Over the last seven weeks, I have spent time meeting with institutional investors across the US, Europe, and Asia, and the conversations have become remarkably consistent.

The debate is no longer whether the rally is fundamentally justified. Earnings have been significantly stronger than expected, AI capex trends remain robust, and systematic flows continue reinforcing momentum beneath the surface. Instead, investors are increasingly focused on how much of the move is now being driven by flows, positioning, and market structure, and whether broader participation can emerge without disrupting the current leadership regime.

A few themes and debates continue to dominate institutional client conversations globally right now – below we highlight the ones we are hearing most frequently.

Global Roadshow Insights: The Top Themes Driving Institutional Client Conversations

1. Can earnings catch up to prices after such a strong move higher in equities?

Clients continue to ask whether EPS revisions are finally beginning to improve, whether markets are discounting 2027 growth too aggressively, and which sectors genuinely possess operating leverage versus those benefiting primarily from narrative-driven optimism.

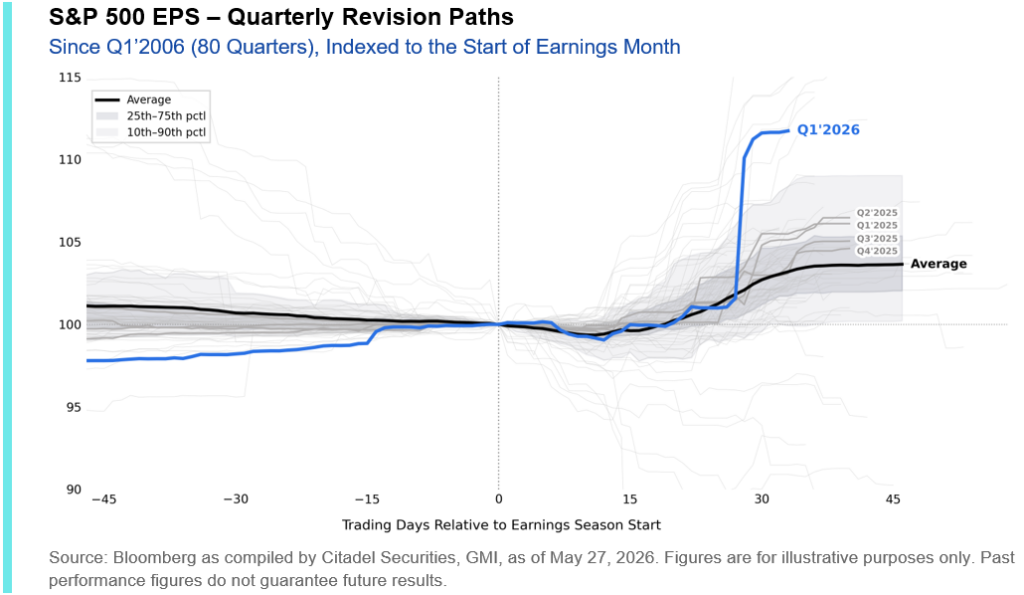

So far, the earnings backdrop has more than supported the move higher in equities.

