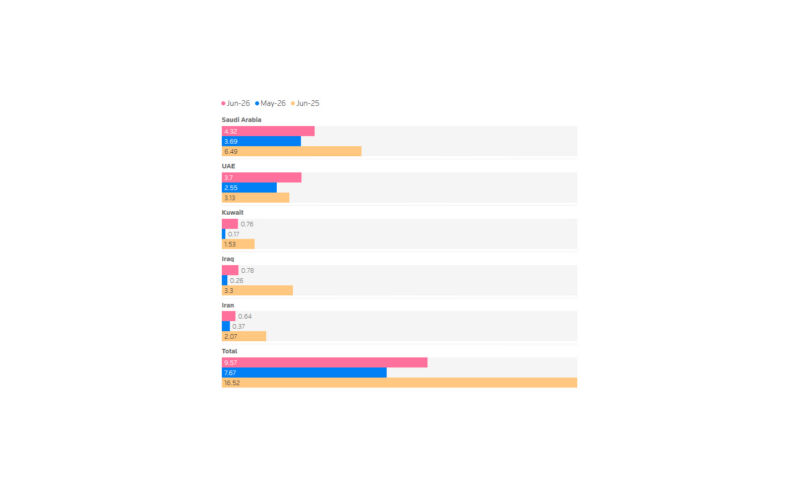

MARKETS ARE STARTING TO WAKE UP TO THE GRAVITY OF THIS WAR IN THE MIDDLE EAST AND ITS IMPLICATIONS FOR ENERGY MARKETS. In last week’s note I highlighted that the market was underestimating risks and identified key escalation triggers, including attacks on energy infrastructure. In recent days, the strikes on Iran’s South Pars gas field and the retaliation on Qatar’s Ras Laffan facility have marked a step-change shift in the magnitude of this conflict and introduced a nightmare scenario for energy markets. This facility provides 20% of the world’s LNG supply and with QatarEnergy confirming “extensive damage”, the implications for natural gas prices are profound. Qatar’s total annual gas production sits at 110bn cubic metres, some of which now faces being offline for months, if not longer. The disruption will sideline 12.8 million tonnes of LNG annually for three to five years and cost $20bn in lost annual revenue. This will dramatically impact European and Asian countries, which rely on Qatar’s supply for the majority of their needs. Investors have been accustomed to fading geopolitical shocks in recent years and have been relatively sanguine about the impact of this current war…predicated on the assumption that President Trump can end the war at anytime and walk away. In my view, this is a miscalculation. Unlike last year’s tariff tantrum, this is not a one-way decision…and even if the US chose to unilaterally depart the arena, the long-term repercussions of this conflict and fragility introduced into energy markets and trade will not disappear quickly. It would also de-facto cede control of the Strait of Hormuz to the Iranians…allowing them to disrupt flows at their will. For Iran, this is an existential conflict. The incentive to sustain asymmetric warfare for months, if not years, is therefore high. Whilst militarily overwhelmed, they have proven to be surprisingly efficient in inflicting enough damage to cause widespread economic disruption. This raises the bar for any ceasefire…one would expect negotiations to hinge on credible, enforceable security guarantees, without which a temporary pause is unlikely to hold. In sum, there is no obvious off-ramp…only the classic features of an escalation trap. Each side continues to intensify the conflict, even as the strategic logic deteriorates, because the cost of backing down – politically, militarily, psychologically – keeps rising. The pattern is familiar…early tactical success (targeting Iranian leadership and military assets)…encouraged further escalation (GCC strikes, threats to Hormuz)…which has now expanded into direct attacks on energy infrastructure in the name of deterrence. But deterrence is interpreted as aggression, prompting further escalation. Each side believes “one more push” will force capitulation; instead, it hardens resolve. Moreover, this is not just an energy story…the war has severely constrained global helium supply (Qatar accounts for roughly one-third of global production), a critical input for advanced semiconductor manufacturing. Helium is notoriously difficult to store, with only ~45 days of buffer in the system, and prices have already doubled since the conflict began. This has direct implications for chip production and the build-out of America’s AI infrastructure. In addition, ~20% of global fertiliser and nearly 50% of urea transit the Strait of Hormuz, posing material risks to agriculture and global food prices. This self-reinforcing cycle of escalation risks embedding a prolonged energy shock, with significant implications for inflation, global growth, and, ultimately, humanitarian outcomes.

