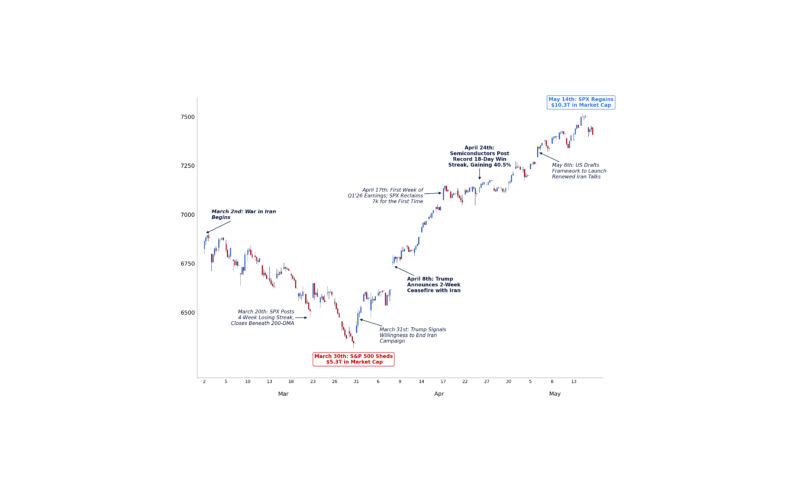

Markets have extended their recent rally, with the Nasdaq now on a 10-day winning streak and the S&P 500 up nearly 10% over the same period – adding approximately $5.5 trillion in market capitalization.

The S&P 500 posted its highest closing price yesterday and now sits just ~35bps below all-time highs.

Against this backdrop, we are revisiting our April Checklist, which has now largely normalized following the dislocations observed three weeks ago. Positioning has reset, volatility has compressed, and flows are re-engaging, marking a meaningful shift in the underlying market backdrop.

As we move into the heart of earnings season, focus is shifting back toward fundamentals, with a more idiosyncratic, stock-driven environment beginning to take hold.

At the same time, a supply and demand imbalance is emerging as non-economic strategies re-lever, institutional investors add risk, retail re-engages following tax season, and corporates re-enter the buyback window.

I. Earnings: High Bar, Low Positioning

As earnings season begins, the market is rotating back toward fundamentals, with company-specific drivers reasserting themselves after a more flow-driven period.

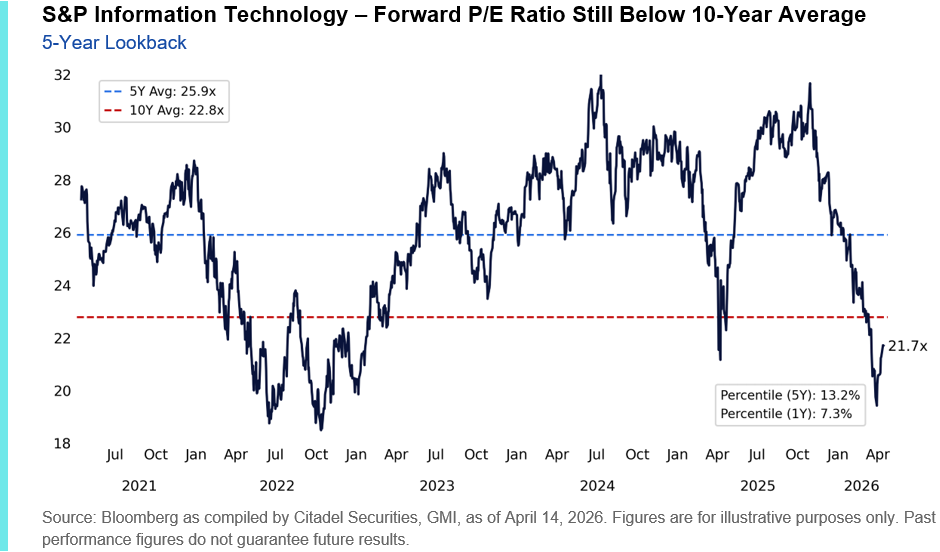

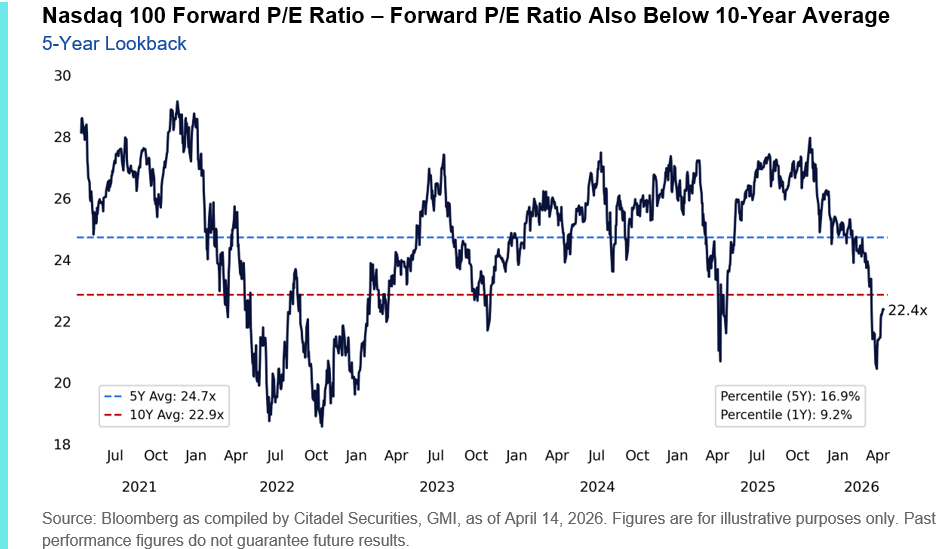

Valuations Reset

Valuations have compressed meaningfully into earnings, particularly in technology, with both the S&P 500 Information Technology Sector and the Nasdaq trading below their 10-year average forward P/E multiples. This reset provides a more constructive entry point in equities, particularly across large-cap quality growth.