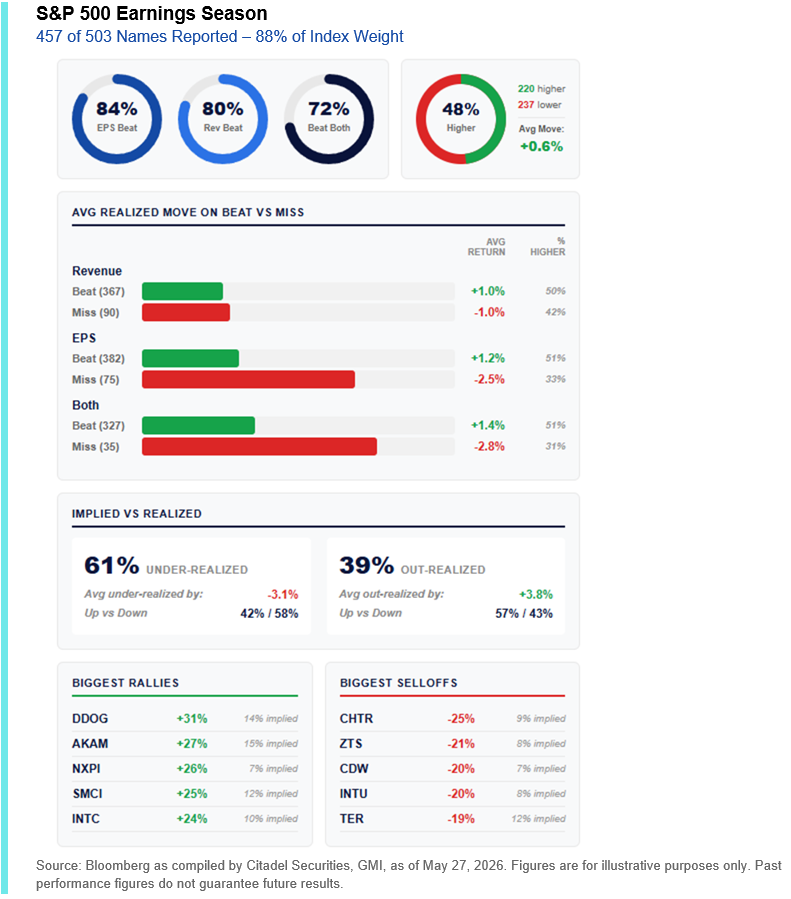

The S&P 500 just posted its strongest earnings season since the post-COVID era. Q1 earnings growth nearly doubled expectations, rising from ~13% expected at the start of reporting season to roughly ~25.5% YoY today.

The largest debates continue to center around AI monetization, corporate margins, productivity gains, and the sustainability of current hyperscaler capex trends. However, AI is increasingly becoming an earnings and revenue story rather than simply a narrative.

The slope of upward revisions this quarter ran materially above a normal seasonal path, particularly across technology (where Q1 EPS growth is +50% YoY).

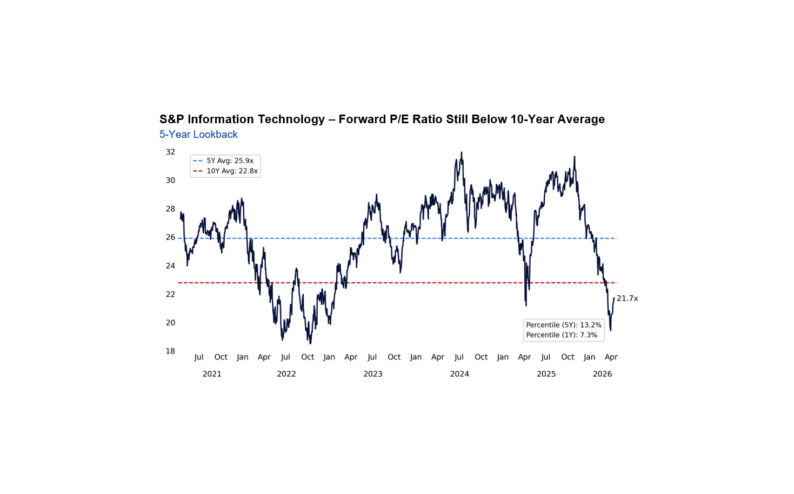

2. Why have stocks effectively become cheaper from a valuation perspective even as markets move higher?

This is not 1999.

At first glance it sounds unlikely, but the math tells an important story. The S&P 500 is up roughly ~10% year-to-date, yet the forward P/E ratio has fallen from ~22.3x at the start of the year to roughly ~21x today (still in the bottom quintile of its 1-year range).

Forward EPS estimates have increased from roughly ~$235 at the start of the year to ~$350 today, driven primarily by large upward revisions across mega-cap technology. In other words, this rally has not been driven purely by multiple expansion, which is typically what investors associate with speculative bubbles.

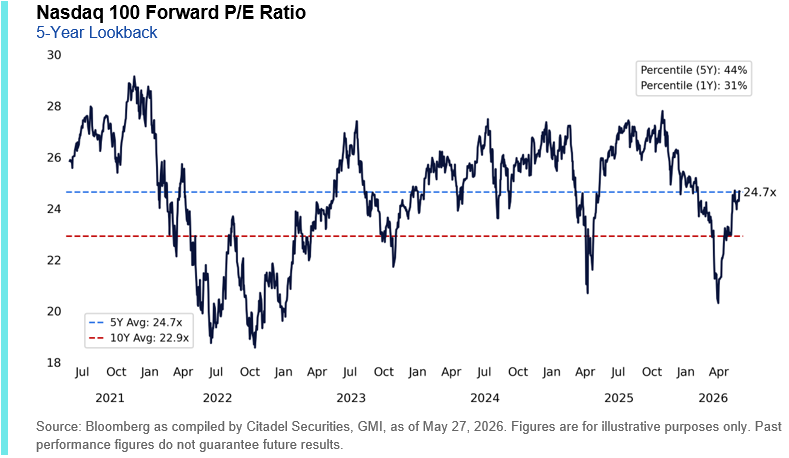

The Nasdaq also remains below its 5-year average valuation multiple despite a +30% rebound since late March. Today, the NDX trades at roughly ~24.7x forward earnings, well below the November 2021 peak and only around the ~31st percentile of its 1-year range.

