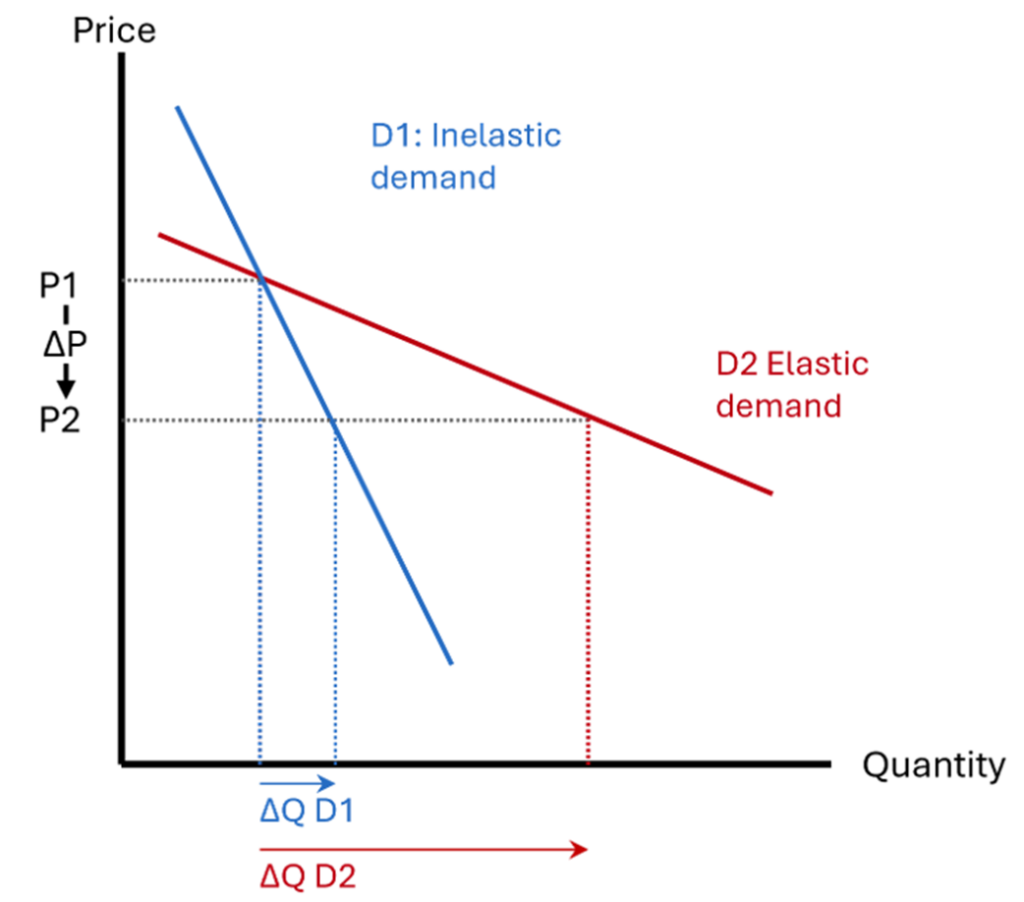

That said – there are clear and numerous ways in which AI can be applied cost effectively as a complement rather than a substitute for labor. AI can deliver efficient and round the clock performance in repetitive processes and give significant leverage by up-skilling workers, that in turn iterate and underwrite multi-stage context windows to deliver the fast and compute efficient improvements many of us are seeing in our day to day work. Economic theory implies that this should expand demand for labor (and software) by driving efficiency gains that in effect reduce costs of production. In resource constrained economies, if demand is elastic then you generally see a material increases in the total quantity consumed of a good/service, if it becomes more efficient/cost effective. This concept is called Jevons Paradox – and it was first observed in the context of the steam engine in England in the 19th century, after an improvement in the coal efficiency of the steam engine resulted in an increase rather than decrease in the total consumption of coal. The parallel for labor here is quite clean in that one can see AI as improving the efficiency of labor meaning that firms consume more labor because its effective cost per unit of work falls and wages are unlikely to adjust quickly. The obvious applied example is that if a software engineer can do more with AI than previously possible, more firms will hire software engineers because they all of a sudden can achieve outcomes that were previously out of reach for a given hiring budget. One can easily extend this concept to institutional grade software, which with the help of AI can be engineered and offered more cheaply, and demand from small businesses could explode. Similarly if AI allows