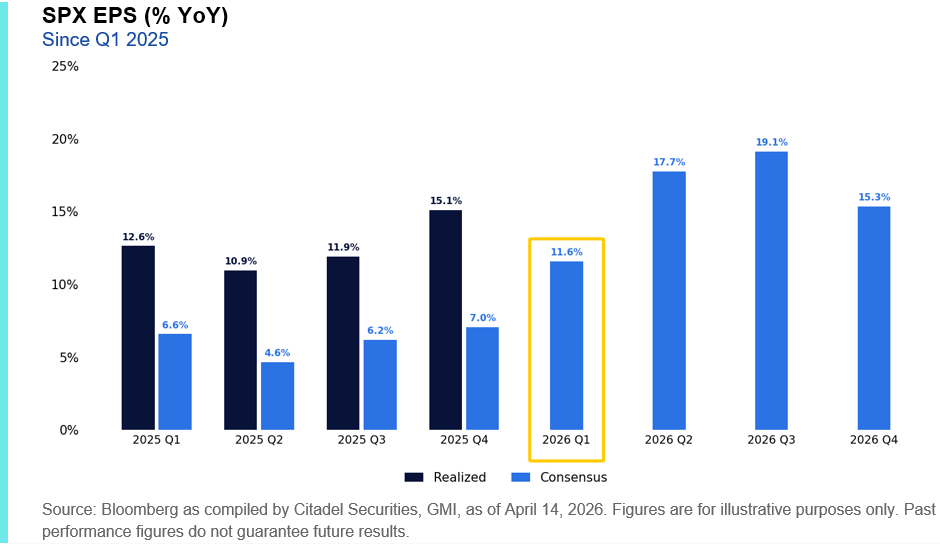

EPS Trends Remain Constructive

The setup into earnings remains asymmetric. Positioning is still light following the recent de-risking, leaving room for incremental fundamental buying.

Despite this reset in valuations, EPS estimates have continued to trend higher over the past month. Earnings expectations are for 11.2% year-over-year growth this quarter, the highest since 2021. This “high bar, low net positioning” dynamic creates the possibility that in-line or modestly better-than-expected results could drive outsized upside.