3. Are discretionary equity risk-takers still underinvested?

Yes, although the conversation has evolved significantly over the past two months.

Many portfolio managers reduced exposure earlier this year amid macroeconomic and policy uncertainty, but are now finding themselves chasing performance as equities continue to move higher.

The conversation has increasingly shifted away from downside protection and toward how much cash remains on the sidelines, where the next incremental buyer comes from, and whether systematic flows can continue extending the rally.

This dynamic becomes increasingly important into month- and quarter-end, as well as the start of 2H, particularly as benchmark pressure intensifies when first-half performance statements are sent out.

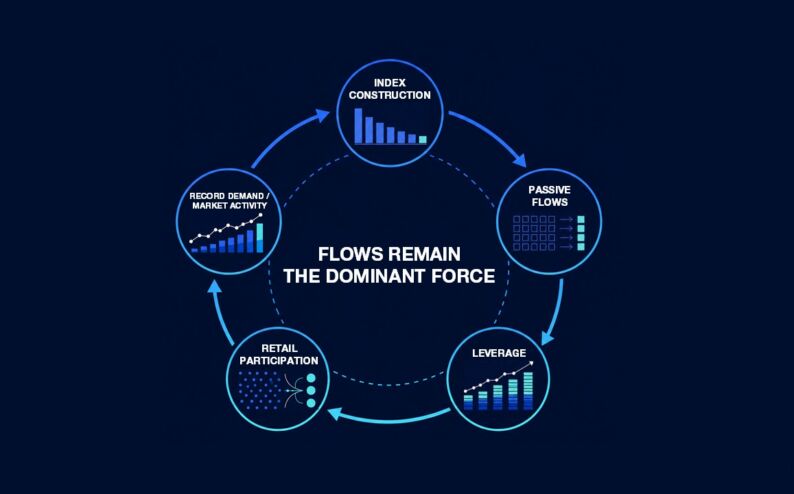

4. How much of this rally is being driven by flows versus fundamentals?

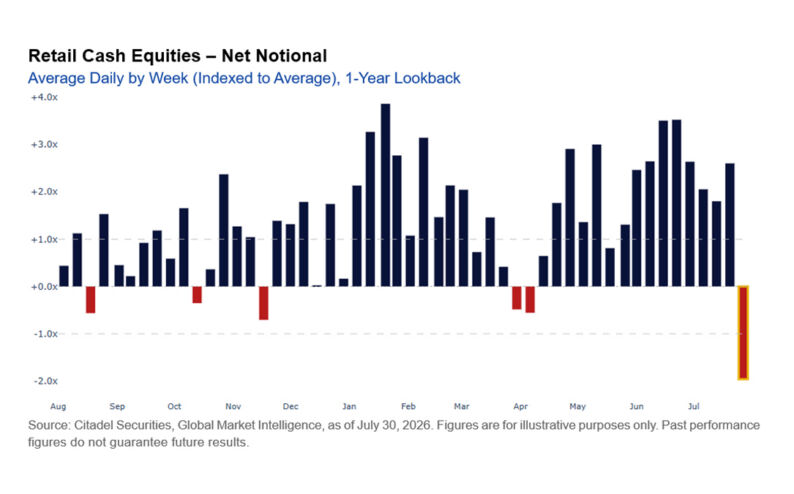

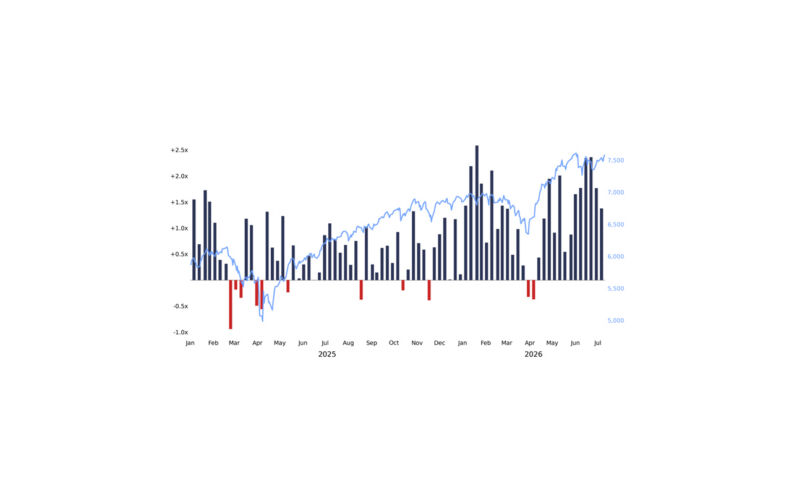

Institutional investors remain heavily focused on flow-of-funds dynamics and the persistent supply/demand imbalance supporting equities. Key tactical flows being watched include CTA positioning (very long), volatility-control demand (increasing), corporate buybacks (accelerating), retail participation (record), pension rebalancing activity (re-risking), and long dealer gamma (market buffer) dynamics.