high end software to be more customized and unique, firms will likely pay up for a better product from their existing providers. Its not clear that general-purpose agents will economically disintermediate existing software at scale as many software workflows are deterministic, repetitive and cheap to serve and hence do not require a persistent high-compute reasoning engine sitting in the loop. In those domains, incumbent software may remain much more economically viable than an expensive agent. Quality, maintenance, AI-cyber resilience, off the shelf customizability and price can become the new moat.

Elastic Demand Results in Large Quantity Expansion

Impact of an Exogenous Price Change on Quantity in Different Elasticity Scenarios

Source: Citadel Securities, Apr-26. Figures are for illustrative purposes only.

Labor Demand in AI Exposed Sectors is Rising

Whilst it may seem counterintuitive relative to the lived experience of how powerful AI tooling is becoming, the reality is that there is very little evidence of labor displacement at scale in the economic data thus far, and actually where we do see evidence of the impact of AI, it looks more consistent with our view that AI is a complement rather than a substitute for labor.

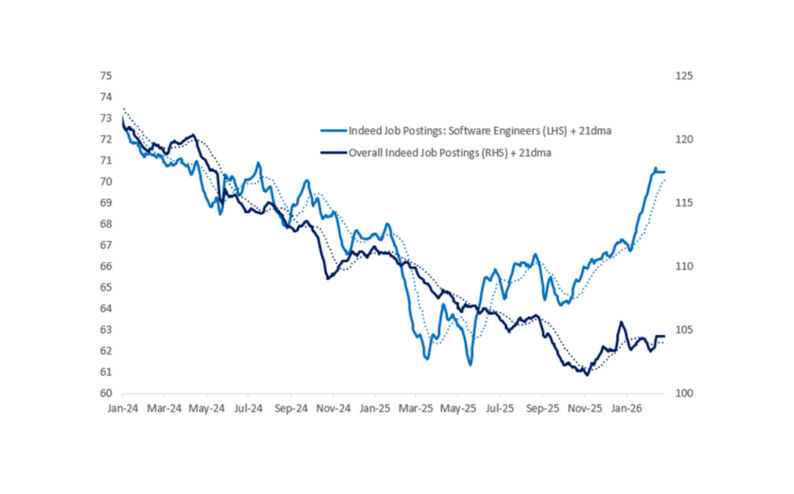

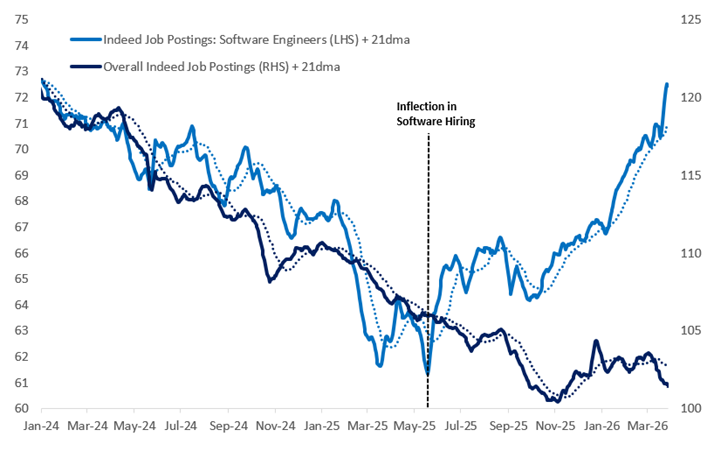

Job Postings in AI Exposed Industries are Rapidly Rising

Indeed Daily Job Postings for Various AI Exposed Industries

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

We illustrated back in February that demand for software engineers, the most AI exposed occupation was accelerating higher, which we argued violates the displacement narrative. Indeed the acceleration in software job postings has continued, now up 18% from the inflection point in May last year.

