Markets are entering one of the most technically important periods of the year.

Over the next two weeks, price action is likely to be driven more by flows than fundamentals as investors navigate month-end, quarter-end, and first-half rebalancing activity. The market is set to absorb the largest options expiration in history, significant quarter-end pension rebalancing flows, and a broad reset in positioning across major investor cohorts.

Looking beyond quarter-end, however, the backdrop becomes increasingly supportive. Historically, July has been one of the strongest months of the year for US equities, as fresh capital is deployed, positioning is rebuilt, and several of the market’s largest sources of demand re-engage.

We remain focused on three key themes: record retail participation, a significant technical reset into quarter-end, and a favorable seasonal backdrop for risk assets. Together, these factors reinforce our view that the path of least resistance remains higher as markets transition into the second half of the year

I. Retail Investors Remain the Market’s Strongest Source of Demand

Retail activity remains one of the strongest sources of demand in today’s market. Through our unique position as the #1 US Retail Market Maker, executing ~35% of all US-listed retail volume, we continue to observe the highest and most persistent levels of retail participation on record. At the same time, the retail investor is evolving. Unlike previous periods of retail enthusiasm, today’s retail flows increasingly resemble those of institutional investors.

Retail Activity is Breaking Records

Retail trading activity has officially entered a new regime. The defining characteristic of today’s retail investor is not just enthusiasm, but persistence.

May shattered previous activity records in cash equities, surpassing the prior monthly high set in January 2021 by more than 10%. Retail cash equity volumes ran 60% above the 2025 average and more than twice the 2024 average. From this peak, activity has accelerated further in June, with volumes this month tracking 9% above May’s record.

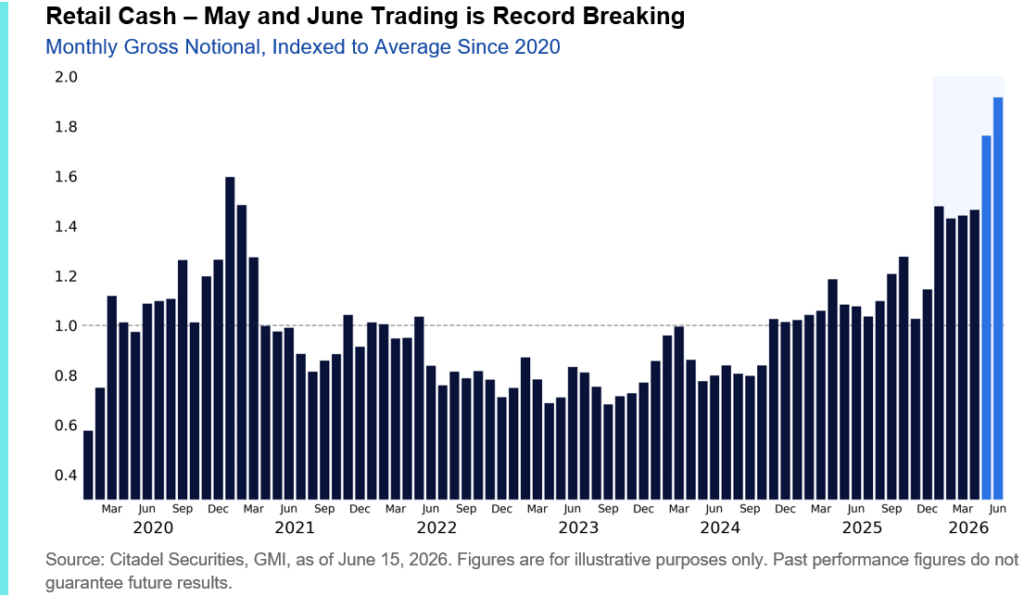

Nine of the ten largest retail trading days ever observed on our platform have occurred in just the last month, including seven during the first half of June alone. Friday (June 12) marked the largest single day of retail net buying in our dataset, surpassing the previous record by 50%.

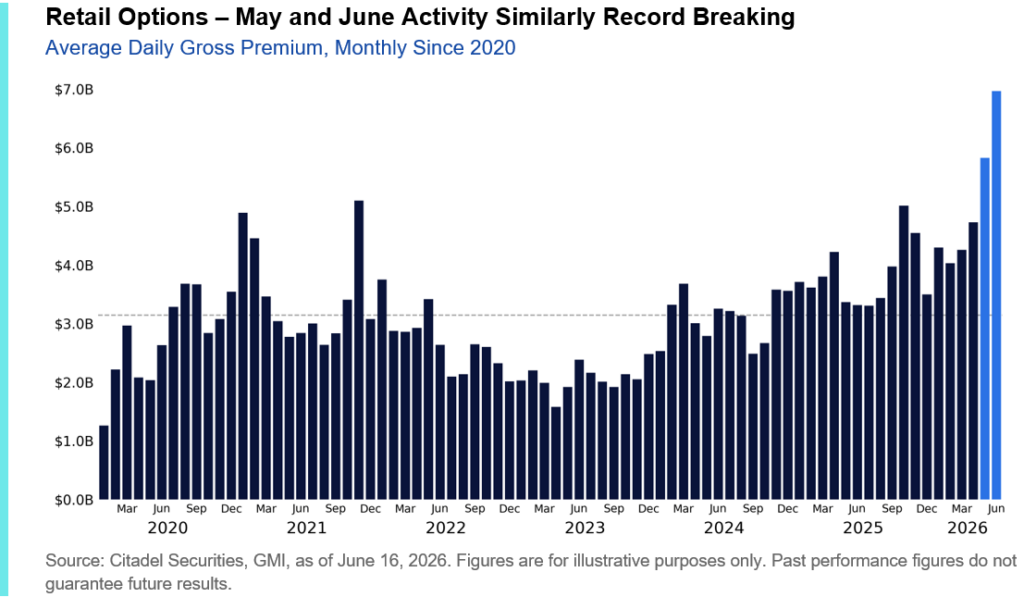

Options activity is similarly breaking records. Average daily options volume on the Citadel Securities retail platform reached a record high in May, running 20% above the trailing one-year average. Participation has continued to build in June, with volumes surpassing the highs made last month by another 20%.

