Hysteresis describes a concept in which the present state of a system depends not only on current conditions, but on the path the system has taken to get there. In a simple linear system, removing the original shock restores the prior equilibrium. In a hysteretic system, the shock changes the structure of the system itself; with a conceptual implication that temporary shocks can have durable effects: once the system has been pushed into a new state, reversing the initial impulse does not reverse the consequences it set in motion.

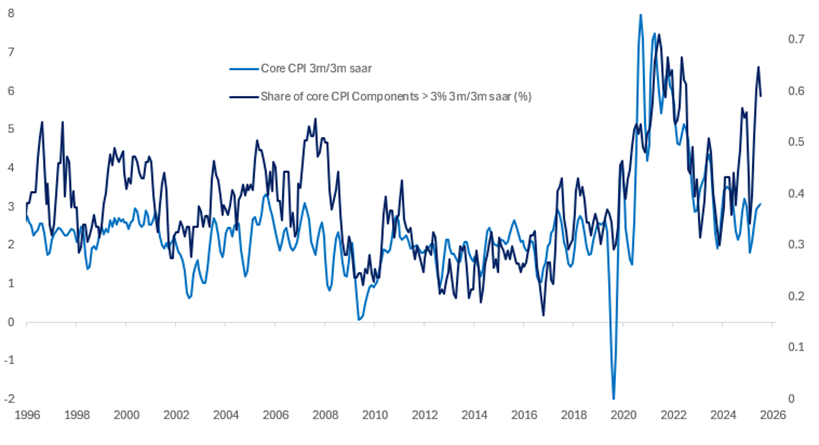

Inflation Breadth is Accelerating

Share of Components >3% 3m annualized vs Core CPI

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

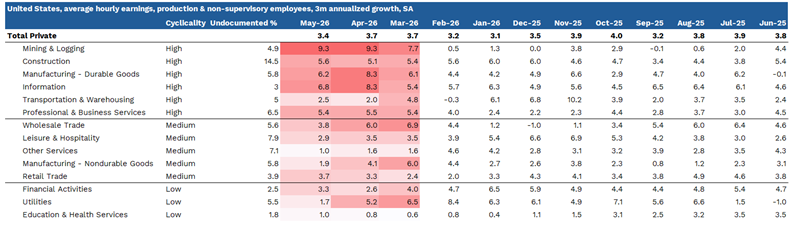

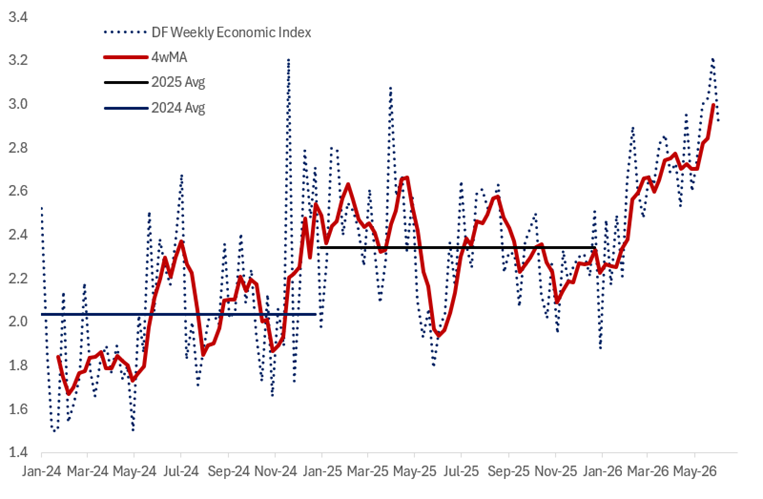

We see a growing risk that the US inflation process is shifting toward a hysteretic equilibrium, in which more sustained price pressures may persist even after the initial energy shock fades. We think the near-term boost to headline inflation from higher energy prices, together with renewed supply-chain disruption, is likely to catalyze second-round effects at a particularly vulnerable point in the cycle, as a temporary price shock collides with our expectation of a positive output gap, easy financial conditions, a generational AI capex cycle ($0.75tn in 2026, $1.25tn in 2027), and a reaccelerating labor market. In that context, an unwind in oil prices may not be sufficient to offset the broader chain of events driving the inflation process. We already see evidence of inflation expectations spilling over into the most cyclical parts of the labor market, where wages are accelerating meaningfully faster than the aggregate (see table below). We think this is an important leading indicator of broader wage growth, given it captures the interaction of the energy shock with our above consensus estimate of the output gap, driven by the continued support to economic activity from the capex cycle. We also note that inflation breadth is accelerating alongside high-frequency economic activity tracking close to 3% (Dallas Fed tracking below).