The debate has shifted toward how mechanically driven current price action has become and how much systematic buying power still remains available to support equities from here. I am concerned about potential mechanical de-leveraging risk, although likely not for today. Last week’s mini de-leveraging event was small and fast, but reinforced how sensitive markets have become to positioning-driven flow adjustments beneath the surface.

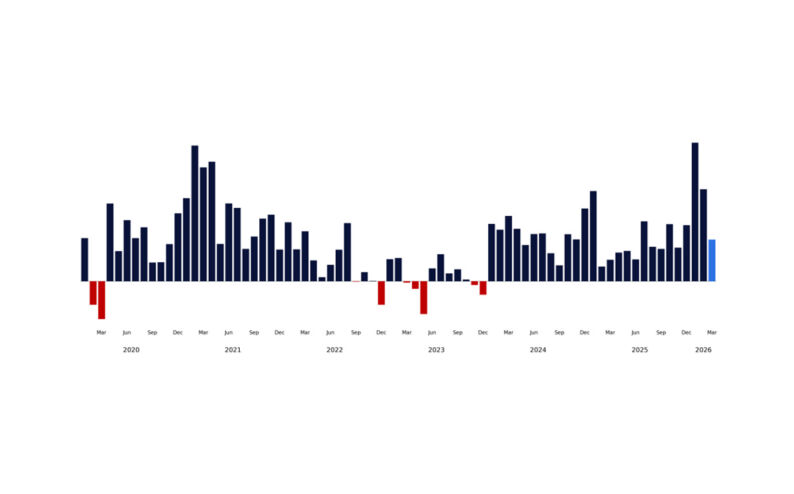

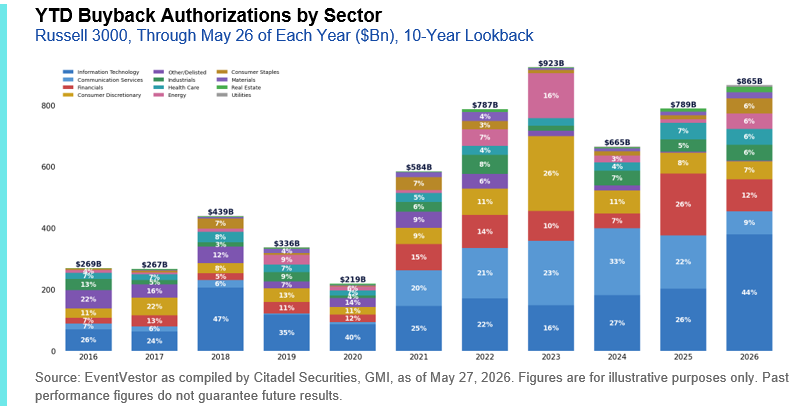

US Corporates have authorized $865 billion worth of stock buybacks in 2026 YTD. The largest buyer of US stocks on an annualized basis will repurchase another $1.5 trillion worth of stock this year, showing confidence from corporate CEOs.

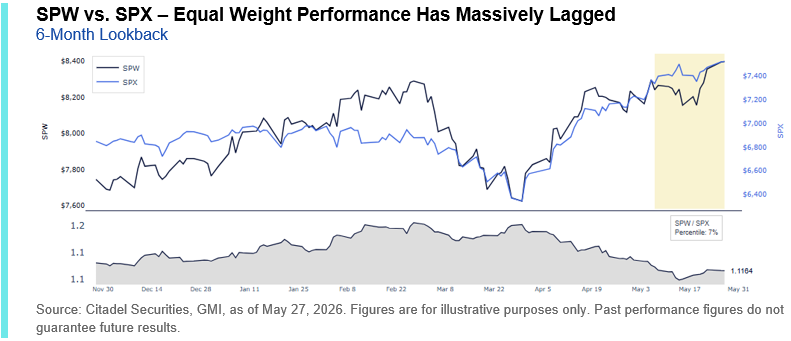

5. Is this still a narrow rally, or is participation finally broadening out? Will investors broaden heading into the mid-term elections?

Clients want to know whether leadership remains concentrated in mega-cap AI and technology names, or whether the 493, cyclicals, small caps, financials, industrials, and international equities are beginning to participate in a more meaningful way.