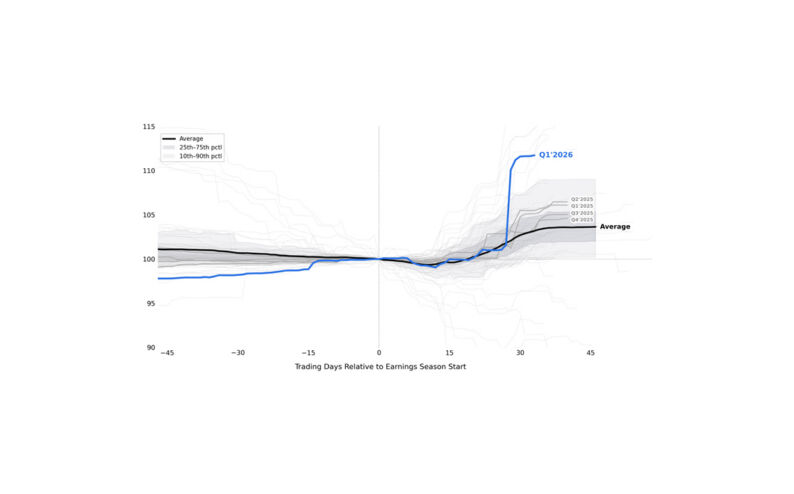

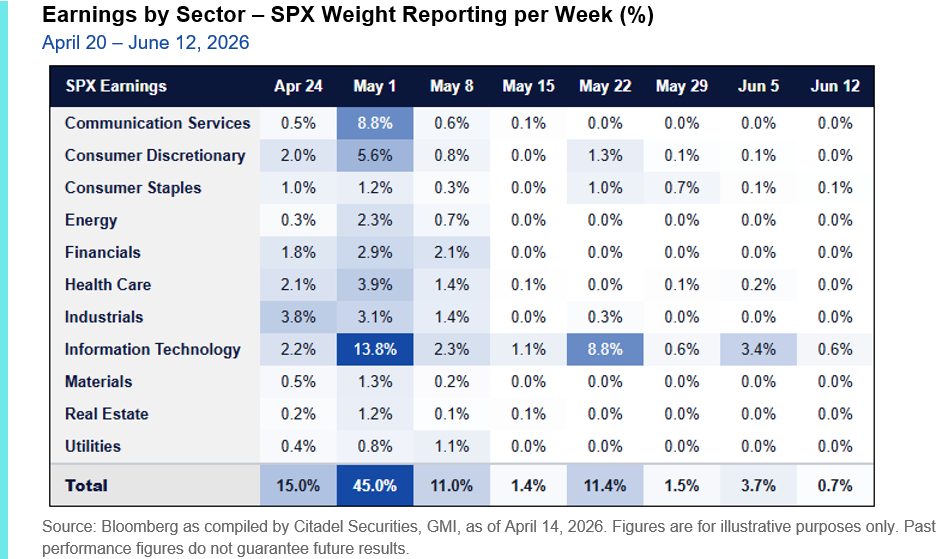

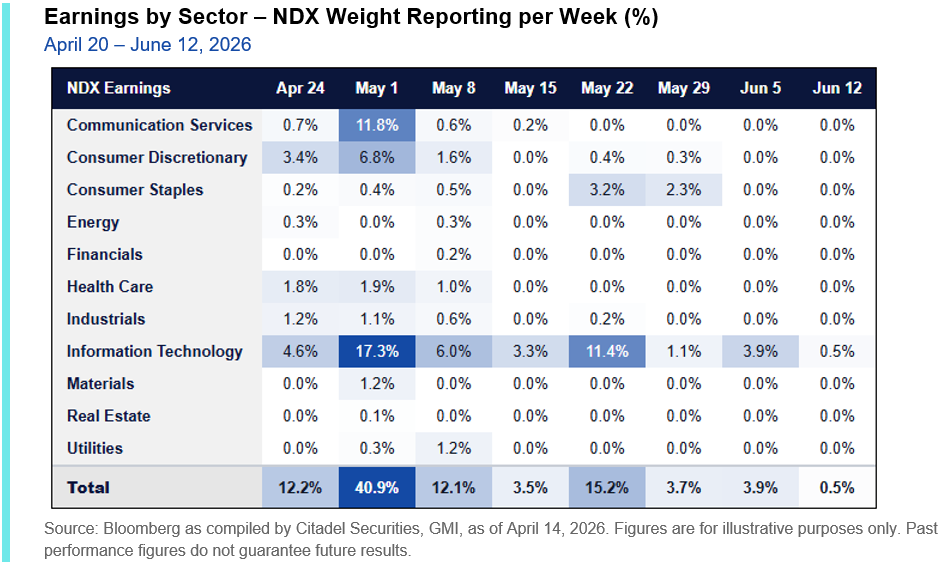

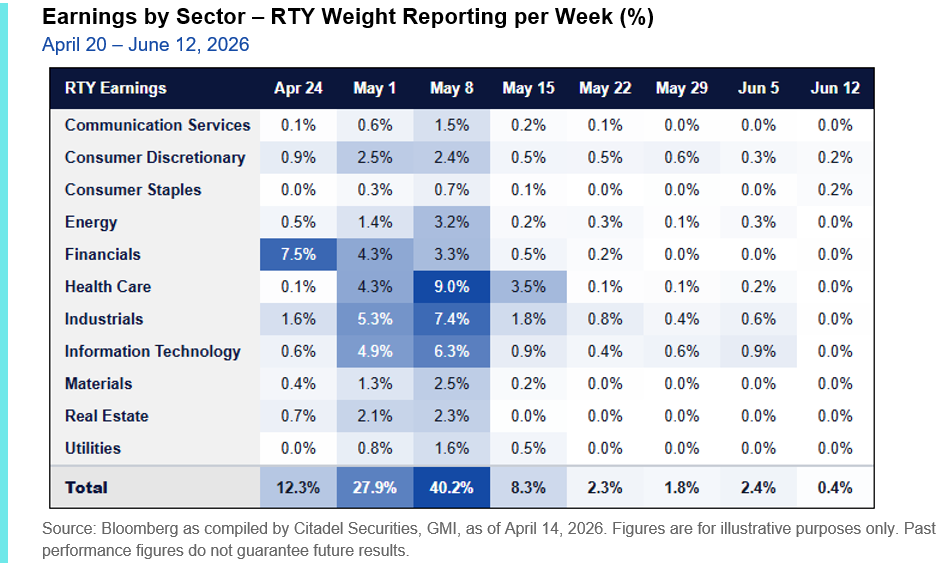

Earnings Calendar: Focus on Late April

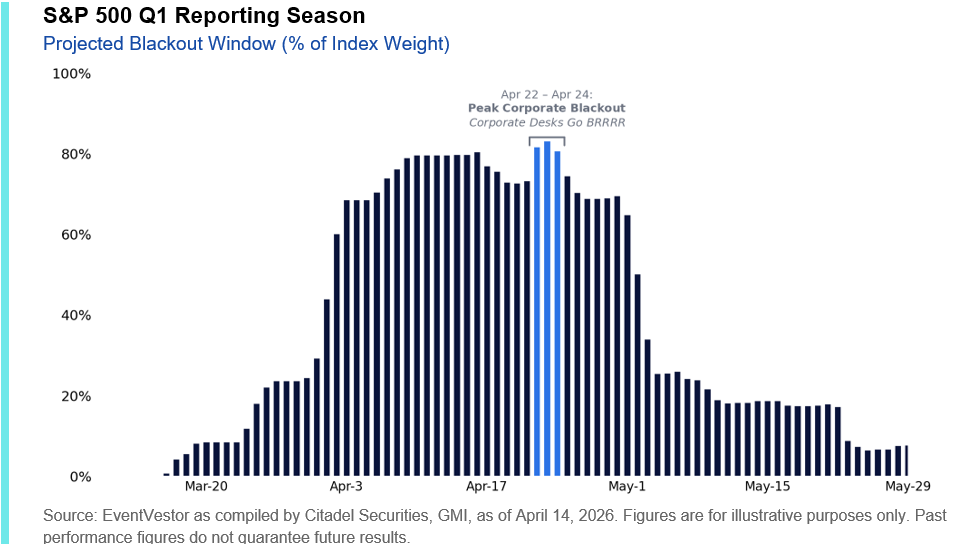

The earnings calendar becomes increasingly important from here, with the final week of April representing the peak of the reporting cycle – particularly for index leadership (Mag7).

The Super Bowl of Q1 earnings will take place from April 27 – May 1. 45% of the S&P 500 and 41% of the Nasdaq 100 will report, including MSFT, GOOGL, META, AAPL and AMZN.

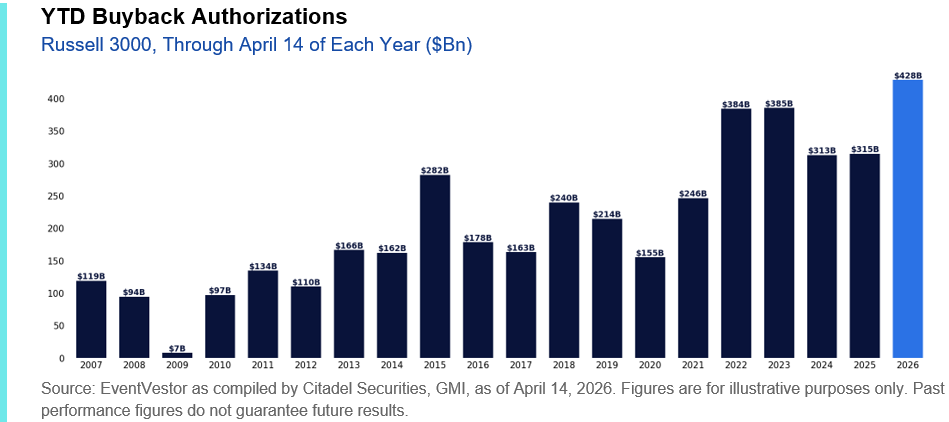

Buybacks Set to Reaccelerate

The flow backdrop improves further into May as the corporate buyback window reopens. While we are currently in peak corporate blackout, the repurchase window reopens in two weeks, providing a tailwind for incremental demand.

