Markets are stabilizing following a period of aggressive de-risking. Positioning has reset, sentiment remains depressed, and flows are turning more constructive.

While technicals are not fully healed, the setup is increasingly asymmetric to the upside.

With volatility resetting and macro-driven flows fading, we are seeing a transition back to fundamentals. This shift raises the potential for Q2 earnings to drive outsized moves in a low-positioned market.

I. Citadel Securities Client Flows

We are observing a meaningful inflection in equity flow dynamics, with the market successfully absorbing persistent supply over recent weeks. Defensive positioning has begun to ease, with fewer new hedges being added, though clients remain tactical and well-hedged. Early signs of upside participation are emerging, particularly in higher-quality large-cap growth names.

Retail Cash

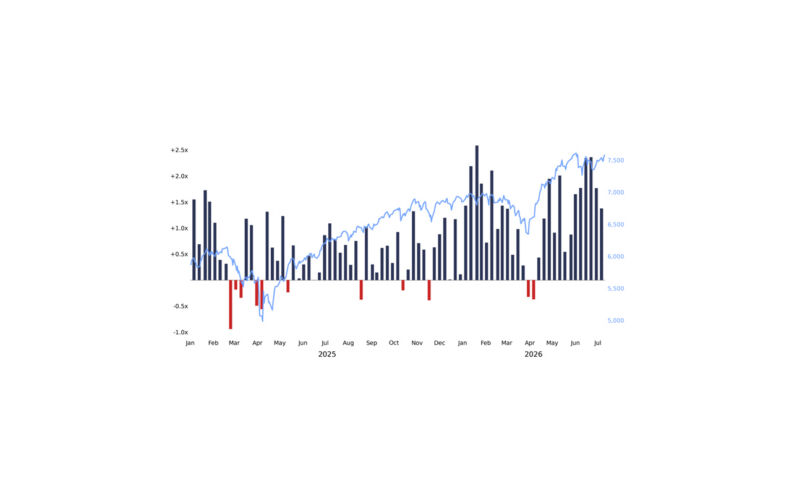

Retail remains a net buyer on the month, but participation has slowed sharply from the record pace seen in January. Net notional spent declined ~55% month-over-month in March and is now down ~70% from January highs.

Even with this normalization, Q1 2026 still ranks as the second-largest quarter of net buying on our platform – second only to Q1 2021. Average daily notional traded last quarter was ~3.3x historical levels, with retail buying in 82% of sessions (vs. a 68% long-run average).

More recently, the tone has softened. Our retail cash platform finished last week net selling, the first such week since November 2025.

As we began highlighting in February, retail has moved away from one-way buying behavior. March data now confirms that shift, with flows turning increasingly contrarian – selling into rallies and buying on weakness. This marks a clear departure from January and February, when retail demand was broadly one-directional to the buy side.

Retail Options

Retail options flows show a similar transition. Activity remains elevated, but positioning has turned more defensive, particularly over the past week.

Flows skewed 4% better for sale last week based on our Call/Put Direction Ratio, the first bearish week since late November, as demand for downside protection has rapidly accelerated.

Put buying has reached extreme levels, with 5-day rolling purchases at record highs. Notably, this hedging demand emerged even during periods of market strength. Between March 27 and April 2 (during which the SPX rose 1.6%), retail spent over $275mm on net put premium – the largest 5-day total in nearly a year, since the week of April 7-11, 2025 (Liberation Day, tariff pause rally week).

Where activity earlier in the year was centered on single-stock opportunities, recent flow has rotated decisively toward index hedging. As highlighted in our monthly Retail Detail: Capitulation Warning, retail is now trading more than 1.5 Index/ETF options for every 1 single-stock option, the highest ratio we have observed and a meaningful departure from the long-run average closer to 1 for 1.

This reinforces the increasingly contrarian nature of retail positioning. The gap between our Call/Put Direction Ratio on S&P up versus down days widened significantly in March: retail was ~7% better for sale on up days, versus ~6% better to buy on down days.

GMI Rules & Tools Backtest: Retail Capitulation

We are now seeing early signs of retail capitulation across both cash and options. Last week, retail flows were net sellers across both platforms – an infrequent occurrence that has only been observed 18 times since January 2020 (most recently the week of April 7-11, 2025).

Historically, forward returns following these signals have been positive on average, with performance improving over longer horizons. S&P 500 returns have been positive ~82% of the time by T+60, with average returns of +4.1%, and average positive returns of +6.9%.