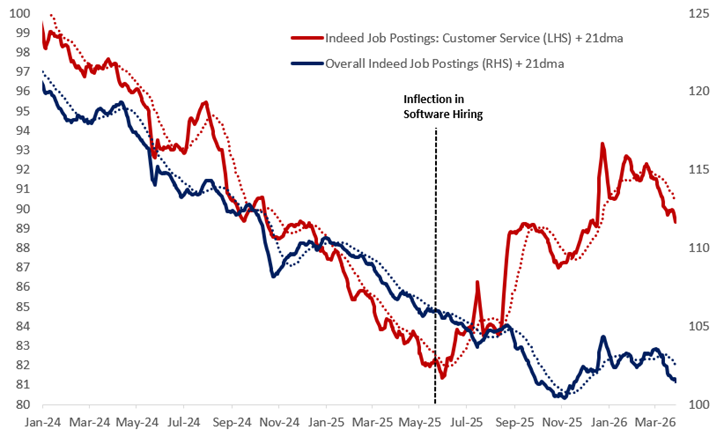

Job Postings in AI Exposed Industries are Rapidly Rising

Indeed Daily Job Postings for Various AI Exposed Industries

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

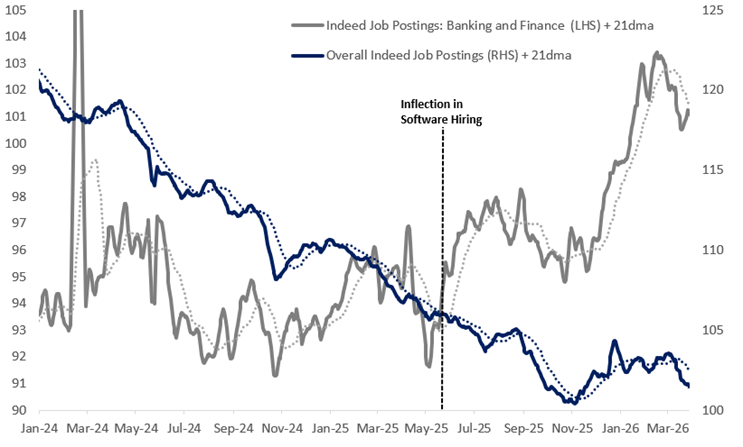

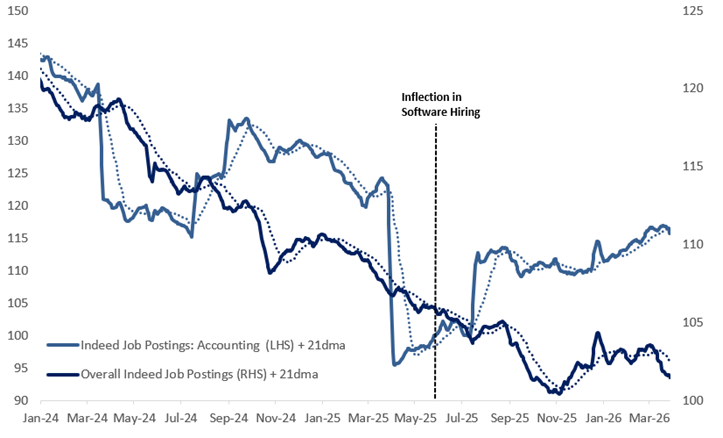

However a thoughtful pushback was that perhaps increasing demand for software engineers reflected a short term dynamic in which engineers were hired to integrate AI into workflows, which would then allow displacement thereafter. To investigate this we can turn to daily job posting data in the remainder of the top five AI exposed industries. We find that job postings in customer service are up 9% from when software postings started to inflect higher in May-2025, in banking and finance postings are up 9% and in accountancy are up 18%.