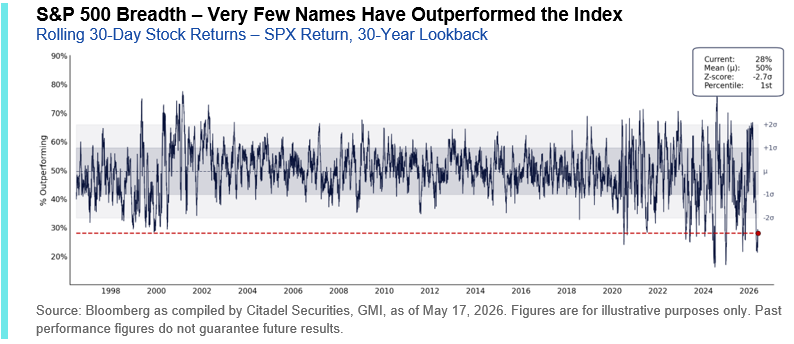

Breadth matters because narrow rallies often feel fragile, particularly when flows remain concentrated in the same handful of risk assets including semiconductors, memory, space, optics, and power.

Breadth remains historically narrow beneath the surface of the rally – just 28% of S&P 500 constituents have outperformed the index over the past 30 trading days, a 1st percentile observation relative to the past 30 years.

Said differently, 67% of the S&P 500’s rally since the end of March has come from just 10 companies.

6. Should investors rotate into lagging sectors or remain concentrated in the current market leaders?

This has become one of the most difficult portfolio decisions in the current market.

Clients increasingly want exposure to the lagging parts of the index including cyclicals, small caps, financials, industrials, and rate-sensitive sectors, particularly if geopolitical tensions continue to stabilize and the rates backdrop improves.

The challenge is that many investors remain heavily positioned in the current leadership cohort, particularly semiconductors and mega-cap technology. A meaningful rotation into lagging sectors would likely require funding from existing technology and semiconductor longs.

We started to see early signs of this healthier broadening dynamic yesterday. While headline index performance appeared weaker, market internals were actually some of the healthiest we have seen in quite some time, with sectors that have lagged since the end of March starting to outperform (i.e., consumer discretionary, homebuilders, biotech).

Clients are debating whether this marks the beginning of a meaningful catch-up trade, whether lower-quality stocks tend to outperform later in the cycle, and whether defensive sectors remain permanently impaired if rates stabilize.