U.S. corporates have already authorized ~$428bn year-to-date, the strongest start on record, setting the stage for a meaningful reacceleration in buyback activity. With a 90% execution rate, this means that US corporates are on pace to execute roughly $1 trillion of share repurchases in 2026.

II. Technicals Update

From a technical perspective, conditions have improved meaningfully this month, with several key indicators now pointing toward a more stable and constructive backdrop – an environment where buyers tend to be more active at higher levels.

We revisit the key technical indicators we’ve been tracking to highlight the extent of the recent normalization.

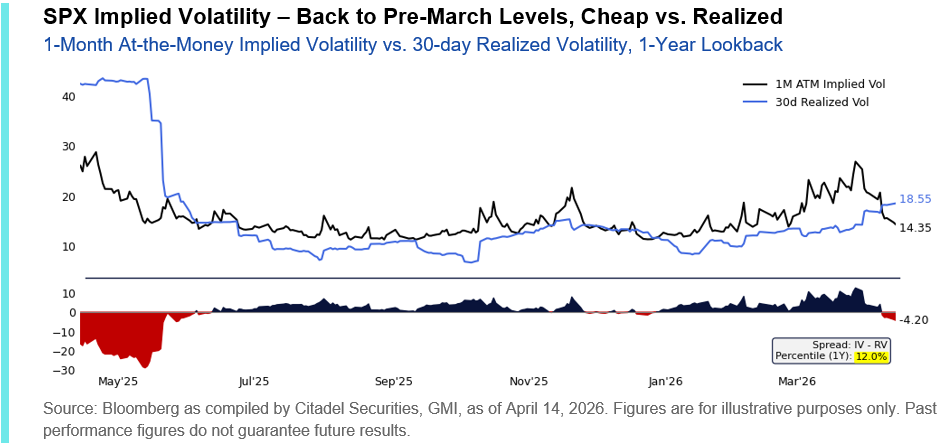

Volatility Has Reset and Remains QB1

The most notable shift has been the speed of the volatility compression (~VIX = 18.00). Vol has compressed sharply across asset classes, with equity volatility in particular retracing a significant portion of the recent spike – resetting positioning and improving entry points for risk.

SPX one-month implied volatility has fallen back to pre-March levels, fully erasing the geopolitical risk premium, and trading at its widest discount to realized volatility since May 2025 (post-Liberation Day). Volatility is no longer the coach on the sidelines; it is the quarterback calling plays in the huddle.

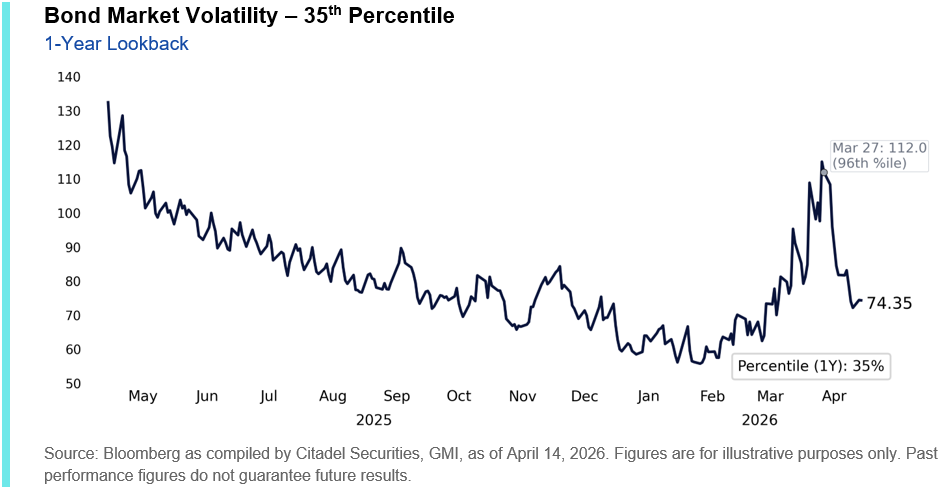

Rates volatility has continued its downward trend as well, with bond market implied volatility back to the 35th percentile of its one-year range.

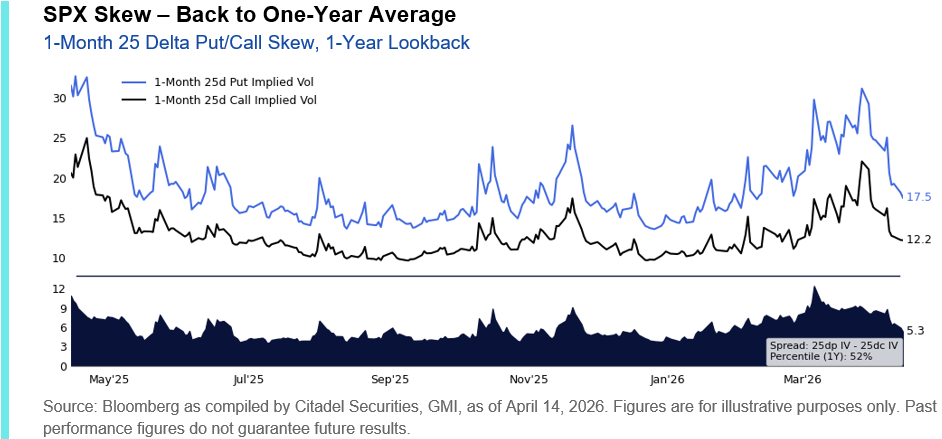

Skew Normalizing, Upside Firming

Alongside the normalization in downside hedging demand, skew has compressed, with SPX 1-month 25-delta skew trading back in-line with its one-year average.