Source: Bloomberg, Citadel Securities

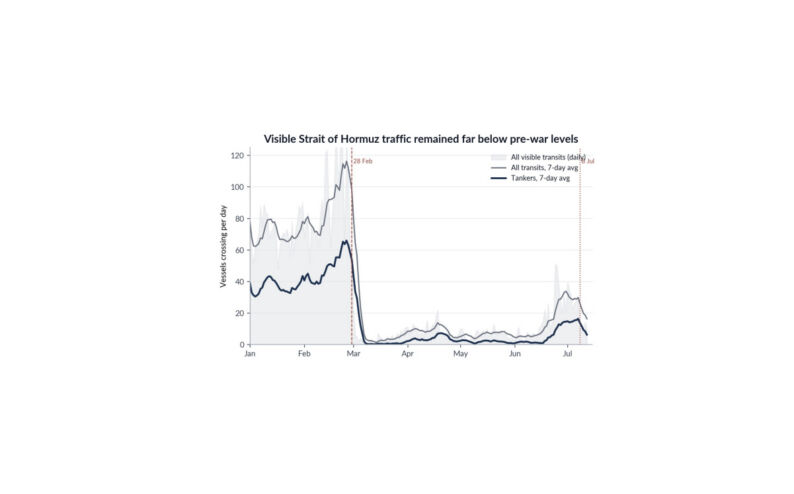

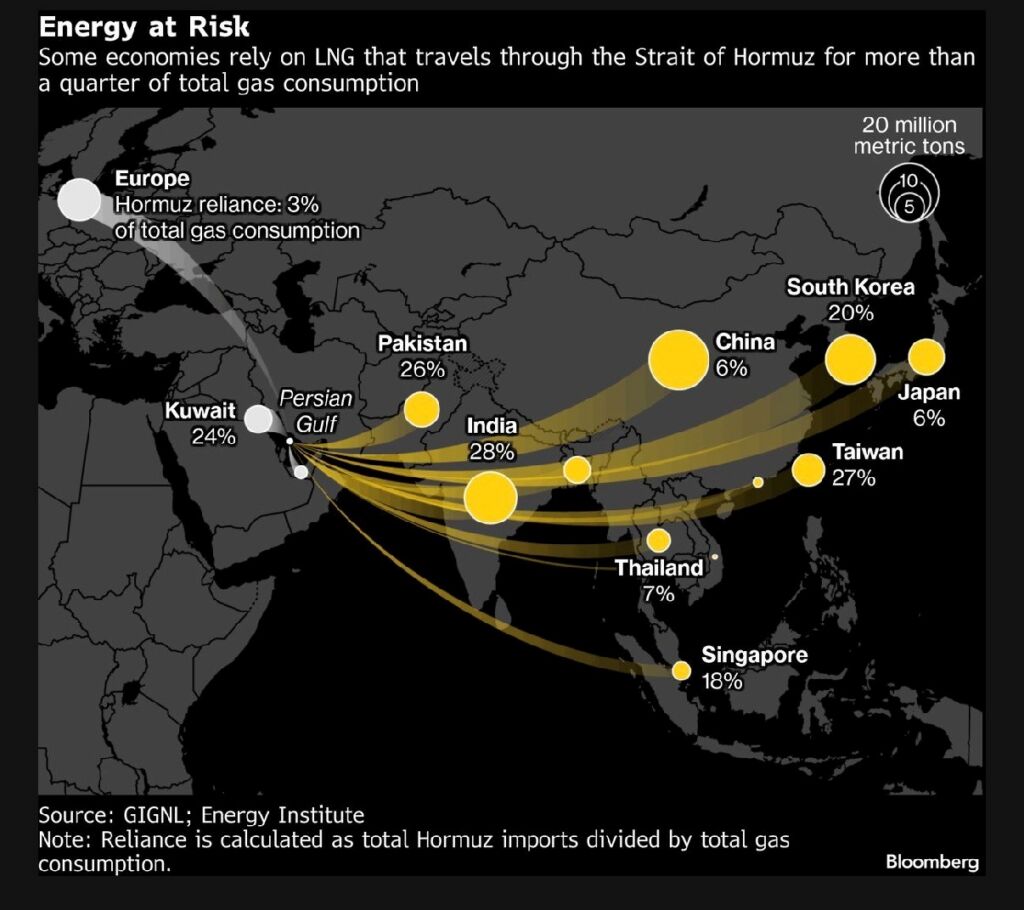

FOR THE GLOBAL ECONOMY, WHAT MATTERS IS THE MECHANISMS THAT COULD MAKE AN ENERGY PRICE SHOCK PERSISTENT. Damage to physical infrastructure like gas fields, LNG terminals, pipelines, and refineries of the type we have seen can take months or even years to repair. This turns short-term disruption into capacity loss. The next crucial factor is the Strait of Hormuz…given the extent of both energy and trade flows that transit this chokepoint, prolonged risk of attacks or closure creates a persistent risk premium, which embeds within prices. Then there is the broader uncertainty injected into this region…energy supply is capex heavy and slow moving, so any investment freeze or reduction in financing due to geopolitical risks can tighten future supply. Ultimately, the risk here is that these factors combine to inject significant volatility into energy market prices, creating a persistent shock through uncertainty, beyond just the level of prices. Simply pulling out the US military will not fix the damage done to global supply chains. Current market pricing implies an inflation shock pre-dominantly, with relatively limited implications for global growth. Central banks are priced to hike rates, on top of already tightening financial conditions…although US risk assets have remained remarkably resilient. The FCI tightening thus far is worth nearly -0.6% of US economic growth, largely offsetting the impact of the fiscal stimulus from the OBBA, and that’s before markets have meaningfully priced-in global growth risks. My concern is that we see contagion from commodities into EM currencies, especially in Asia where dependency on physical LNG imports via the strait is highest. Data from Bloomberg imply that Pakistan imports 26% of its total LNG consumption from tankers that transit the Straits of Hormuz, India 28%, South Korea 20% and Taiwan 27%. Should these currencies continue to depreciate against the dollar, the energy shock could morph into a classic EM crisis. Emerging markets are often hit more acutely because many are net energy importers with currencies sensitive to risk sentiment. Higher dollar oil prices widen current account deficits, trigger currency depreciation, and force procyclical monetary tightening to defend external stability. This tightening, combined with imported inflation, erodes domestic demand and financial