New records are being set almost weekly. The first week of June established a new high for retail options activity, only to be surpassed the very next week. This week is on track to challenge those levels once again.

Retail investors are also deploying more capital, trading a record $5.8 billion of options premium per day during the month of May on our platform. This has already climbed to $7 billion in options premium per day in June.

The Retail Trader Has Evolved

As highlighted in our latest Retail Detail, The Return of Momentum, the composition of retail activity is as notable as its magnitude.

During the retail rally of 2021 and the volatility-driven surge in October 2025, retail flows were concentrated in idiosyncratic single-stock stories, often driven by high short interest equities.

Today’s retail investor looks markedly different. Rather than only chasing speculative corners of the market, retail investors are increasingly concentrated in the same companies driving benchmark returns and institutional positioning.

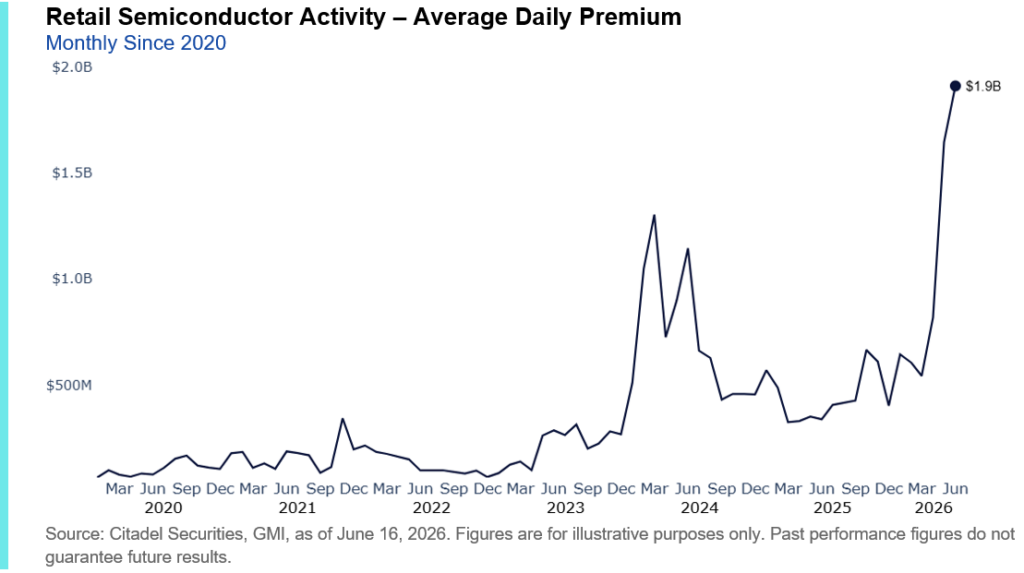

Semiconductors sit at the center of this trend. Average daily options premium traded in semiconductor names reached a record high of $1.6 billion in May, more than doubling April levels, running nearly 5x the historical average, and surpassing the previous record by more than 25%. June is already tracking at approximately $1.9 billion per day, 16% above May’s record.

Retail Investors Still Have Capacity

Record activity does not necessarily imply exhaustion.