While not a timing signal in isolation, this setup reinforces the broader theme: retail participation is no longer a one-way source of demand, and periods of retail exhaustion have historically coincided with more constructive forward returns.

Institutional Options

Institutional positioning has also leaned defensive, with the shift occurring earlier than in the retail cohort. In early February, we observed the two largest single days of hedge buying from our institutional clients, alongside March expiration ranking as the third-largest put-buying event.

Since then, institutional options flows have remained largely defensive and highly tactical in nature, with activity skewed toward shorter-dated tenors – reflecting the preference for maintaining flexibility (and owning near-dated gamma) amid macro uncertainty.

That said, over the past few weeks, we have begun to see early signs of re-engagement. Dip-buying behavior has started to emerge, particularly in large-cap technology (Magnificent-7), with investors utilizing call spreads to position for a potential rebound. Our Institutional Call/Put Ratio finished last week skewed 2% better to buy amid the strength in the market (“buyers live higher” in this market).

April Seasonality / Tax Day (April 15)

April historically marks a transition in investor behavior, and we are seeing early signs of that shift. Tax-related reallocation flows are beginning to fade, with capital rotating toward forward-looking catalysts, including Q2 earnings and a potential reacceleration in IPO activity.

II. Technical Checklist: Healing, But Not Healed

Our GMI tactical checklist is not fully healed; however, the flow-of-funds backdrop is increasingly skewed to the upside.

Cross Asset Volatility

Volatility is beginning to trend lower across asset classes. Most notably, rates volatility compressed sharply into the end of last week (MOVE ~115 → ~82; 95th → 57th percentile).

Equity implied volatility has also declined, though it remains elevated (SPX 1-month at-the-money IV ~86th percentile). Energy volatility (OVX) has similarly started to come in.

Systematic Exposure

This cross-asset vol normalization is an important signal we are watching closely, as sustained compression in volatility is a prerequisite for broader (systematic) re-risking.

Systematic strategies remain underexposed relative to improving realized conditions, creating potential for incremental buying flows as markets stabilize.

Implied Correlation and Dispersion

Implied correlations have moved higher and single-stock dispersion has compressed, reflecting a shift toward more macro-driven trading.

Dispersion began the year at extreme levels (~99th percentile vs. the last 30 years), before compressing sharply as correlations rose during the selloff – falling to near cycle lows (~12th percentile) amid the onset of geopolitical tensions – and has since normalized back toward long-run averages (~58th percentile).

As correlations stabilize, dispersion will re-expand, particularly into the Q2 earnings season. We anticipate that dispersion by sectors and single names could continue to offer opportunities and challenges (i.e., it is a market of stocks, not a stock market).

Market Structure

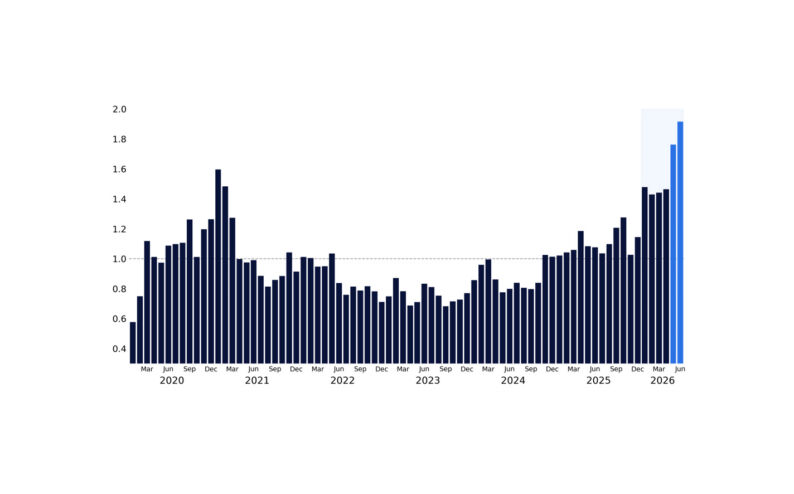

Macro products (ETFs + index-driven flows) continue to dominate both price action and sentiment.

That said, top-of-book liquidity is improving, while macro/ETF trading remains elevated (>35% of total volume). Overall macro-driven volumes have begun to decline in recent sessions.

This points to a gradual normalization in market functioning, though conditions remain somewhat fragile.

Sentiment / Positioning

Investor sentiment remains depressed and has reset significantly from earlier highs.