Job Postings in AI Exposed Industries are Rapidly Rising

Indeed Daily Job Postings for Various AI Exposed Industries

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

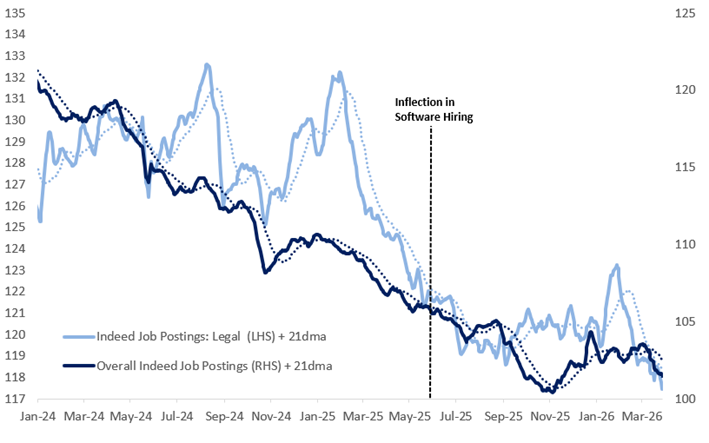

This is striking in the sense that job postings in these sectors are not just up relative to overall job postings but up in absolute terms, despite overall job postings being down 4%. Legal job postings are down 4%, in line with overall postings.

Job Postings in AI Exposed Industries are Rapidly Rising

Indeed Daily Job Postings for Various AI Exposed Industries

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

The synchronicity in the inflections higher in AI exposed hiring, implies that as AI capability rises, firms are expanding the amount of work they can productively undertake in these domains rather than collapsing headcount.

Job Postings in Law Are In Line With Overall Trends

Indeed Daily Job Postings for Various AI Exposed Industries

Source: Bloomberg, Citadel Securities, Apr-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Moreover there is increasing evidence that AI is driving significant hiring in construction- in line with our views from earlier in the year, as the data centre built out is very labor intensive, but also that AI is resulting in job creation and new company formation. We can complement the analysis in our previous work that showed an acceleration new business formation with a contribution from Guillermo Gallacher that shows there is a positive correlation between AI exposure and new business formation in those industries, underlining the theory that AI is making activity that once failed to clear expected value thresholds economically viable, by reducing costs of production and barriers to entry. This is consistent with findings from LinkUp reported by the WSJ that imply AI has already created 650k jobs, and implies that on net, reports of AI related layoffs (which are likely more a function of over-hiring/overspending on behalf of management anyway) are being more than offset by AI related hiring.

Source: Guillermo Gallacher’s calculation based on Census Bureau Business Formation Statistics and Felten, Raj & Seamans (2021), paper link