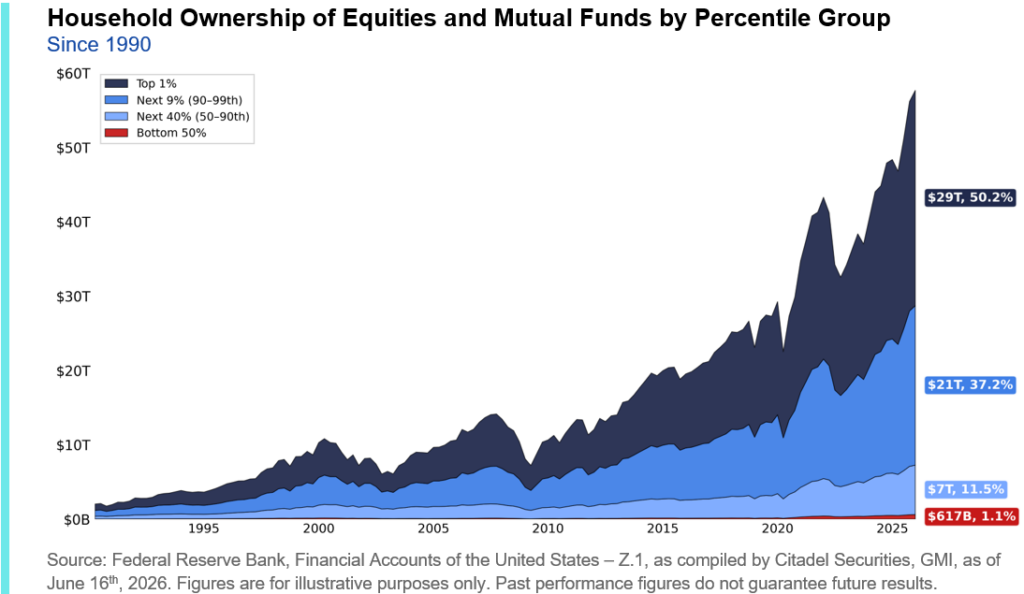

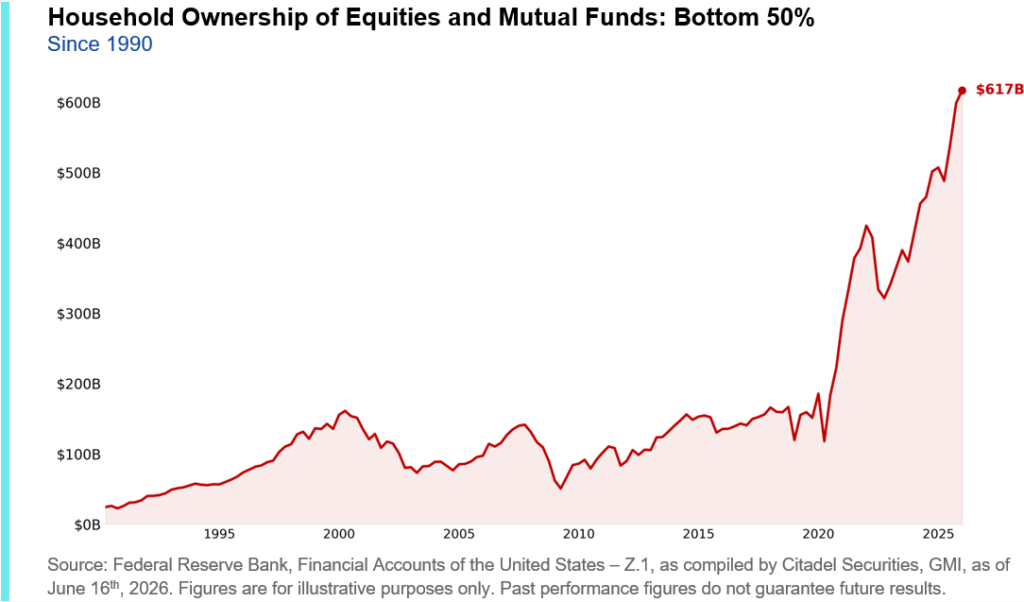

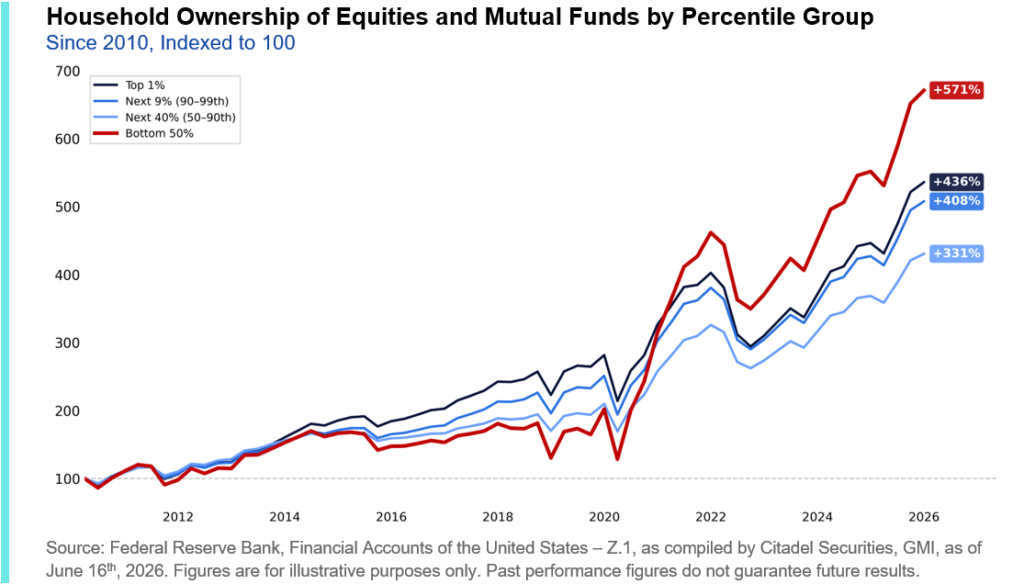

Equity ownership continues to broaden across income cohorts, with the fastest growth occurring among households that historically had the lowest market participation rates.

Since 2010, equity and mutual fund ownership among the bottom 50% of households has increased by more than 570%, outpacing every other wealth cohort. Today, the bottom half of households owns more than $600 billion of equities and mutual funds, a record high.