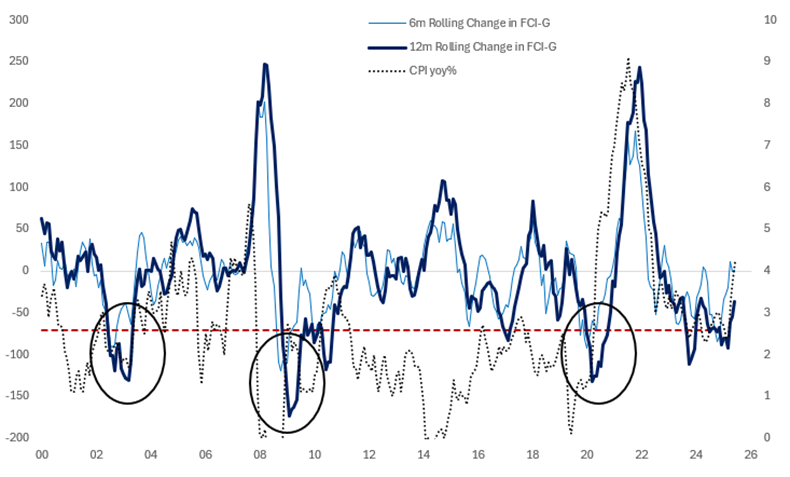

Financial Conditions are Easy Both Historically and vs Inflation

CPI YoY% vs 6m and 12m Rolling Change in FCI-G

Source: FOMC, Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

We think Kevin Warsh faces a choice between allowing markets and the broader Committee to question his commitment to the inflation target at his first meeting or taking his own advice that once you let inflation take hold of the economy, it’s more expensive and harder to bring it down. We think this skews the risk toward more hawkish communication at the June FOMC, and think the risks skew to a rate hike at the September meeting.

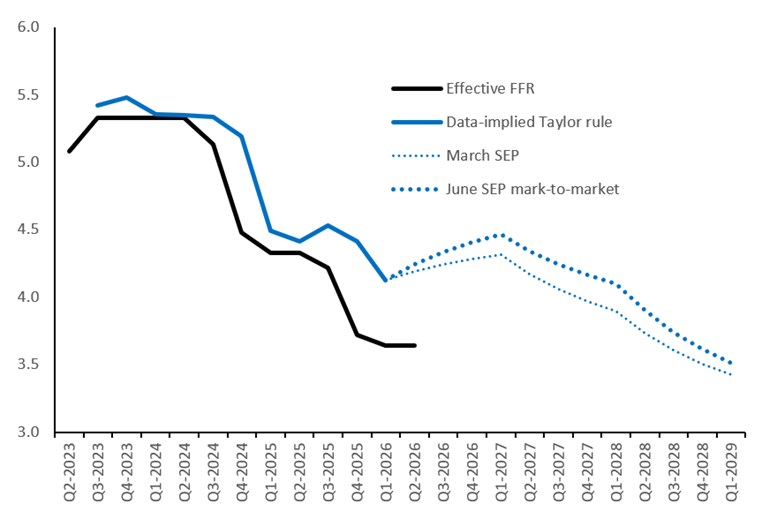

Our Expectation of the FOMC’s June SEP

Expected Change in FOMC Set of Economic Projections in the June Meeting

Source: Citadel Securities, Jun-26. Figures are for illustrative purposes only.

On communication in the June meeting, we expect the Committee to remove its easing bias, think the SEP is likely to show no cuts in 2026, with a risk that 5+ participants pencil in hikes, alongside an upgrade to 2026 core PCE to >3.0% and a slightly lower unemployment-rate projection. This forecast mix may still look somewhat dovish relative to the underlying economic reality, but a materially more hawkish set of projections would likely be difficult to square with an on-hold policy stance at the June meeting. Taking these forecasts alone and plugging them into an inertial Taylor Rule implies an optimal policy path of 75bp of hikes this year. Furthermore we would be cautious about placing too much weigh on the 2027 projections given the unusually high uncertainty around the inflation path, and we suspect the FOMC will be reluctant to anchor to back year inflation trajectories when making policy decisions.