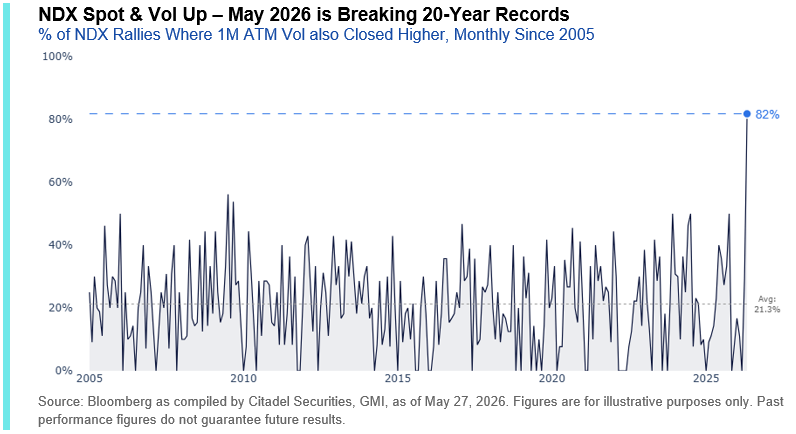

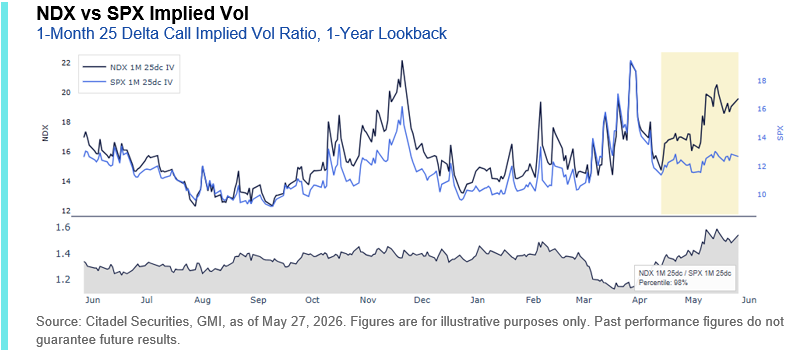

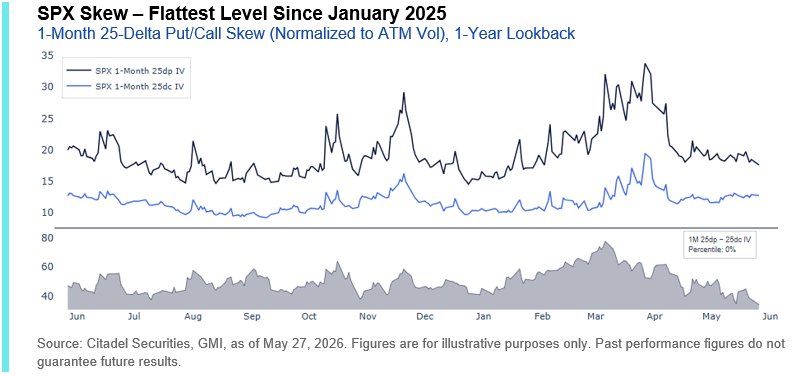

7. What does this environment mean for volatility? And why have we seen rare “spot up + vol up” behavior?

As realized volatility compresses, clients increasingly ask whether lower volatility itself is mechanically extending the rally. Investors also remain focused on whether markets are underpricing tail risk, whether skew has become too inexpensive, and at what point volatility suppression could become unstable.

What has made this rally particularly unusual is the emergence of a persistent “spot up, vol up” dynamic, particularly across Nasdaq and Semiconductor leadership. The chase for tech upside through call options has pushed call volatility higher even as equities continue to rally. This has been most visible in the Nasdaq, where elevated demand for upside exposure has driven NDX volatility to its richest levels versus SPX in more than a year.

Through May 2026 to date, NDX has experienced 9 sessions in which both spot and 1-month at-the-money implied volatility moved higher, accounting for ~82% of all rallies this month. This is the highest frequency observed in data going back to 2005 and well above the long-run monthly average closer to ~21%.

This has forced put/call skew to materially flatten, with one-month downside protection now trading near its cheapest levels relative to upside exposure in more than a year.

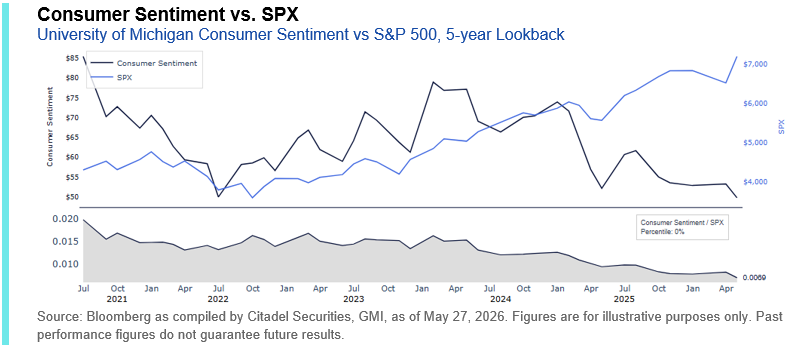

8. Why is the stock market not the economy? What is the retail investor doing now?

The economy measures jobs, wages, spending, and overall activity, while the stock market reflects expectations for future corporate profits. Markets are forward-looking and stocks price in what investors think will happen six to eighteen months from now, not what is happening today. That is why stocks can rise even when consumer sentiment regarding the broader economy feels weak.