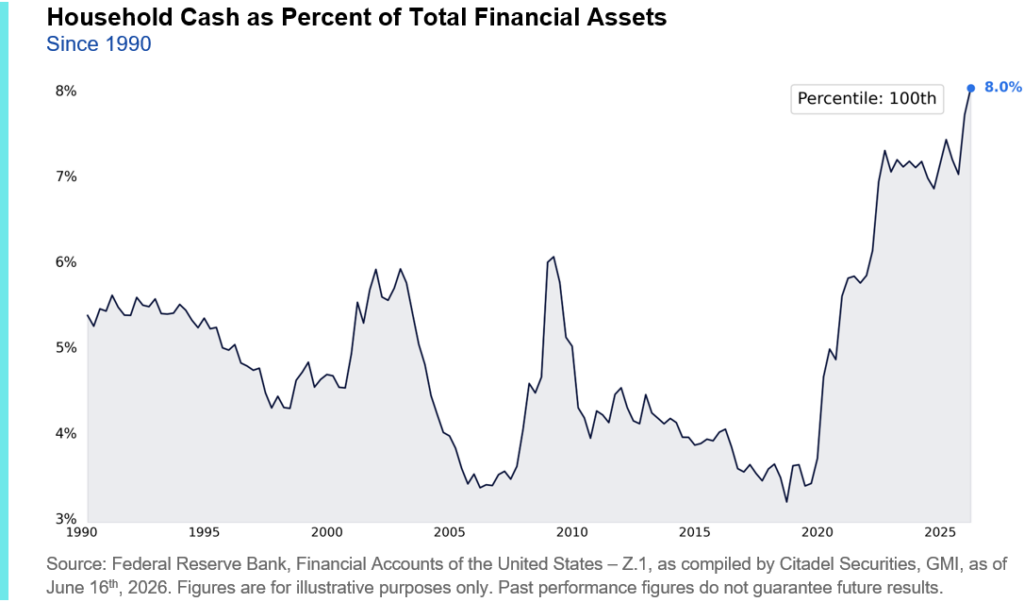

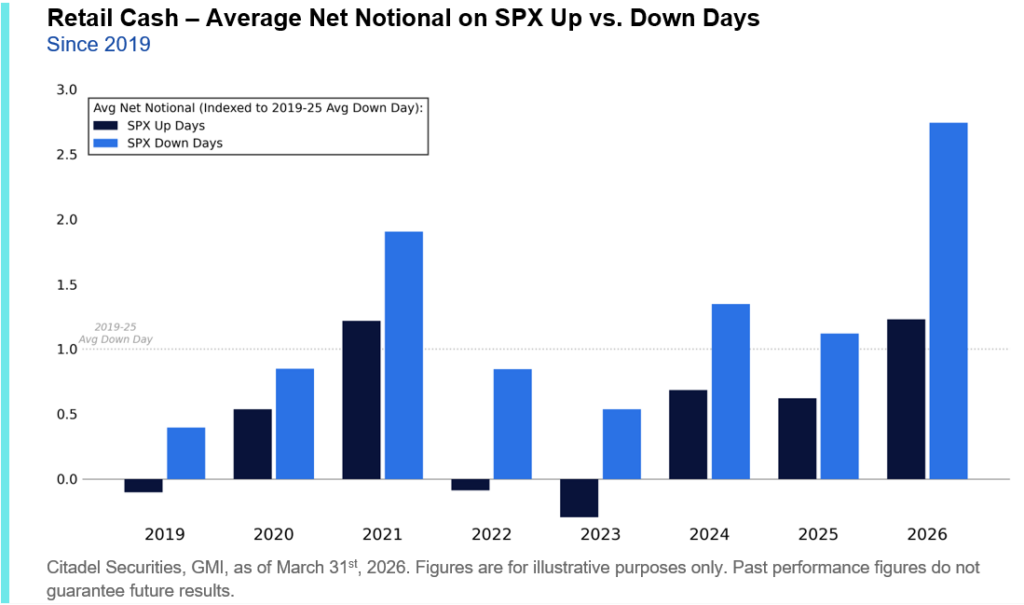

Despite increased engagement, households hold record cash balances, waiting to deploy capital on market dips. This dynamic only changes when the VIX rises above 30. Today, the VIX is approximately 16.

We observe this “buy-the-dip” behavior on most down trading days in our data at Citadel Securities.

II. Markets are Approaching a Major Technical Reset

The next two weeks are likely to be driven more by market mechanics than fundamentals.

Investors are navigating the largest options expiration in history, major index rebalances, quarter-end pension flows, and the start of a new allocation cycle. Taken together, these events represent one of the most significant periods of technical repositioning on the calendar.