conditions…and critically, interacts with large stocks of foreign currency denominated debt (often in dollars), where depreciation mechanically worsens balance sheets, raises debt servicing costs, and increases default risk (where FX mismatches are large) across sovereign and corporate borrowers. As credit risk rises, capital outflows accelerate and local financial systems come under stress, turning the initial terms of trade shock into a broader EM financial shock. It’s important to remember that the US is not immune from these shocks…broad based financial conditions tightening would likely weigh on risk appetite and growth, creating downside pressure on valuations and, over time, earnings expectations. A corresponding move lower in US equities will likely feed into credit spreads and further tighten financial conditions, which in turn will feed negatively into risk appetite driving further dollar appreciation, making the EM terms of trade shock worse…which ultimately feeds back again into advanced economies in a re-enforcing feedback loop. What began as a relative price shock in energy thus propagates through external balances, exchange rates, and balance sheet vulnerabilities into a synchronized global growth slowdown, reinforced by second round effects on confidence, investment, and cross border capital flows and tighter FCI.

Source: Bloomberg

CENTRAL BANKS ARE BEING PRICED TO RESPOND QUICKLY…with UK and Euro front-end rates now discounting the risk of imminent hikes, reflecting their higher exposure to gas prices. The tone from the Fed, ECB, and BOE this week points to a clear willingness to confront this inflationary shock…particularly given concerns around inflation expectations and the elevated starting point for CPI (in the US). There is a sense that policymakers are wary of repeating the mistakes of “team transitory” in 2022 and are determined to stay on the front foot as inflation risks build. However, the current backdrop is materially different. Policy rates are not starting from the zero bound, there is no post-pandemic reopening boom, and governments are not in a position to deliver a pandemic-scale, co-ordinated global fiscal impulse. So, the challenge for central banks is that tightening into a supply shock risks exacerbating an already vulnerable macro backdrop, increasing the likelihood of financial stress. This is not 2022…and it’s important not to fight the last war.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/