The Economic History of Technological Change

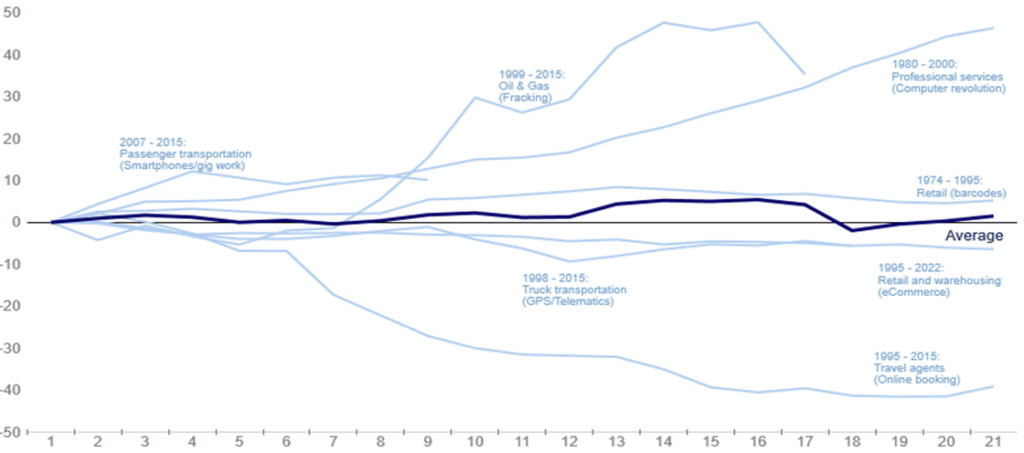

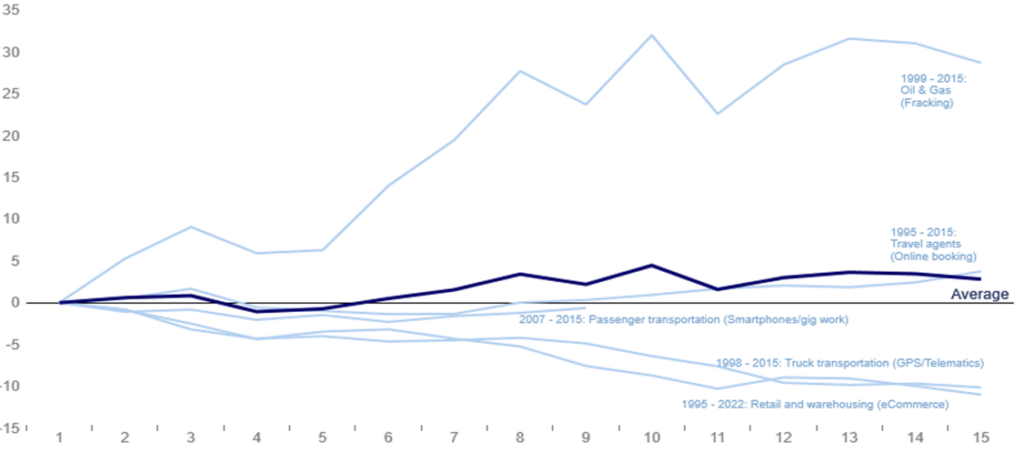

The economic history of technological change implies it is – on average – net positive for labor. To illustrate this point, we use BLS data for the last c.50 years to understand how hiring and wages behaved during sector specific technological shocks. We study 7 sector specific shocks, index each sector’s share of total private payrolls at the point of arrival of the new technology, to understand how hiring in that sector responded relative to the overall economy. We find that on average relative hiring increases over the period of adoption. We also find that on average relative wages rise slightly, which makes sense as technology gains that increase the marginal product of labor, which over the long run is the key determinate of wages.

Technological Change Appears to On Average Increase Hiring

Cumulative Change in Industry Share of Total Private Payrolls

Source: BLS, Citadel Securities. Figures are for illustrative purposes only.

Technological Change Appears to Drive Wages Higher on Average

Cumulative Change in Relative Hourly Earnings by Industry

Source: BLS, Citadel Securities. Figures are for illustrative purposes only.

