THE MIDDLE EAST WAR REMAINS THE DOMINANT THEME IN GLOBAL MARKETS…despite attempts at de-escalation. As I have been writing about since before the conflict started, a geopolitical shock of this magnitude risks blowing off course the trajectory of global growth and inflation…and we are seeing exactly this play out in recent weeks. Investors conditioned to “buy-the-dip” have underestimated both the magnitude and ramifications of a prolonged energy price shock. Whilst there is now a clear desire to bring an end to the kinetic phase of this war, the reality is there are no good options for a quick cessation of hostilities. Leaving the Strait of Hormuz, the key bottleneck in global trade in energy, to effective Iranian control is unacceptable to the US and much of the rest of the world. Equally, it seems unlikely that the Iranian regime will agree to any US ceasefire plan without security guarantees. So, what we’re left with is a classic escalation trap – something I discussed in last week’s note. Each side ratchets up the conflict in the hope that one final surge will push the opponent to back down; but instead, this is viewed as aggression, justifying a larger response, increasing violence on both sides. This continues beyond the point at which the original strategic benefits of the war are exceeded by the costs. Recent news of an even larger US troop deployment (up to 10,000 more to the region) with the potential for a ground operation, continued drone and missile attacks by Iran, and reports of the Houthis entering the conflict with risks to the Bab al-Mandeb Strait all suggest we are still caught in this trap. My mantra throughout this crisis has been ‘follow the troops, not the tweets’…and I think this remains true. Risk markets continue to underestimate the peril of a long conflict without a clear endgame and the impact of a sustained energy price shock. This is a very different crisis compared to last year’s tariff disruptions, which was both one-sided and financial in nature. Damage to physical energy infrastructure and global trade supply chains will take months, if not years, to repair. Whilst the US economy has unique strengths which afford great resilience, it is not entirely immune. The implications for growth, inflation, consumer sentiment, and ultimately corporate earnings will be profound should this crisis endure.

Source: Morning Consult

FOR CENTRAL BANKS, THIS REPRESENTS A SIGNIFICANT CHALLENGE, SIGNALLING A STEP CHANGE IN THE PREVAILING NARRATIVE COMPARED WITH THE PRE-CONFLICT PERIOD. The risk is that inflation expectations become elevated, forcing policymakers to lean in a hawkish direction. But this is not 2022…the current conditions create a meaningfully different backdrop: the starting point of policy rates is higher…there is no post-pandemic re-opening boom….excess savings are not high…and we are unlikely to see a globally co-ordinated fiscal impulse. Instead, the risk this time is a substantial hit to growth at the same time as rising inflation => stagflation. The worst outcome for central bankers right now would be a significant rise in survey-based inflation expectations in the face of weaker growth dynamics. Thus far, the reaction we have seen is how you’d expect any central banker to respond – respect the fact that conditions have changed and stand ready and willing to fight any sustained move higher in core inflation. Front-end policy rate expectations have responded in kind, pricing in almost 3 rate hikes from the ECB and BOE by year-end and no further cuts from the Fed. But the hit to growth muddies this picture – damage to risk appetite, the feedback loop from tightening financial conditions and the non-linearity associated with a prolonged move higher in energy prices means that aggressively tightening monetary policy may exacerbate financial stress in the economy, with highly uncertain second round effects. In sum, I expect demand destruction to happen in both scenarios should this war continue for much longer…either from central banks that are forced to hike rates assertively to challenge spiralling inflation expectations…or from a large hit to growth from a persistent energy price shock. There is only one circuit breaker to this crisis: rapid de-escalation. This is not a financial shock; it’s a physical one. Nowhere is this more evident than in the AI theme, whose fulcrum is energy. Damage to physical infrastructure, rising premiums for reliable power, concerns over middle eastern data centre security, helium shortages, and broader supply chain disruptions all leave this theme vulnerable to a further tightening in global financial conditions. We are not out of the woods yet.

Source: Bloomberg, Citadel Securities

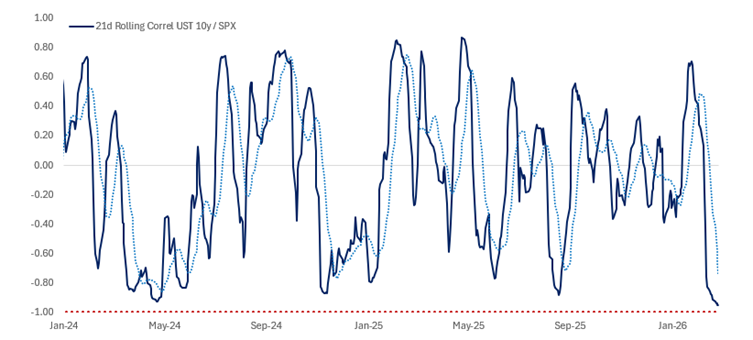

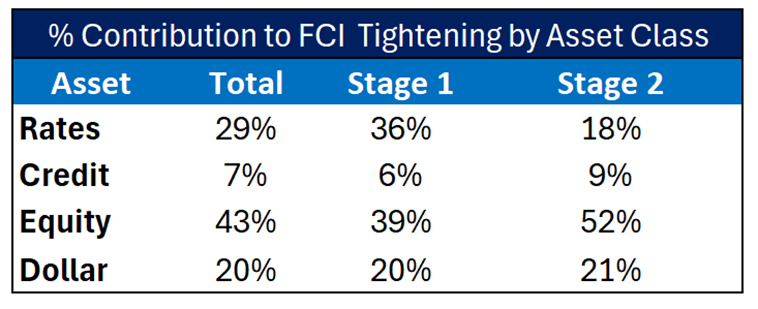

MARKETS HAVE SO FAR FOCUSED ON THE INFLATION SHOCK…which makes sense as the first-order implication from this crisis. This is observable in the extreme move in stock–bond correlations, which reached -0.95 on a 21-day rolling basis (equities down, yields up). Such extremes in realised correlation often mark turning points in macro regimes. There are signs we are approaching a shift where fixed income begins to reassert itself as a hedge to risk assets as the extended duration of the conflict implies a more significant impact on growth. This shift is visible in the composition of financial conditions tightening….in the initial phase of the conflict (27 Feb – 25 Mar), rates and the dollar accounted for 56% of the tightening, with risk assets contributing 44%. More recently, the dynamic has changed…risk assets have driven 61% of the tightening, suggesting a transition from pricing an inflation shock to pricing growth risks. On Friday, the contribution from risk assets reached as high as 78% intraday, highlighting how quickly this rotation is occurring. This evolution is consistent with a growing focus on the impact of the shock on consumer confidence, hiring, risk appetite, and supply chains. As these growth concerns come to the forefront, longer-dated fixed income should start to perform as a hedge to risk assets. This marks a change in stance from my previously held view in favour of higher yields given everyone was short the inflation tail. Valuations have adjusted to a point where the feedback loop from higher energy prices into weaker growth has become more material.

Source: Citadel Securities

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/