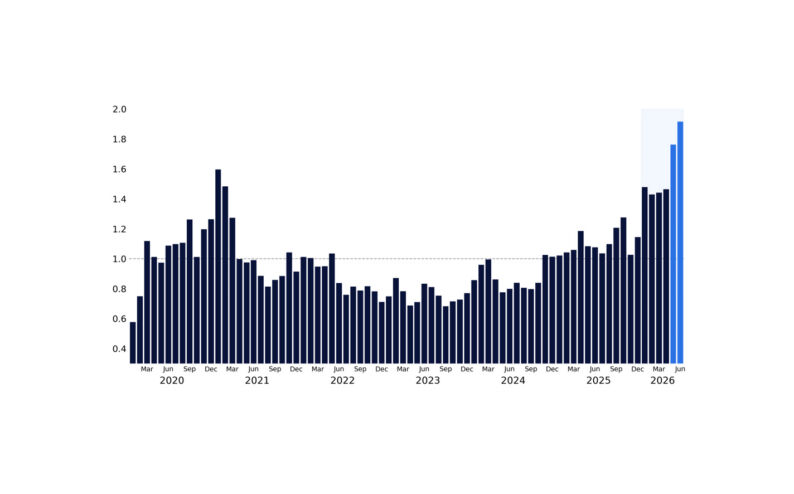

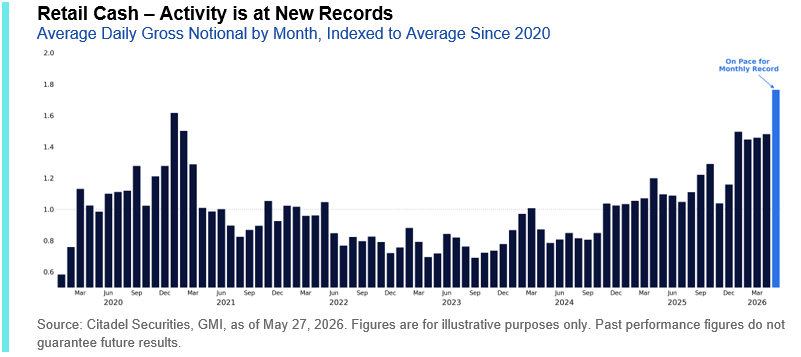

Retail traders are the new price setters in the market. May volumes across our retail cash equities and options platforms are currently tracking at record levels. Daily volumes on our cash platform are setting new highs and are on pace to finish nearly ~10% above the previous record established during the January 2021 meme-stock era.

Retail options activity has been similarly elevated, with May currently tracking as the second-highest monthly ADV we have ever seen, second only to the October 2025 squeeze. More notably, May is on pace to become the largest month on record in terms of options premium traded. Average daily gross options premium is currently tracking roughly ~1.9x the historical monthly average and ~13% above the prior peak from 2021.

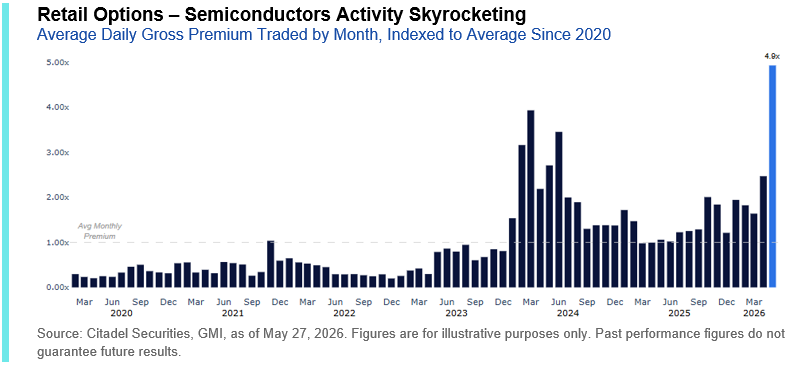

The biggest difference between January 2021 and today is where that activity is concentrated. Retail participation is increasingly focused in the same high-quality leadership names as institutional investors, particularly across semiconductors, AI infrastructure, and mega-cap technology.

Retail traders have also been a notable contributor to the current “spot up, vol up” dynamic. Total retail options volume in our semiconductor basket this month is currently ~2.7x larger than average, the highest reading on record, and roughly ~15% above the previous peak from June 2024.

Even more notable, gross options premium traded across semiconductors this month is running ~5x above the historical monthly average and roughly ~25% above the prior record from March 2024.

9. What is the pain trade now?

“Higher, then lower.”

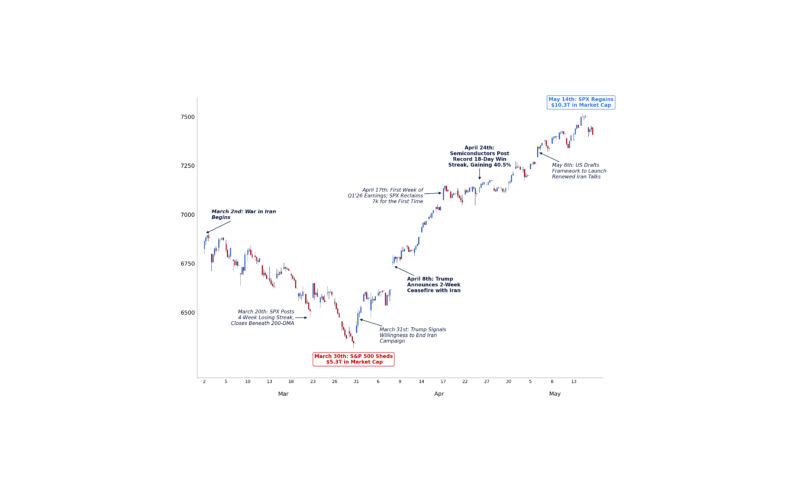

Earlier this year, the pain trade was lower equity prices into the March drawdown. Today, after an extended rally, the pain trade has shifted toward the possibility of even higher equities on improving geopolitical sentiment, lower volatility, continued mega-cap leadership, and bearish bond investors ultimately capitulating.