Taylor Rules Imply 75bp of Hikes Based on Modest Changes to June SEP

Inertial Taylor Rule Outcomes Based on Projected June SEP vs Mar SEP

Source: FOMC, Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

We see the natural policy sequence thereafter as likely to result in the July statement shifting towards a hiking bias, setting up a September hike. We think the market has under-indexed to the hawkish shift in recent FOMC communication, particularly from Waller, and over-indexed to the framing of Warsh as a dove, which contrasts with his record as a Fed governor. We think Warsh is likely to avoid explicit forward guidance, but in the context of a more hawkish SEP and statement, that restraint itself may sound hawkish given the market’s learned experience of dovish Powell pressers. Should Warsh pass up on the opportunity to push back against the pricing then that would leave the market free to follow the data. The evidence suggests policy should be moving in a clearly hawkish direction, and we think Warsh will choose to preserve inflation credibility rather than validate the market’s dovish prior. We think the risks skew towards Fed hikes in September ‘26, December ‘26 and March ’27.

Wage Growth is Highest in the Most Cyclical Sectors

Average hourly earnings, production & non-supervisory employees, 3m annualized growth, SA

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

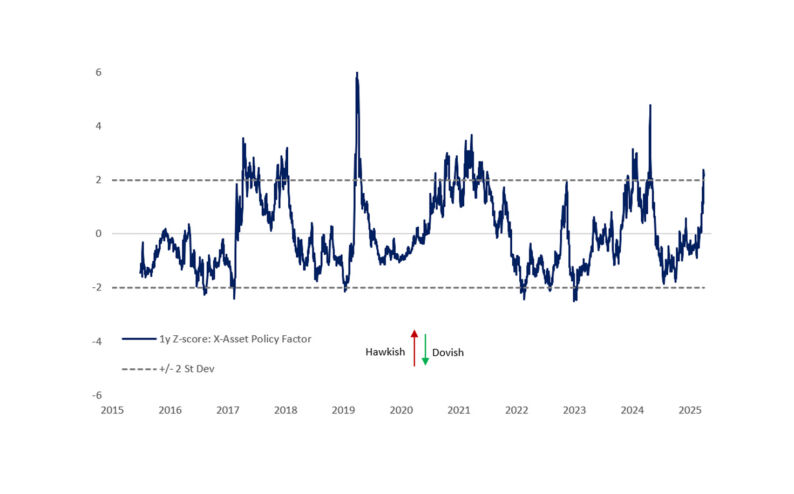

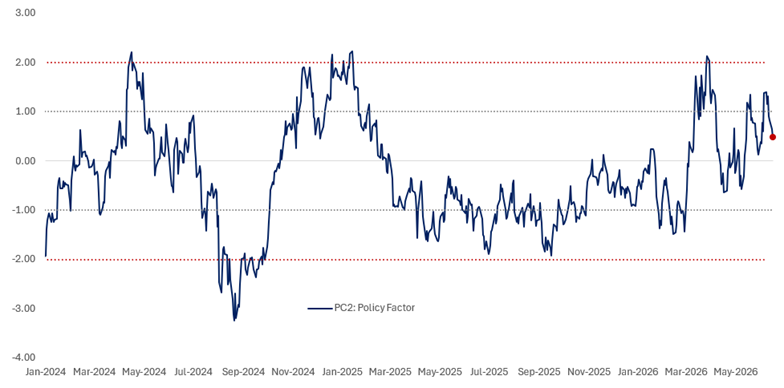

From a markets perspective, we think this outlook is validated by our macro framework, in which we decompose moves in broad macro markets into their macro drivers (Growth and Policy). The framework implies that the performance of risk assets is largely offsetting the sell off in front end rates and policy pricing sits at just +0.48 st deviations, in the 58th percentile of its 5y history, implying there is plenty of room to price a more hawkish policy pathway.