At the same time, upside volatility remains relatively firm, reflecting the growing demand for “upcrash” call options as well.

Systematic Re-Grossing Underway

Systematic strategies (CTAs, Risk Parity, and Vol Control) are beginning to re-engage as realized volatility declines. Early signs of re-grossing are already evident in a flat tape, with these flows likely to provide incremental support on continued stability.

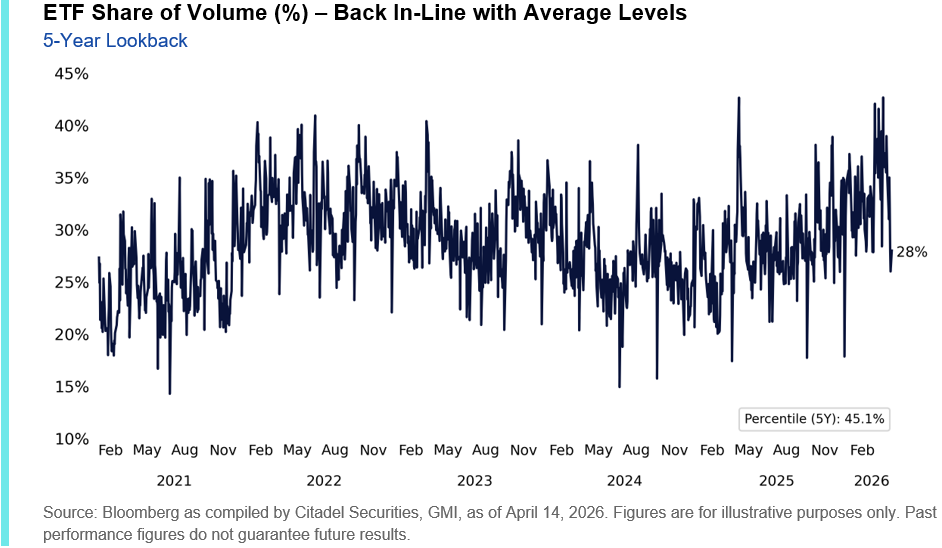

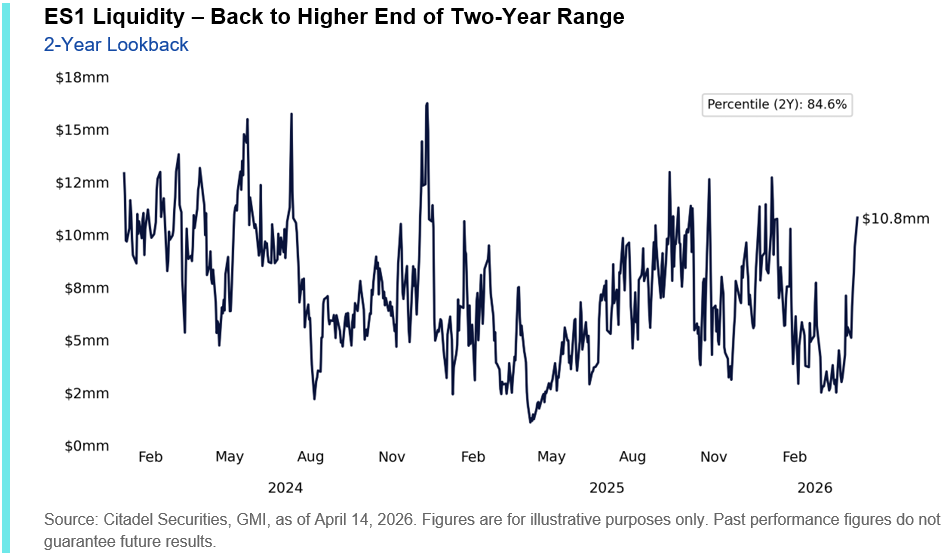

Liquidity and Market Structure Are Improving

Liquidity conditions are quickly improving, with healthier top-of-book depth and more stable market functioning. ETF-driven trading is back toward average levels, as overall macro-driven volumes have begun to decline – pointing to a more normalized trading environment.

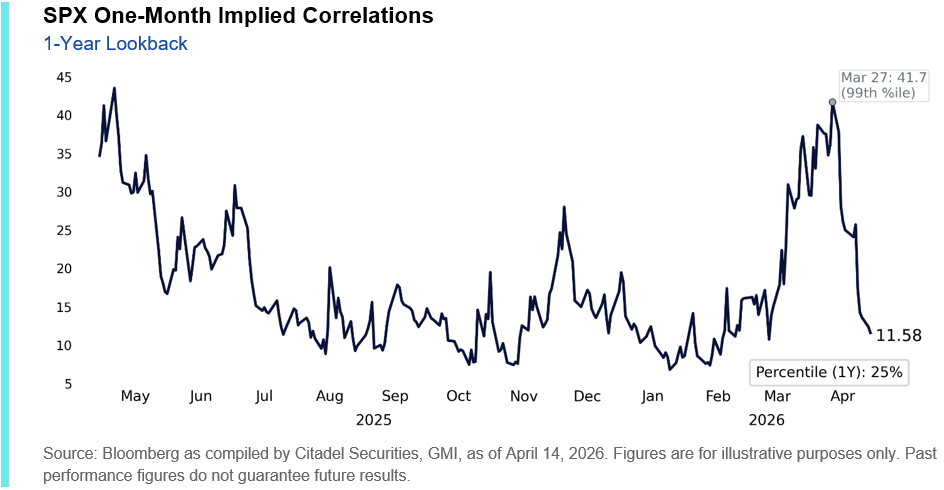

Dispersion Increasing

Correlations are starting to move lower, driving a re-expansion in dispersion. This marks a shift back toward a more idiosyncratic, stock-driven market, where company-specific developments (particularly across favored AI-linked sectors) are once again driving performance.

