We have argued for some time that agentic and complex workflows delivered by frontier models would be expensive to run, constrained by physical bottlenecks, and vulnerable to unrealistic expectations of frictionless deployment cost. That judgement now looks less contrarian than it did when we first set it out in February. Amazon has now removed its token leaderboard, Microsoft has cancelled Claude Code subscriptions, and there have been multiple reports of unexpectedly large token bills. The salient point is that even the most powerful technologies must pass through the prosaic discipline of cost curves, capacity constraints, and marginal returns. Adoption is therefore becoming less about what frontier models can do in principle and more about the price and scarcity of the inputs required to make AI operational at scale. Compute, power, cooling, memory bandwidth, and inference budgets are real and binding constraints.

Economic theory tells us that prices perform three basic functions: they signal scarcity, create incentives for substitution, and ration scarce resources toward their highest-value uses. These functions apply clearly to AI. Higher compute and inference costs signal the scarcity of the underlying inputs; they encourage substitution away from low-return experiments and toward more efficient models or workflows; and they ration scarce capacity toward the areas where the marginal productivity of AI justifies the marginal cost of using it. We do not think this implies that the frontier of inference-intensive AI will be abandoned, only that it is likely to be concentrated among a narrower set of firms with the balance sheets to absorb the compute cost, the research depth to deploy it effectively, and, most importantly, the operating domain to scale the rewards from solving genuinely hard problems. For the economy at large, simpler models may be the more cost-effective, productivity-augmenting pathway until physical constraints are eased. We hence see growing signs of a bifurcation in frontier vs “everyday” AI usage.

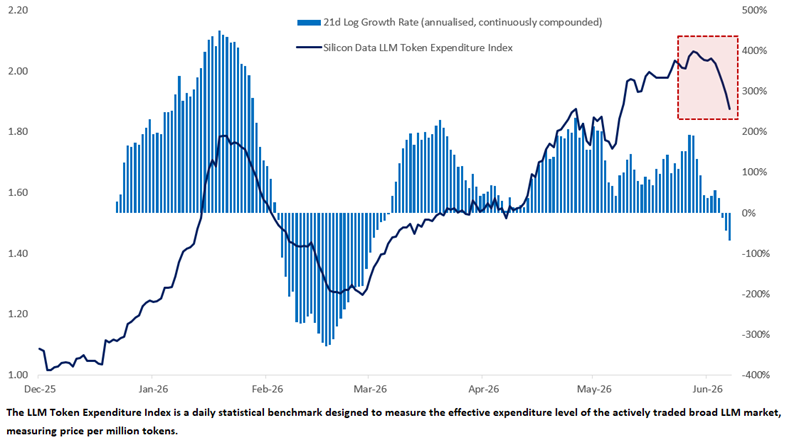

Recent Token Expenditure Index Declines May Reflect a Shift to Cheaper Models

Silicon Data LLM Expenditure Index, Level and 21d Log Growth Rate (Annualized)

Source: Silicon Data, Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

The recent decline in the Silicon Data LLM Expenditure Index, which measures the price and mix of LLM token usage, may reflect some of this shift toward cheaper models. Silicon Data notes that “the index can…fall when individual model prices decline, when users substitute toward more efficient model choices, or when the market diversifies away from expensive concentration.” That interpretation is consistent with the broader view that rising sensitivity (elasticity) to the all-in cost of AI deployment (token price x token volume) is pushing users toward cheaper or more efficient models where the frontier technology is not required. It also helps explain why falling token prices need not contradict rising demand for AI infrastructure: in an elastic market, lower unit costs can unlock additional usage, even as the composition of that usage shifts toward cheaper and more efficient systems.

We remain constructive on the terminal outcome of AI as a productivity-enhancing technology, but note the route to that value is likely to be more selective and cost-conscious than markets once assumed, and that may be relevant for asset prices. As we have argued in prior work on AI and labour markets, the key variable is not productivity alone, but the elasticity of demand for the tasks and services whose costs are falling. Where demand is elastic, AI-enabled efficiency gains can expand output enough to raise demand for complementary factors of production, such as labour. That is why the most durable and scalable productivity gains thus far appear to come from embedding AI as a complement to human labour: developers using coding assistants to accelerate production, documentation, testing, and debugging; customer-support agents using copilots to resolve cases faster; and knowledge workers using models to compress search, drafting, translation, and analytical preparation. These are narrower, more disciplined, and more token-efficient applications than the vision of autonomous agents running everything everywhere all at once. Over the medium term, improvements in model efficiency, compute, cooling, and power infrastructure can offset some of today’s physical constraints. However markets may do better to avoid anchoring to a world in which AI is ubiquitous, frictionless, and immediate. A more plausible path is uneven diffusion: frontier deployment concentrated where the returns justify the compute, broader adoption shaped by cost and capacity, and asset prices periodically forced to reconcile ambition with physical constraint.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.