Our Cross Asset Macro Framework Implies Policy Pricing is Not Particularly Hawkish

Second Principal Component of our Cross Asset Macro Framework: Policy Factor

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

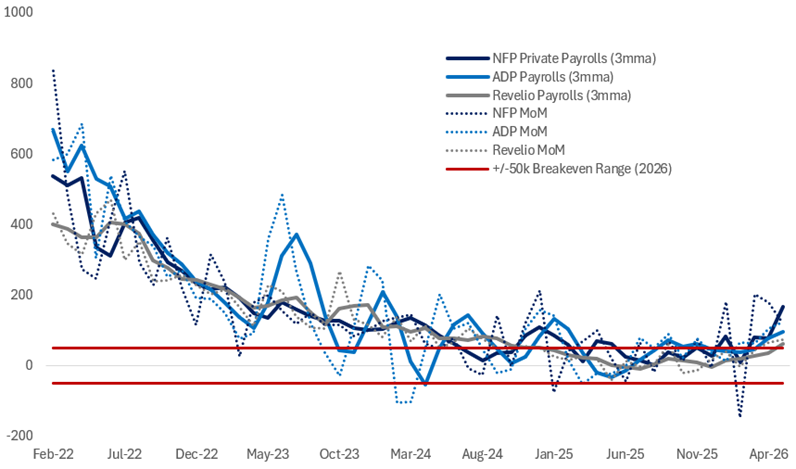

Labor Demand is Accelerating Amid A Very Low Breakeven Rate

Private Sector Payrolls: Establishment Survey, ADP, Revelio, 3mma

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

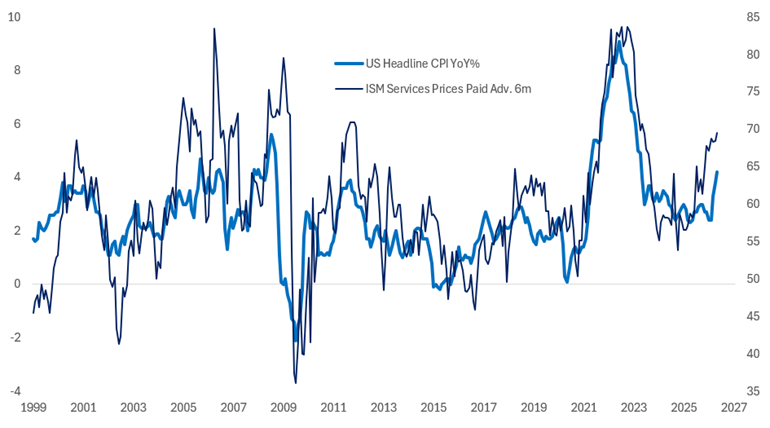

Forward Looking Inflation Indicators Point to Upside Risks Ahead

US Headline CPI vs ISM Services Prices Paid

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

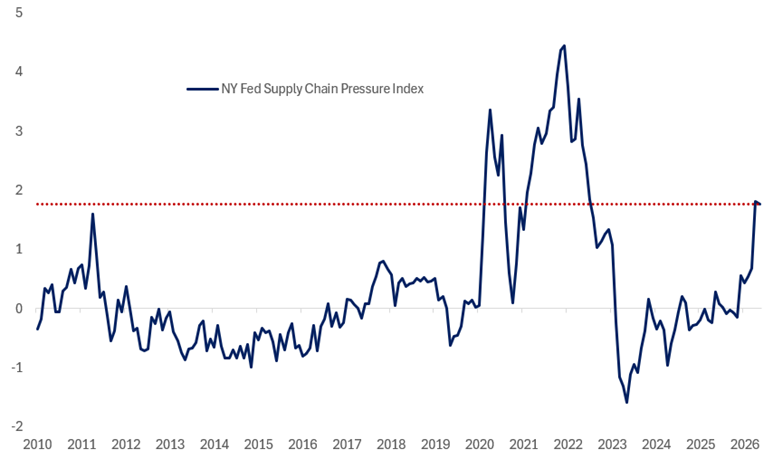

Supply Chain Pressure is Consistent Early Post Pandemic Period

NY Fed Supply Chain Pressure Index

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

High Frequency Economic Activity is Accelerating

Dallas Fed Weekly Economic Activity Index

Source: Bloomberg, Citadel Securities, Jun-26. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.