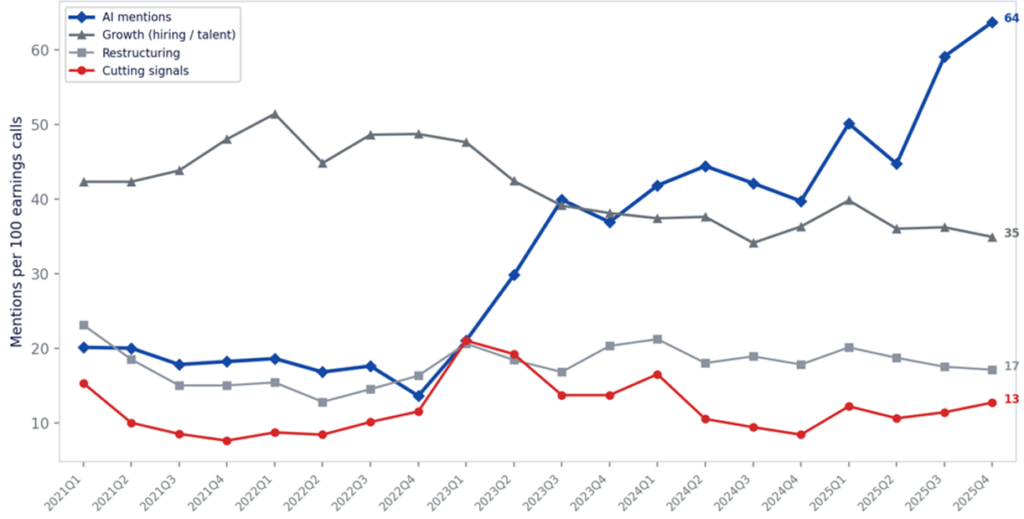

How Do Executives Frame AI/Labor on Earnings Calls?

Given the theoretical, historical and spot data precedents all lean away from the AI displacement risk and more towards the labor complementary argument, the bar to think this time is different should be relatively high. To understand the risk that this time is different, we think it makes sense to investigate what companies, on aggregate, are saying about AI displacement risks.

We use newly developed in house technology to ingest and read 9,646 S&P 500 earnings call transcripts. We use key word analysis and semantic classification techniques to return structured data to understand how corporate executives frame the interaction between AI and labor (complement/substitute/neutral) across job functions and time.

We find that AI mentions on S&P 500 earnings calls grew materially over the period, from 20% to 64%. This acceleration began in earnest in 2023Q1 (ChatGPT launch), meanwhile workforce signals imply stability in labor trends. Our analysis finds that labor cutting signals (layoff, severance, hiring freeze, etc.) peaked at 21% in 2023Q1, then subsided to 13% by 2025Q4. Labor growth signals (hiring, talent) have drifted from 42% to 35% and restructuring language remains steady at 17%, suggesting very little change in labor market trends, despite a material acceleration in management focus on AI.

AI, Hiring and Layoff Mentions on S&P 500 Earnings Calls

Mentions of Various Topics on Corporate Earnings Calls

Source: LSEG StreetEvents Transcripts as compiled by Citadel Securities, as of April 2026.

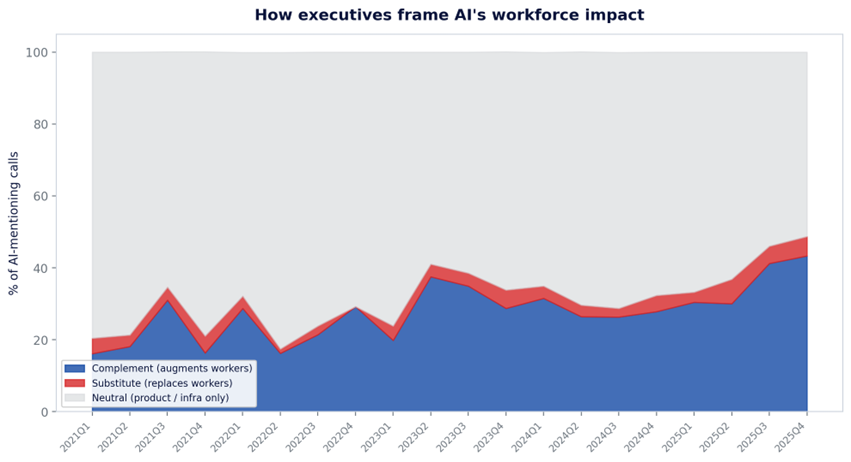

Among earnings calls that mention both AI and workforce/efficiency terms we find 58.4% of all S&P 500 earnings calls in 2025Q4 discussed AI in a workforce context, up from 17.1% in 2021Q1. The most important consideration here is how management teams characterize the relationship between AI and labor. If AI is framed as a complement to labor, it suggests firms see it as enhancing worker productivity and potentially supporting labor demand. If it is framed as a substitute, it implies potential labor displacement and weaker labor demand. We find that complement framing dominates substitute framing by a ratio of ~8:1, with 43% of firms framing AI as a complement to labor, 51% framing it as neutral for labor and just 5% framing AI as a substitute for labor. Our analysis is consistent with our priors that executives are framing AI as a tool that makes their existing workforce more productive, not as a replacement.