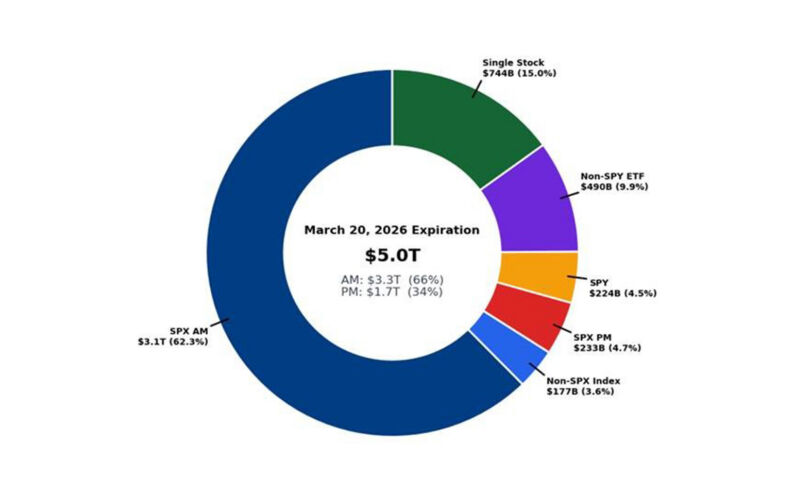

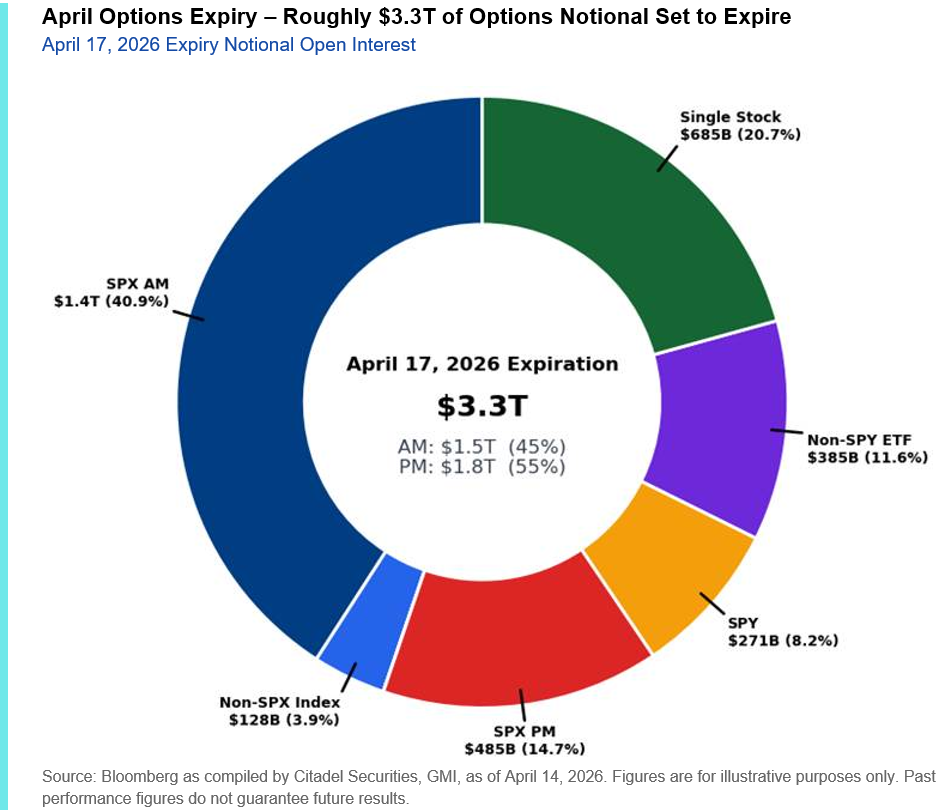

April Expiry Rebuilds Long Gamma Buffer

Following VIX expiry, we are also monitoring April options expiry this Friday. ~$3.3 trillion of US notional options exposure will expire, comprising ~15% of all US options. Long dealer gamma continues to rebuild in the market, providing a stabilizing market buffer. This differs from the “short gamma” environment that we saw during March.

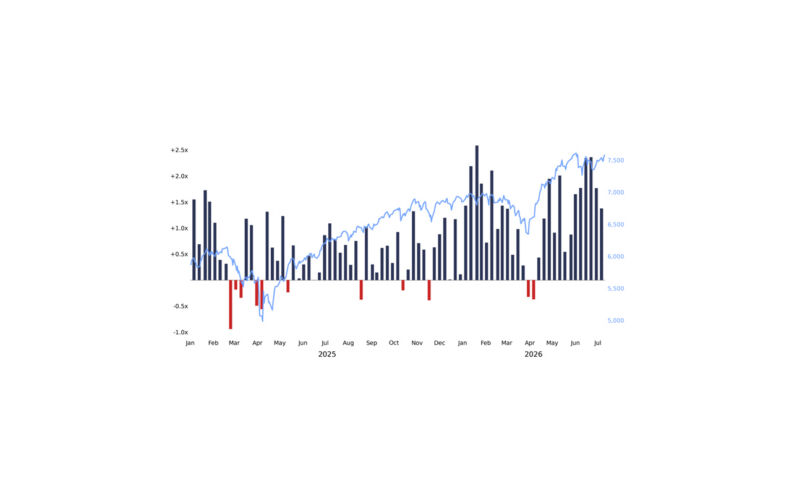

III. Citadel Securities Client Flows: Demand Rebuilding

Flows have continued to improve materially over the past week, with strong signs of re-engagement, particularly from our institutional clients.

