MARKETS REMAIN TOO COMPLACENT ABOUT THE RISKS FROM THE IRAN WAR. My focus is on the forward path for markets and asset prices, rather than on the politics. There is an old adage that “anything worth doing is hard” and we are seeing that play out in real time. There is another that says, “hope for the best, but plan for the worst”. Market participants would be wise to take heed of this in the current landscape for the purpose of risk management. Investors have been conditioned to fade the impact of geopolitical shocks which typically have a fleeting impact on the economy and asset prices. But this conflict in the middle east carries with it a unique macro risk – sustained disruption or closure of the Strait of Hormuz – which is extremely harmful and disruptive to the global economy should the war continue for months (rather than weeks). As a reminder, this key passage for global trade sees over 20% of the world’s supply of crude oil (as well as refined products) flow through it. Continued Iranian drone attacks on shipping have severely disrupted traffic through the Strait…with the new supreme leader Mojtaba Khamenei vowing to continue his strategy to exert upward pressure on oil prices, which have settled above $100 (the highest since 2022)…despite the coordinated release of 400 million barrels from strategic reserves by the US and 32 other IEA member states (including 172 million barrels from the US SPR). Prices remaining elevated despite this intervention highlights the scale of the shock. Global oil demand is running above 100 million bpd…if the current disruption implies a supply shortfall on the order of 15-20 million bpd, that translates into a cumulative deficit of ~200 million barrels since the war started. Strategic reserves are simply not enough to offset a prolonged closure of Hormuz. Naval escorts for tankers face material operational risks amid ongoing drone attacks and threats of mining in the Strait. As such, a durable reopening likely requires de-escalation rather than purely military solutions. Whilst President Trump hinted at this earlier in the week, I struggle to see an imminent off-ramp…especially if US strategic objectives have not been met. Regime change does not seem likely, nor unconditional surrender…reports suggest that the IRGC maintains control of the streets and there is little in the way of an uprising that some had expected. History suggests this will be difficult without boots on the ground, which is possible, but would lead to further escalation and take months, if not years, to achieve – with consequences for US public opinion. There may also be divergence between US and Israeli objectives, complicating strategy…continuing aerial bombardment is not without long-term consequences…leaving a failed state with no clear plan risks a huge country filled with hostile militias, which would create an entirely new risk premia for the broader region, including nearby GCC countries, that would remain susceptible to continued attacks. These countries have been dramatically impacted by this conflict – stability and security have been at the heart of their economic diversification strategy – now at risk should this conflict endure. A fundamental re-assessment of their approach to defence is likely needed going forward. For Iran, survival is the objective…while much of its conventional capability may have been degraded, it retains asymmetric tools…including relatively inexpensive drones that can impose outsized economic costs by targeting energy flows. The cost asymmetry is important…low-cost drones (~$30,000 each) versus high-value interceptor and cruise missile systems (Tomahawks at $3.6 million each). The continued pace of Iranian drone strikes suggests they still retain meaningful supplies, whilst reports estimate the US has used 168 tomahawks in the first 100 hours of the war (annual US procurement has been less than 100 in recent years). Moreover, the Pentagon has stated that the war has cost $11bn in the first 6 days. At this juncture, I don’t see President Trump calling a halt to this war without further progress on strategic objectives (even Iran’s enriched uranium remains intact). At the same time, Tehran will want to continue with asymmetric warfare, disrupting energy markets and therefore the global economy, in the hope of exerting enough pressure to reach some sort of negotiated settlement including ceasefire guarantees. In sum, absent de-escalation, the longer the Strait remains severely disrupted, the greater the risk of a sustained energy shock with global macro consequences.