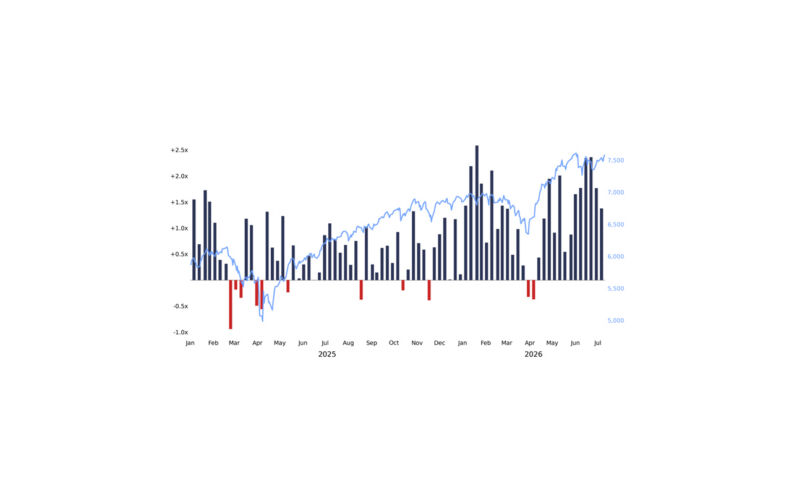

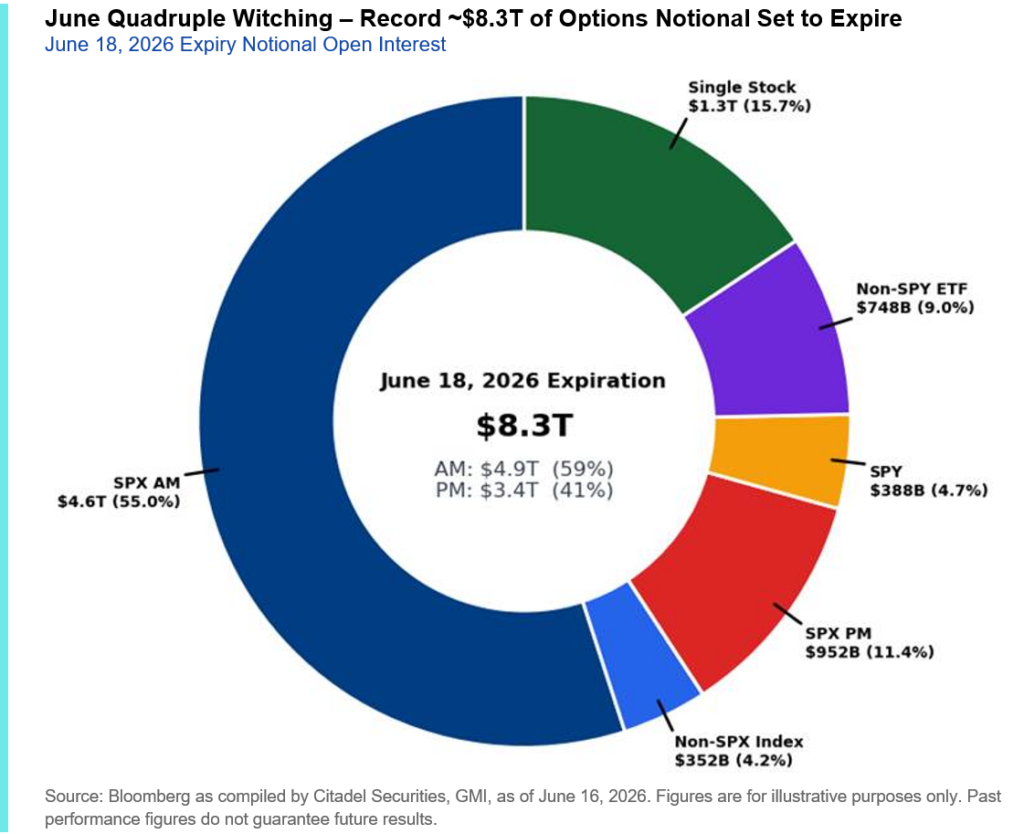

June OPEX – The Largest Options Expiry on Record

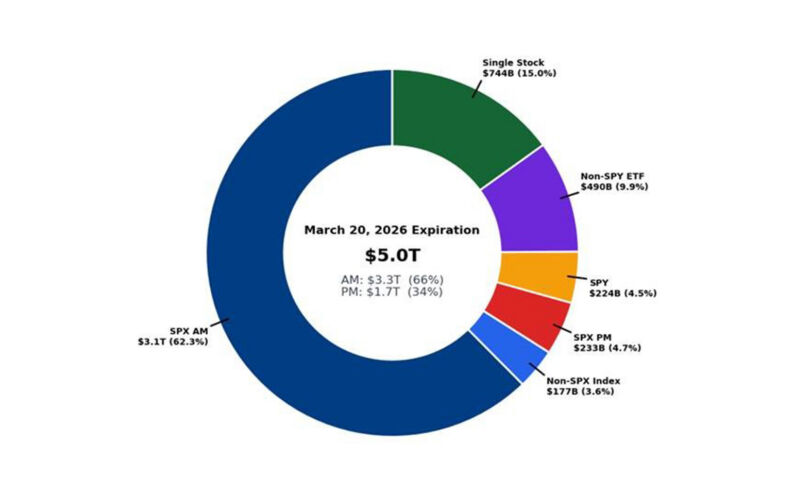

The first major technical event arrives with June quadruple witching tomorrow (June 18). Options open interest currently sits at all-time highs, and 28% of all listed options are set to expire in what will be the largest options expiration event in history.

An astounding ~$8.3 trillion of US options exposure will roll off, 18% larger than the previous record set in December (~$7.1 trillion). The event will clear a substantial amount of gamma from the market, resetting positioning and increasing sensitivity to flows as investors rebuild exposures into month-end.

Quarter-End Rebalancing

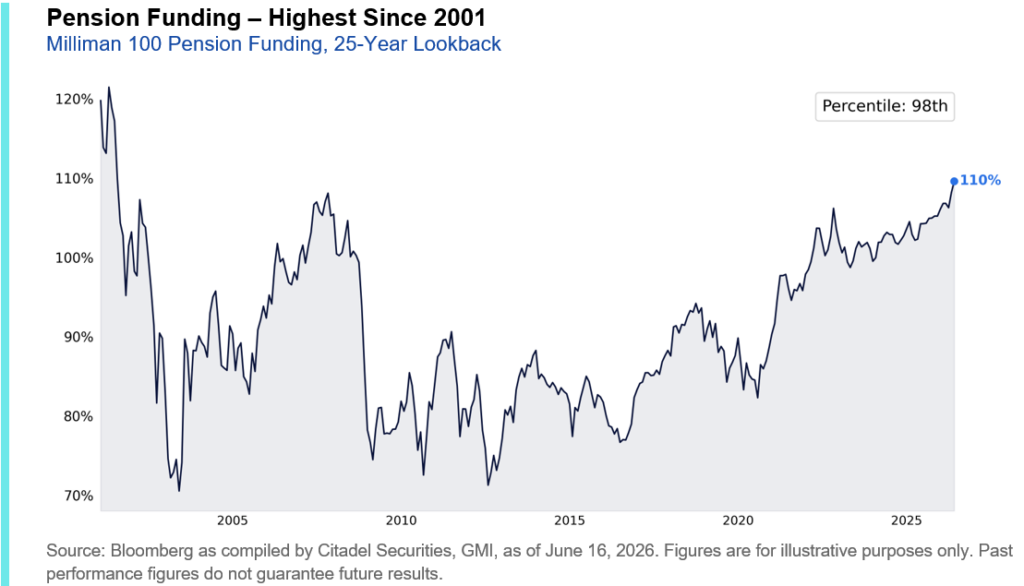

The second major technical event arrives at quarter-end. Many pension funds place significant emphasis on quarterly rebalancing. The top 100 US pension funds are currently 110% funded, their highest funding level since 2001.

As a result, we expect many plans to continue de-gliding and immunizing portfolios, creating a mechanical source of equity selling and fixed income buying into month-end. Any associated weakness should be viewed through a technical lens and, in our view, would likely prove temporary.