Executive Framing of The Impact of AI on the Workforce

Contextual Framing on Earnings Calls of Impact of AI on Workforce

Source: LSEG StreetEvents Transcripts as compiled by Citadel Securities, as of April 2026.

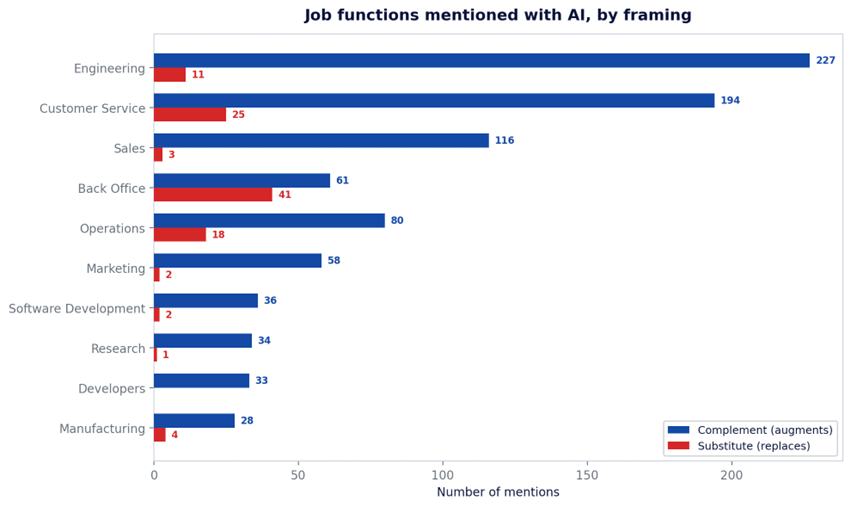

Furthermore, we find evidence of Jevons Paradox in the earnings call data, where increased efficiency leads to more resource consumption, not less: as calls concurrently mentioning AI and hiring/talent had surged to 26.0% of all calls by 2025Q3. We also find that AI and workforce language is not evenly distributed. Extraction of specific job functions mentioned alongside AI implies engineering is the #1 function mentioned with AI, overwhelmingly as complement. Companies are hiring engineers because of AI, not despite it, whereas back office function have the highest substitute ratio, but even there we still see a larger share of firms framing AI as a complement to those functions.

Job Functions Have Different Exposure to AI

Contextual Framing on Earnings Calls of Impact of AI on Workforce: By Sector of Work

Source: LSEG StreetEvents Transcripts as compiled by Citadel Securities, as of April 2026.

Conclusion

The economics of frontier models, the increasing importance of compute and power, and the current labor-market evidence, read alongside economic theory and historical experience and all seem to lean against the consensus view that AI will result in broad labor displacement. It may be more accurate to think of AI as a high-capability, high-marginal-cost technology whose efficiency gains expand demand for intelligence faster than they compress the cost of supplying it, so that the first-order consequence is not substitution away from labor, but a broader increase in demand for compute, power, infrastructure, and the many forms of complementary labor. There is nothing especially anomalous about that pattern in historical context: over the course of more than a century the global economy has absorbed electrification, mass production, mechanization, industrial robotics, personal computing, the internet, and smartphones without derailing long-run growth or making human labor obsolete. The history of technological change is not one of a fixed pie with a shrinking share attributable to labor, but instead of a growing pie, in which new technologies expand capacity, enlarge the productive frontier and leave the economy larger than before.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.