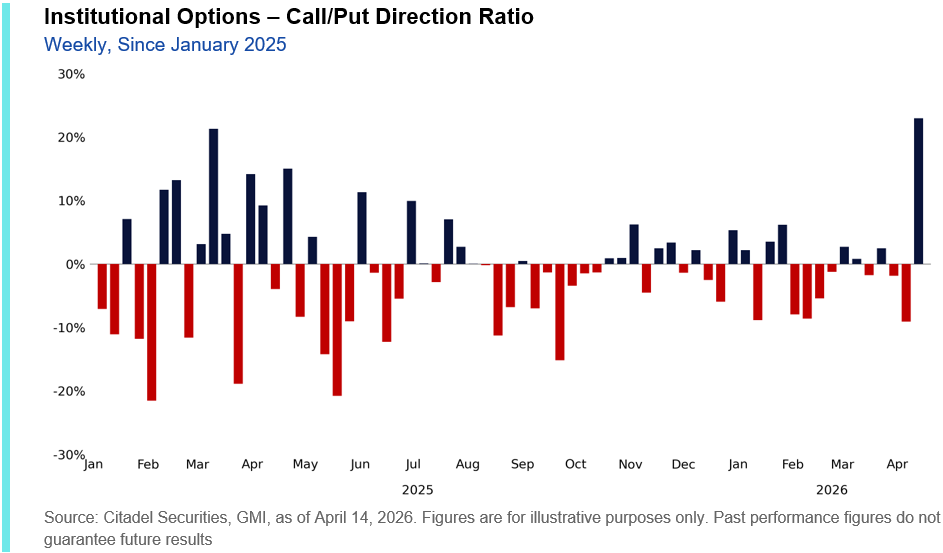

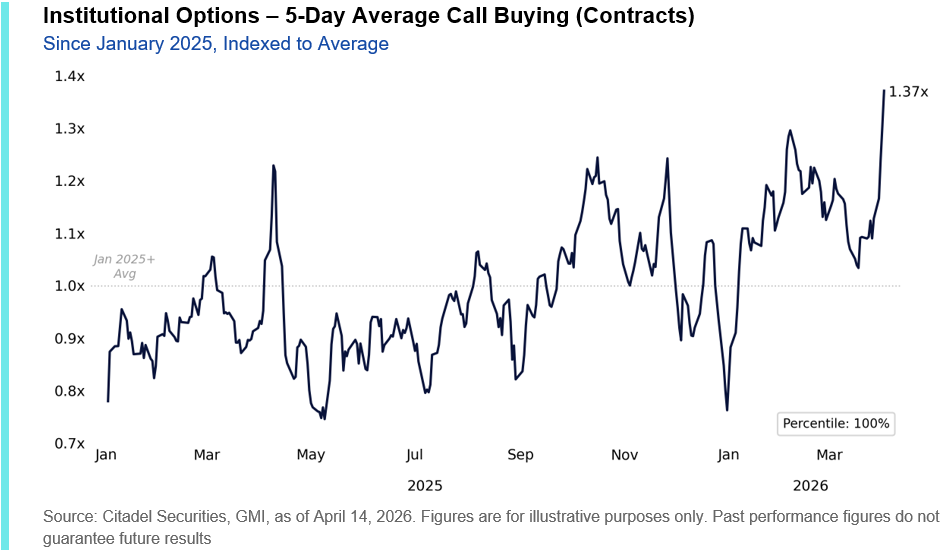

Institutional Demand Strengthening

Institutional option flows turned more constructive toward the end of last week and have strengthened further to start this week, with these past two sessions currently on pace for the largest weekly buy skew on our platform since October 2024.

Positioning is also extending further out the curve, with increased upside buying across June and September expiries – particularly in single names – marking a notable shift away from the more tactical, short-dated activity seen throughout March.

Institutional demand for calls has reached the highest levels we have observed – call buying over the past five days has exceeded any prior rolling five-day period on our platform. This demand has persisted alongside market strength, with the S&P 500 up 5.3% over the same period.