A New Allocation Cycle Begins

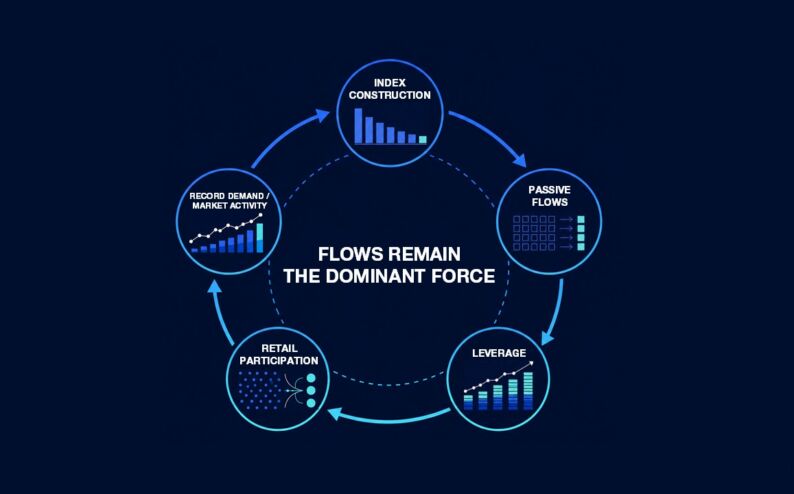

July 1st marks the beginning of a new allocation cycle as retirement contributions, target-date funds, passive allocations, mutual fund inflows, and systematic strategies begin deploying fresh capital. As one of the largest pools of assets in the world resets portfolios for a new quarter and a new half of the year, market leadership can increasingly be driven by the destination of those flows.

ETFs have accounted for approximately 31% of average daily trading volume year-to-date, well above the 10-year average of roughly 27%. As a larger share of market activity flows through passive vehicles, reallocation decisions can have an increasingly meaningful impact on price action.

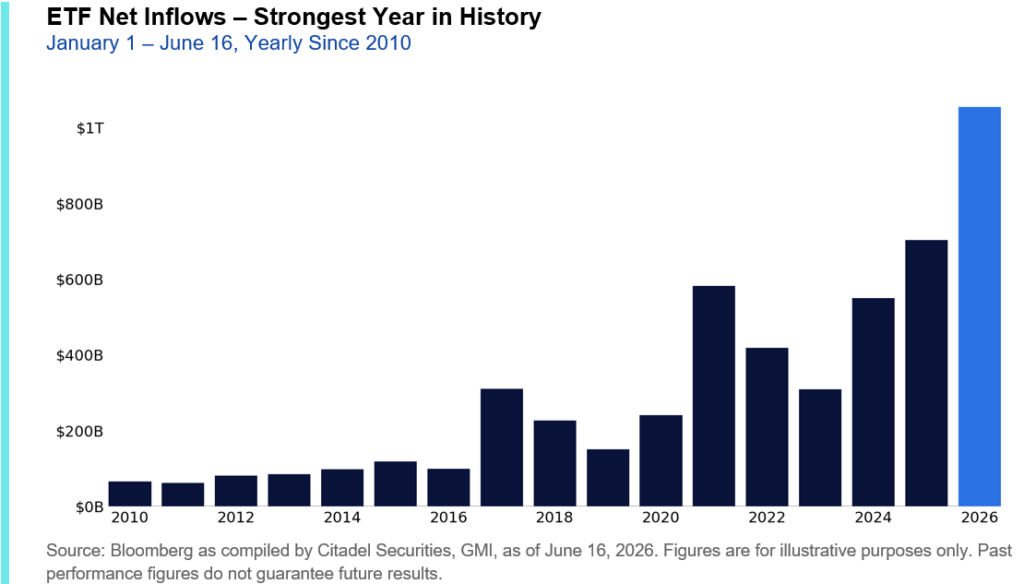

The scale of those flows remains extraordinary. ETFs have already attracted more than $1 trillion in inflows year-to-date, approximately 45% ahead of last year’s record pace. For perspective, the average full-year ETF inflow through 2024 was ~$490 billion. In less than six months, ETF investors have already allocated more than twice the amount that historically represented a full year’s worth of flows.

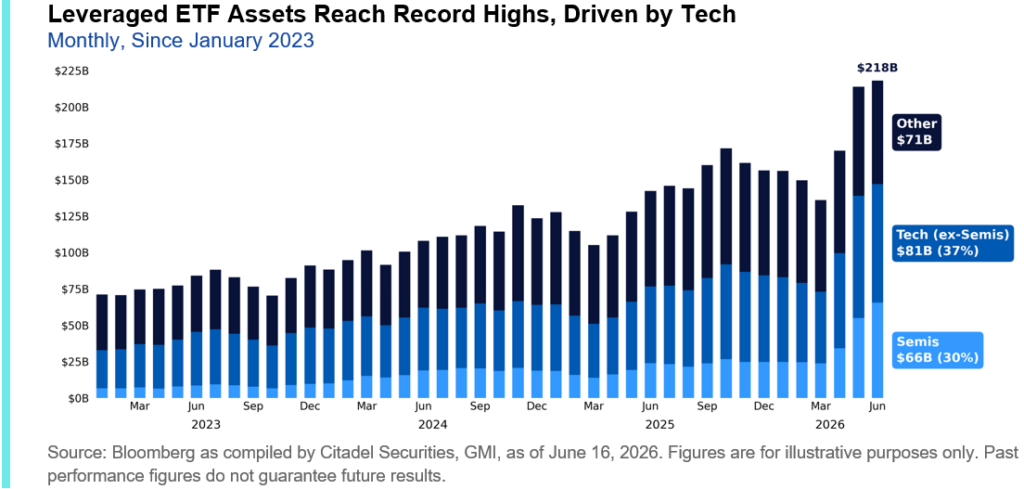

The growing influence of ETFs extends beyond traditional passive products. Leveraged ETFs have become one of the fastest-growing segments of the market, introducing an additional layer of mechanically driven buying and selling activity. Assets under management in these ETFs have reached a record ~$218 billion, increasing by roughly $82 billion (+60%) since the end of March alone. Leverage tied to technology has grown 136% over the same period, while leverage linked to semiconductor exposure has nearly tripled (+175%).

This dynamic is particularly important in today’s market, where an increasing share of capital is directed by index construction itself.