These shifts in positioning psychology can extend rallies significantly longer than fundamentals alone would otherwise justify. The pain trade remains higher as the “wall of worry” in global macro has slowed re-risking into high-profile IPOs and fast-track index inclusion.

10. What ultimately pauses the rally?

Investors are not necessarily bearish, but many remain long crowded equities while simultaneously nervous about the durability and pace of the move since March 30th.

The most common concerns include a reacceleration in inflation, higher rates, Treasury supply and liquidity pressures, policy uncertainty, questions surrounding AI capex payback, crowded positioning, and prolonged geopolitical risk.

Increasingly, the debate centers around what potential catalyst could be powerful enough to overwhelm the current flow-driven environment.

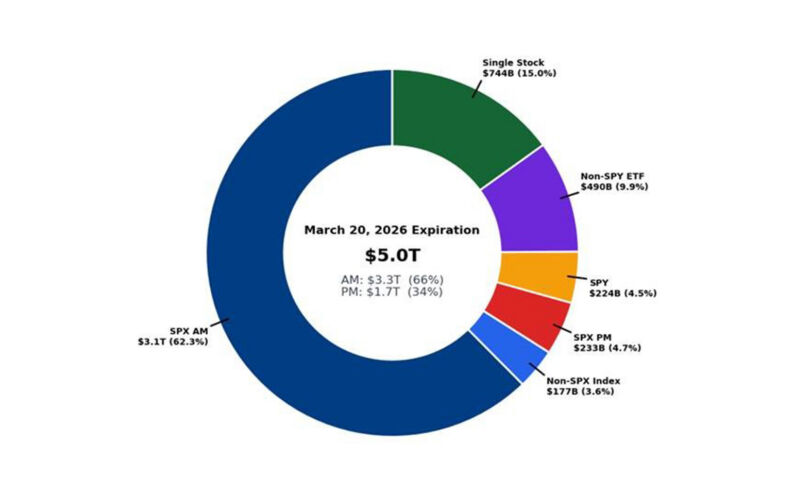

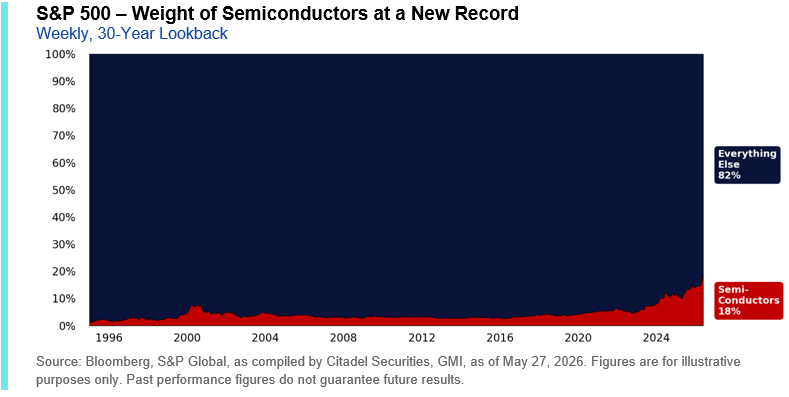

The heavy indexing of modern flows means market dynamics are increasingly dictated by concentration. If you allocate $1 into the S&P 500 ETF today:

- ~18 cents is allocated to semiconductors (record)

- ~37 cents goes into the Magnificent 7 (near-record)

- ~41 cents is concentrated in the Top 10 holdings (record)

Ultimately, the pause in the rally comes from weakness in technology, particularly given how dominant the largest market-capitalization tech companies have become across ETFs, options positioning, and levered products. Importantly, even a healthy broadening into cyclicals, small caps, or lagging sectors could temporarily pressure headline indices if investors fund those rotations by reducing exposure to the current leadership cohort.

GMI BOTTOM LINE

The current equity rally remains characterized by a powerful but increasingly unusual combination: historically narrow breadth alongside exceptionally strong earnings growth. Rather than a speculative bubble driven purely by multiple expansion, mega-cap technology earnings and revisions have continued to outpace price appreciation, allowing valuations to compress even as equities move higher.

At the same time, intense performance-chasing, systematic positioning, and flow-driven momentum have created a market where many investors still feel underinvested (despite equities sitting at highs) and in a state of nervous bullishness, actively searching for the catalyst capable of disrupting the current momentum regime. This has fueled increasingly rare dynamics such as the “spot up, vol up” behavior seen throughout May.

Ultimately, the pain trade likely remains higher for now. But the market is also becoming progressively more dependent on the same leadership cohort, the same systematic flows, and the same momentum dynamics continuing to work simultaneously beneath the surface.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.