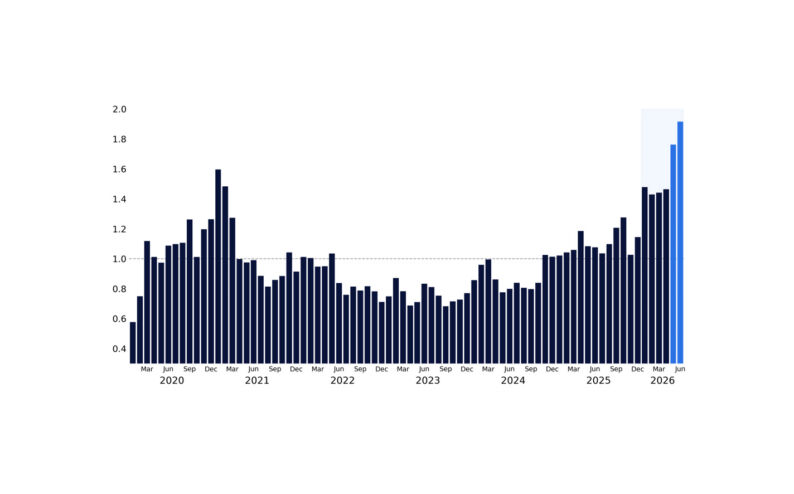

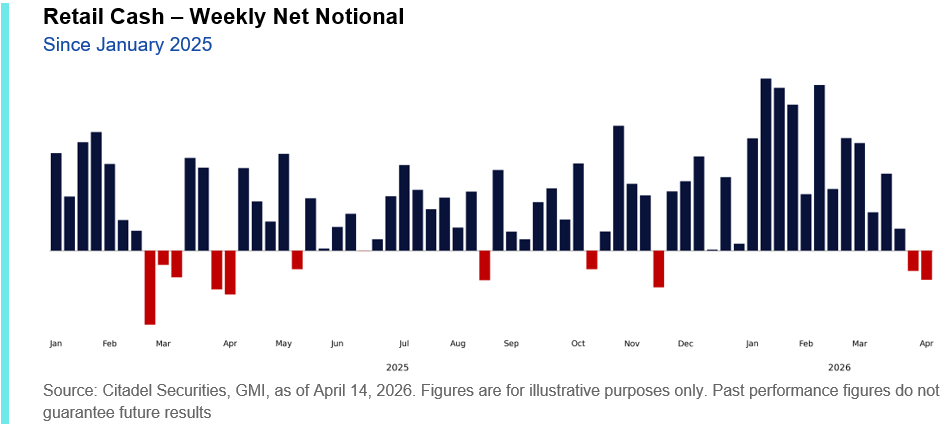

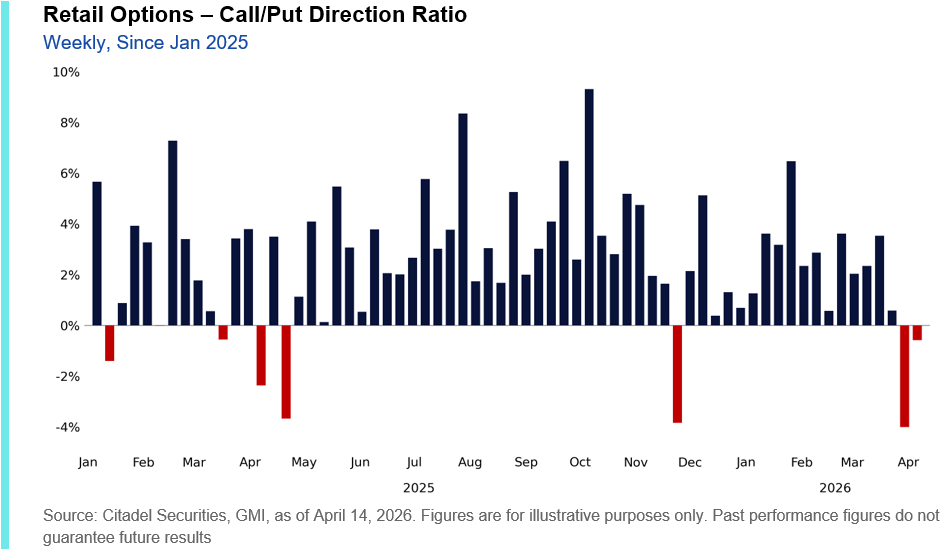

Retail: Set to Re-Engage Post Tax Season

We are seeing further evidence of retail selling pressure, with retail posting a second consecutive week of net selling across both cash and options. This marks the first back-to-back net selling weeks in cash since Liberation Day last year, and the first such occurrence on our options platform since August 2023.

This is consistent with the seasonality of Tax Day, especially after a record year in 2025 for retail traders.

While retail behavior remains largely contrarian (i.e., buying dips and selling rallies), rather than the persistent one-way demand observed earlier in the year, we are beginning to see engagement pick up again over the last few sessions.

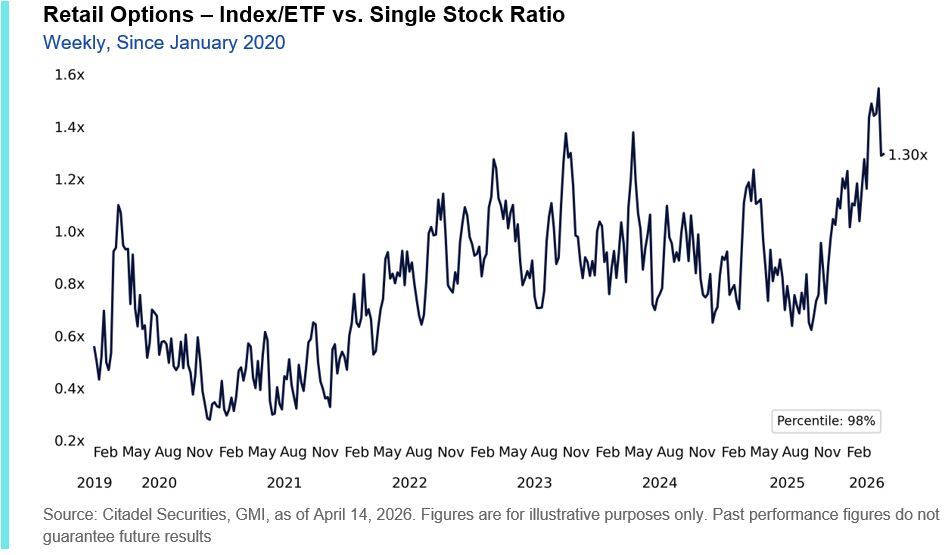

This re-engagement is increasingly important in the context of rising dispersion. We are starting to see early signs of a shift back toward single-stock activity, particularly in higher-beta names. Retail had been heavily skewed toward index and ETF options, trading more than 1.5 index/ETF options for every one single-stock option – the highest ratio we have observed.

We are starting to see a normalization now, with this ratio back to ~1.3x by the end of last week. If retail options participation starts to increase, incremental demand is likely to have an outsized impact, particularly in single names.

GMI BOTTOM LINE

The April GMI setup has largely normalized, with volatility reset, positioning improved, and flows turning more constructive.

As earnings take center stage, markets are transitioning back toward a more idiosyncratic, fundamentally driven regime.

We continue to see scope for further upside, though the nature of the move is evolving – from broad, flow-driven beta to more selective opportunities, particularly across AI and U.S. large-cap technology, as dispersion re-expands.

Copyright © Citadel Enterprise Americas LLC or one of its affiliates. All rights reserved.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CDGE”) authorized and regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch authorized and regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the Japan Financial Services Agency (“JFSA”); and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”), Financial Industry Regulatory Authority (“FINRA”), and Securities Investor Protection Corporation (“SIPC”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC, FINRA, and SIPC, or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity. Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at www.citadelsecurities.com/GlobalSalesTrading.