Index Construction Matters More Than Ever

As a reminder, today roughly 18 cents of every dollar allocated to the S&P 500 is directed toward semiconductor companies, 33 cents flows into the Mag 7, and nearly 40 cents is concentrated in the index’s ten largest holdings.

As passive ownership grows and ETF flows continue to accelerate, an increasingly disproportionate share of new capital is directed toward the same companies already driving benchmark returns.

III. The Calendar Turns Supportive

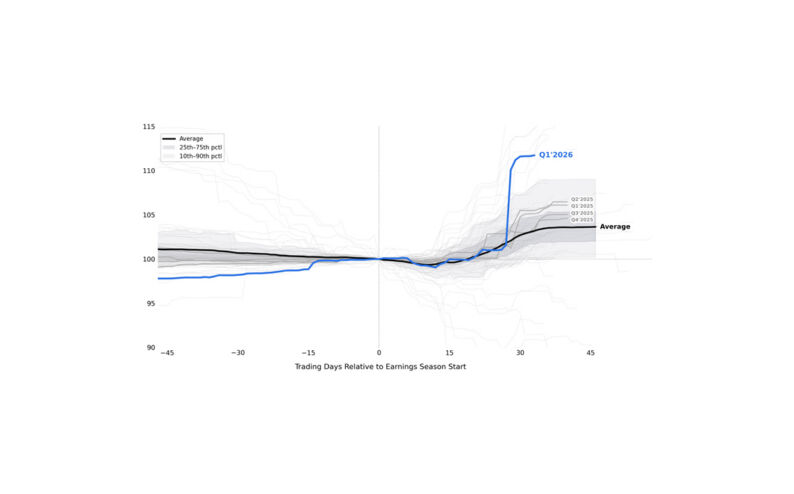

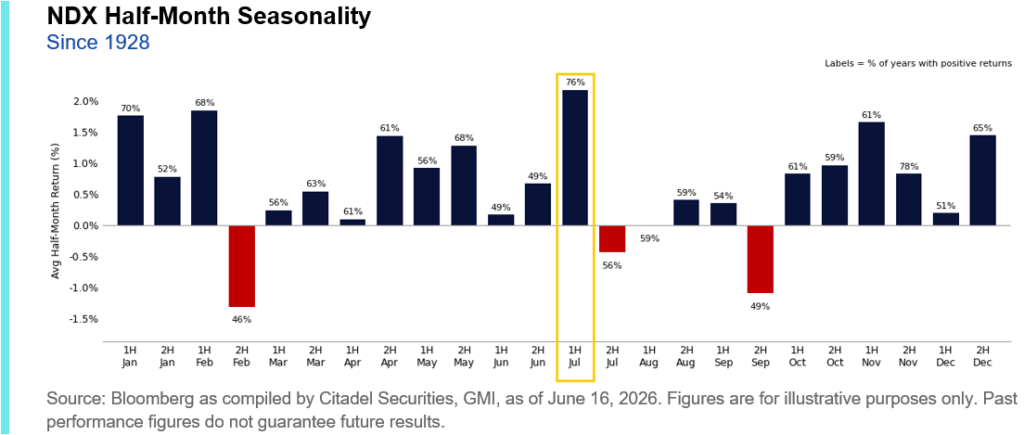

The mid-year flow cycle has historically aligned with strong July performance across major equity indices, particularly during the first half of the month.

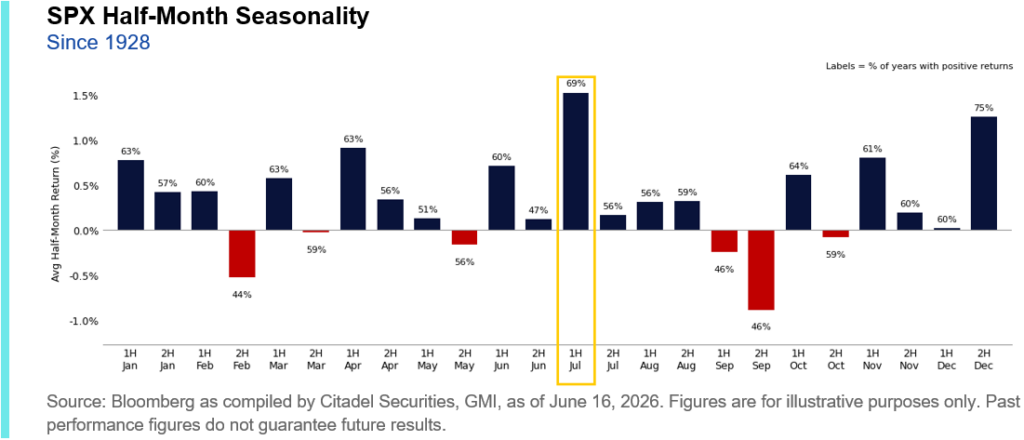

Historically, the first half of July firmly stands out as one of the strongest seasonal periods of the year:

- Since 1928, the S&P 500 has advanced 69% of the time during the first half of July, generating an average return of 1.5% and an average rally of 3.2% when positive.

- Since 1985, the Nasdaq 100 has risen 76% of the time, with an average return of 2.2% and an average rally of 4.4%.

The S&P 500 has finished higher in each of the last 11 Julys, while the Nasdaq 100 has advanced in 17 of the last 18 years.

This seasonal backdrop is reinforced by several of the market’s largest sources of demand.