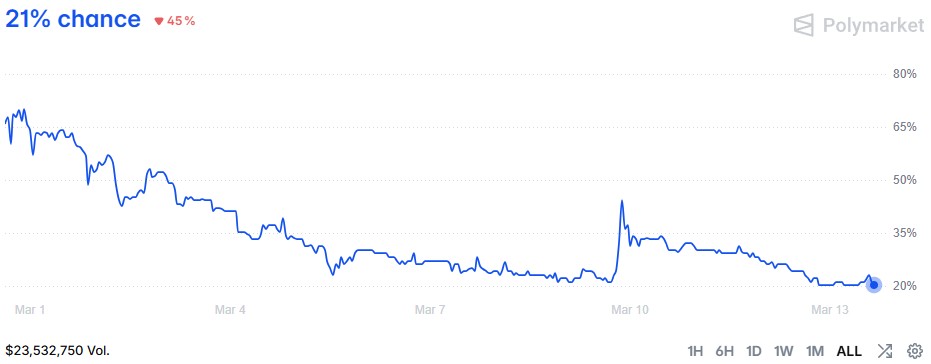

Odds of ceasefire by 31 March

WHAT ARE THE ESCALATION RISKS? First, an attack on Kharg Island oil facilities, which handle around 90% of Iran’s crude exports. Friday’s attack was focused on military targets, but threats to oil infrastructure would heap further pressure on energy markets and represent a further expansion of the conflict, given its consequences for rebuilding any future Iranian state. Second, the East–West Saudi pipeline is now a key route to the Red Sea and can be surged toward ~7 million bpd. A direct attack on this pipeline would not only exacerbate supply constraints, but risks drawing Saudi directly into the war. Third, the Houthis, widely regarded as an Iranian proxy militia, have yet to be meaningfully activated; most likely, they could be used to constrain international shipping in the Red Sea, further impacting global trade. Fourth, direct attacks on oil production facilities in Saudi and elsewhere remain on the cards if escalation ensues. And finally, strikes on water desalination plants…the lifeblood of civilian infrastructure across the GCC, where countries rely on desalination for the vast majority of drinking water…would cast a long shadow over daily life, far beyond the current strains of persistent drone attacks. Whilst I am not proposing that any of these are imminent, investors should be alert to the risk that this conflict could easily worsen, especially if the Iranian leadership becomes more desperate for survival under continued bombardment.

Source: Citadel Securities, Bloomberg

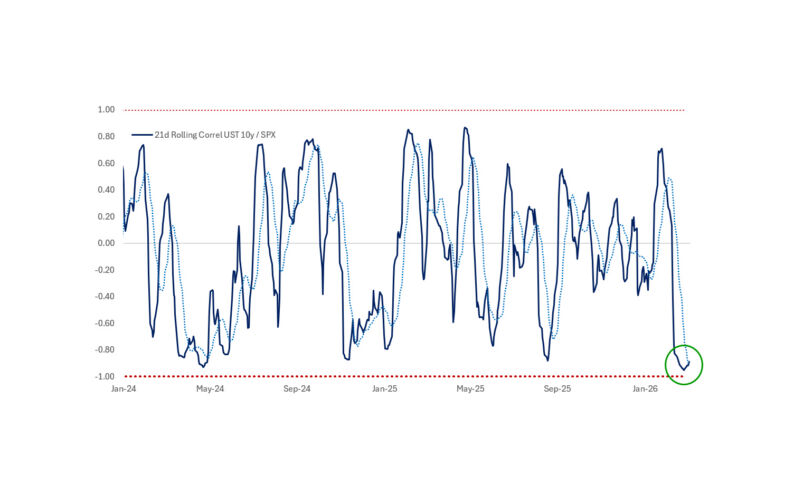

GLOBAL RATES MARKETS HAVE REACTED IN A BROADLY APPROPRIATE FASHION. Front-end yields are no longer pricing much in the way of rate cuts in 2026, reflecting elevated risks of a sustained inflationary shock. This week’s data was a timely reminder that inflation is likely to remain well above target for some time. With February Core PCE likely to come at 0.4% MoM (3.1% YoY), following a similar print in January, it would require meaningful disinflation over the coming months to reach the Fed’s 2.5% year-end forecast. Troublingly, progress on goods disinflation appears to have stalled, while services inflation remains sticky. And this is before incorporating any impact from the conflict. The war affects not only energy prices, but food…the Strait of Hormuz carries roughly one third of global fertiliser trade…critical to agriculture. Gulf states account for ~50% of global urea production and ~30% of ammonia. Continued disruption would constrain availability and drive prices higher, with potentially significant consequences for crop yields and global food prices…a concerning echo of 2022 following Russia’s invasion of Ukraine. This is clearly a political risk for President Trump and the GOP ahead of midterms where “affordability” is likely to be a key issue…but it also complicates the Fed’s task. Whilst the FOMC would likely look through first-round effects from an energy-induced inflation shock, if inflation expectations were to become unanchored, policymakers would be forced into a more hawkish stance, particularly given inflation is still running ~1% above target. This is why we are starting to see financial conditions react and tighten (albeit from very easy levels). Against a backdrop of large fiscal deficits and heavy gross Treasury issuance, the risk that long-end yields demand a higher risk premium in response to recent events continues to be high.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/