Historically, this type of positioning backdrop creates a favorable setup for upside convexity as exposure begins to rebuild.

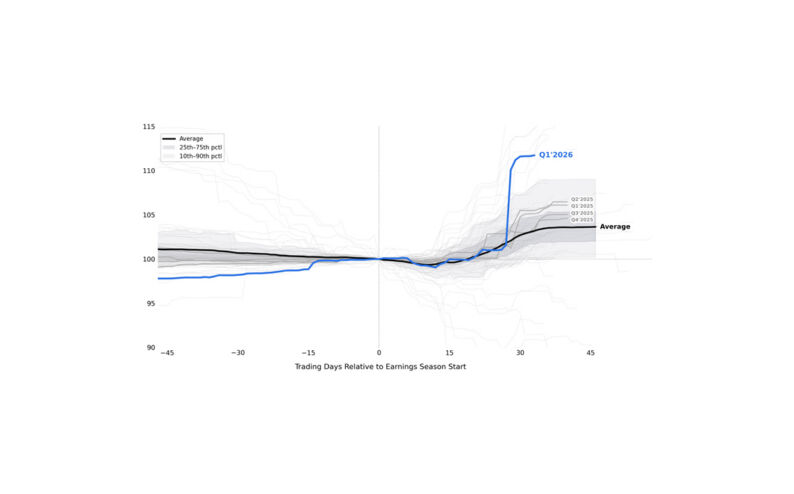

III. Q2 Earnings Outlook (Begins April 14)

We expect a transition back toward fundamentals following a period dominated by positioning and flow-driven price action.

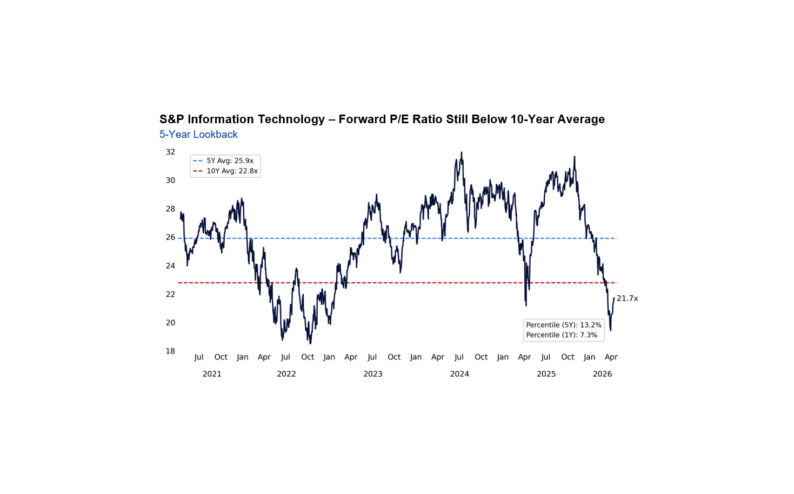

Valuation Reset

Valuations across U.S. equities have reset meaningfully, with both the S&P 500 and Nasdaq now trading at the lower end of their recent ranges. SPX forward P/E is now ~19.5x, below the 5-year average ~20.1x and in the sub-6th percentile of the past year’s range.

This marks a sharp reset from the start of the last earnings season (SPX forward P/E ~23x in October), providing a more supportive entry point for equities.

Earnings Revisions

Despite the reset in valuations, earnings revisions remain constructive – particularly for 2026 and 2027 – with strength concentrated in large-cap growth and technology.

Notably, EPS estimates have continued to trend higher over the past month, even amid broader market volatility and macro uncertainty, underscoring the resilience of the underlying earnings backdrop.

Positioning vs. Expectations

The market has shifted from a “low bar, high positioning” regime to a “high bar, low positioning” setup – characterized by high gross exposure (driven by shorts) and low net exposure.

At the same time, expectations remain solid, with double-digit earnings growth anticipated through the remainder of the year.

Key Catalyst: Technology Earnings

The “Super Bowl” of Q2 earnings takes place in the final week of April, with large-cap technology expected to drive a significant share of index-level outcomes.

43% of the S&P 500 by weight will report that week, including AAPL, MSFT, AMZN, META and BKNG.

GMI BOTTOM LINE

Positioning is light, sentiment is washed out, and flows are stabilizing after absorbing significant supply.

While the technical backdrop is not fully healed, the setup is asymmetric to the upside, particularly as volatility resets lower and markets start to transition back to fundamentals into Q2 earnings.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.