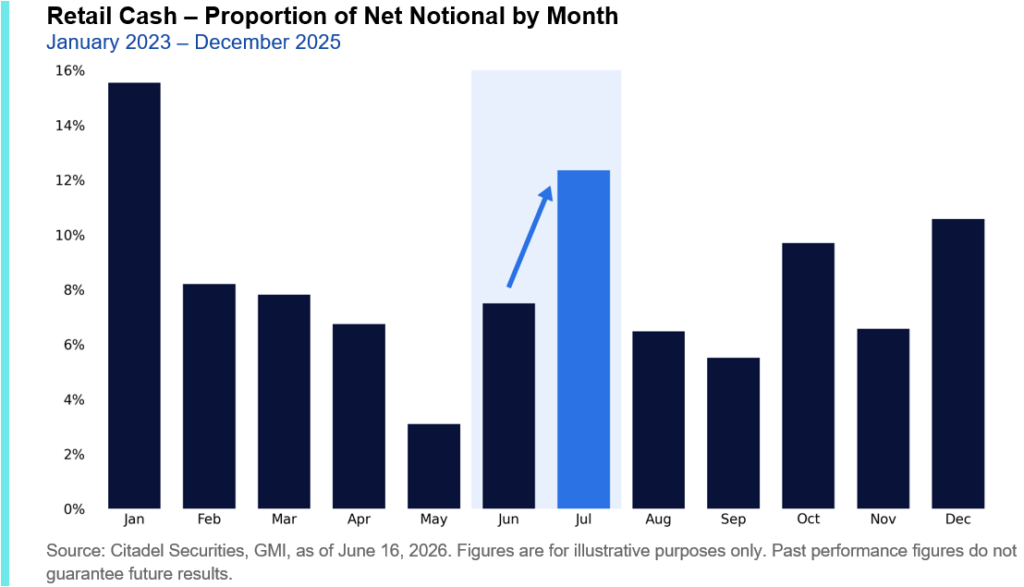

Retail participation has historically remained elevated during July, a trend that may prove particularly important this year given the record levels of activity currently observed across our platform. Based on net capital deployment, July ranks as the second-most active month of the year for retail investors, trailing only January, the market’s most important annual allocation window.

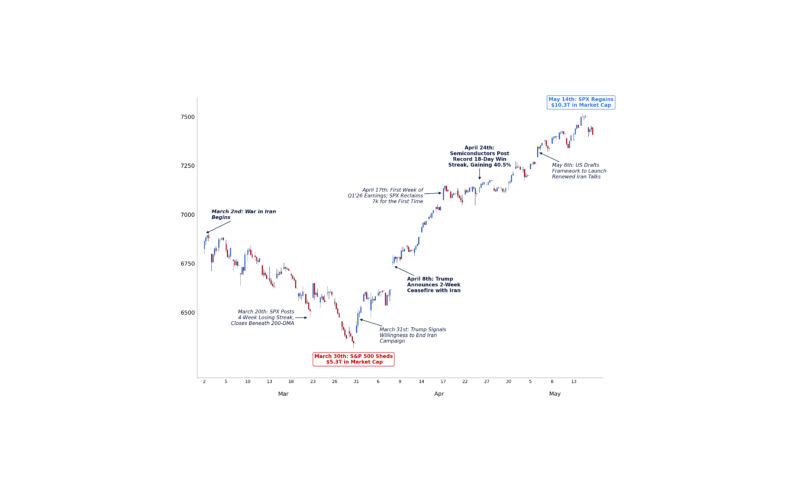

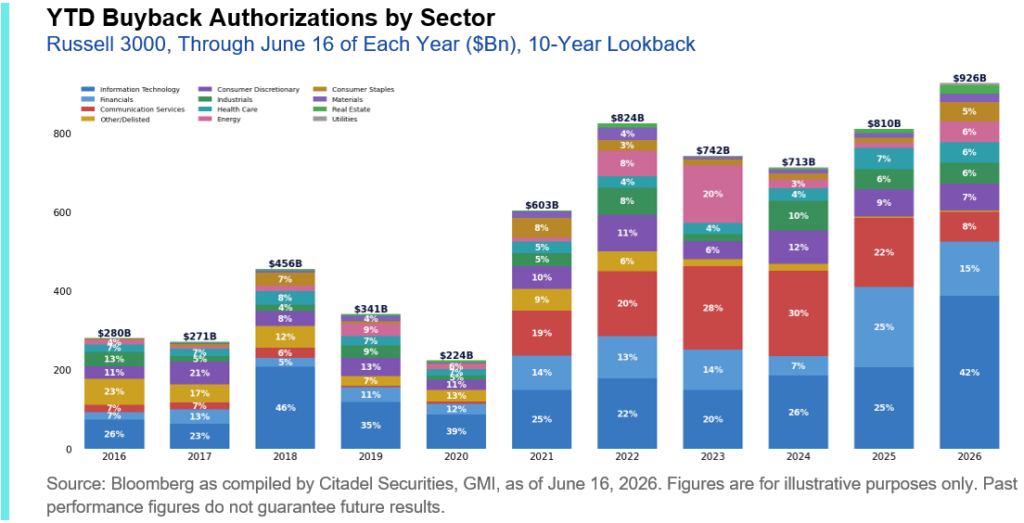

Meanwhile, the largest buyer of U.S. equities remains active. Year-to-date, US corporates have authorized more than $925 billion of share repurchases, the strongest pace ever recorded through this point in the year. Technology and Financials account for roughly 57% of all announced buybacks in 2026, reinforcing demand in many of the same sectors already benefiting from strong retail participation and passive flows. Equity issuance remains small even when compared to current buyback demand.

GMI BOTTOM LINE

We expect the next two weeks to be dominated by flows, not fundamentals.

The market is about to absorb the largest options expiration in history, quarter-end pension rebalancing, and a significant reset in positioning across major investor cohorts. Any resulting weakness should be viewed through a technical lens.

Looking beyond quarter-end, the setup remains favorable. Retail demand is at record highs, ETF inflows continue to accelerate, corporate buybacks remain robust, and the market is entering one of its strongest seasonal periods of the year.

We continue to believe the path of least resistance is higher as markets transition into the second half of the year.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.