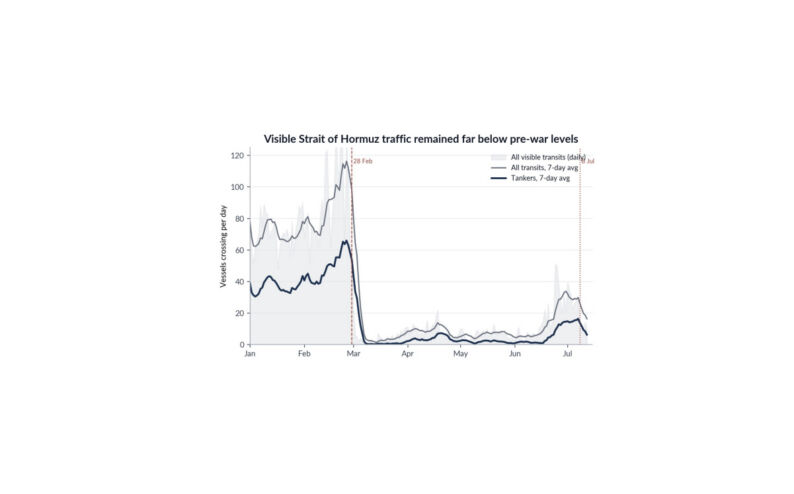

I CAN SEE AN ENDGAME COME INTO VIEW…after almost five weeks of continuous escalation in this war. Even prior to the conflict beginning, I had been warning of the risks to energy markets, the knock-on implications for global growth and inflation, and the extent to which markets were under-pricing those risks. As I’ve been writing, the players in this conflict have appeared caught in a classic escalation trap. US military dominance has never been in question with over 12,000 targets destroyed in a short space of time, materially degrading Iran’s strike capabilities. Yet Iran’s use of asymmetric warfare and horizontal escalation – as is often the case when confronting a much stronger opponent – has proved effective, most notably in closing the Strait of Hormuz, the critical chokepoint for trade in energy, fertiliser, and helium. Polymarket odds now put the probability of a ground invasion by the end of this month at 80%, reflecting peak negative sentiment on the direction of this conflict. This seems too high to me. My takeaway from President Trump’s address to the nation on Wednesday is that the US now appears unlikely to attempt a forcible reopening of the Strait. Doing so would require a far larger troop deployment, including ground operations, with a high risk of casualties and a strong likelihood of rapid regional escalation…potentially drawing in multiple state and non-state actors with severe consequences for energy infrastructure. In my view, the timelines (months of engagement) associated with such a military-led reopening are inconsistent with the President’s typical preference for short, sharp operations and desire to avoid prolonged wars with associated political consequences at home. Instead, POTUS seems inclined to continue with the current pattern of air strikes, while leaving the door open to negotiations with the Strait to “open up naturally” after cessation of hostilities. On the Iranian side, despite the ever-present wartime rhetoric, their responses have retained a degree of proportionality. That suggests, to me, a desire to pause kinetic warfare, while still maintaining control over traffic through the Strait. The key factor for markets, remember, is simply the resumption of transit through this critical energy chokepoint. I can envisage a scenario in which the US steps back over the next few weeks, leaving the international community to negotiate it’s reopening. At that point, Iran would have little incentive to keep it closed to international traffic; its priority would shift toward rebuilding and preserving some semblance of a functioning nation state. European and Asian countries could plausibly claim non-participation in the conflict and therefore be positioned to broker a wide-ranging international agreement…potentially one in which Iran offers more favourable terms to some nations over others. Both sides would be able to claim victory…the US having effectively decapitated Iran’s military capabilities, and the Iranian regime having endured. Ultimately, it is becoming clearer that neither side – having escalated the conflict to this point – is willing to take the next, far more costly step.

Source: Citadel Securities, Bloomberg

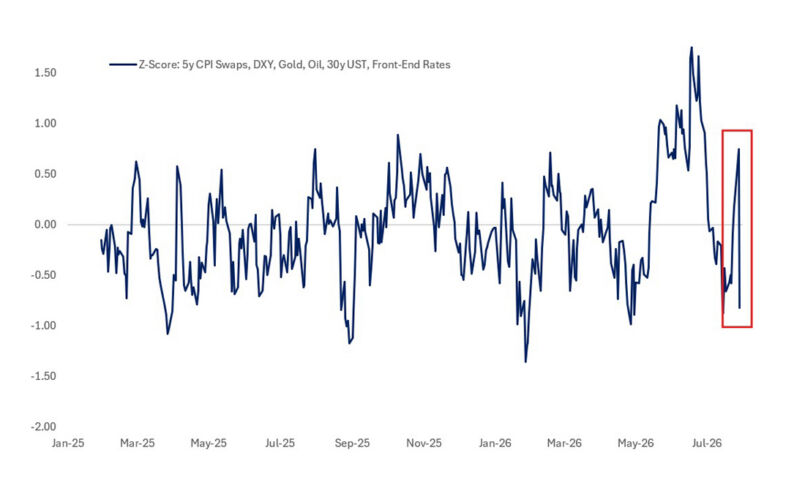

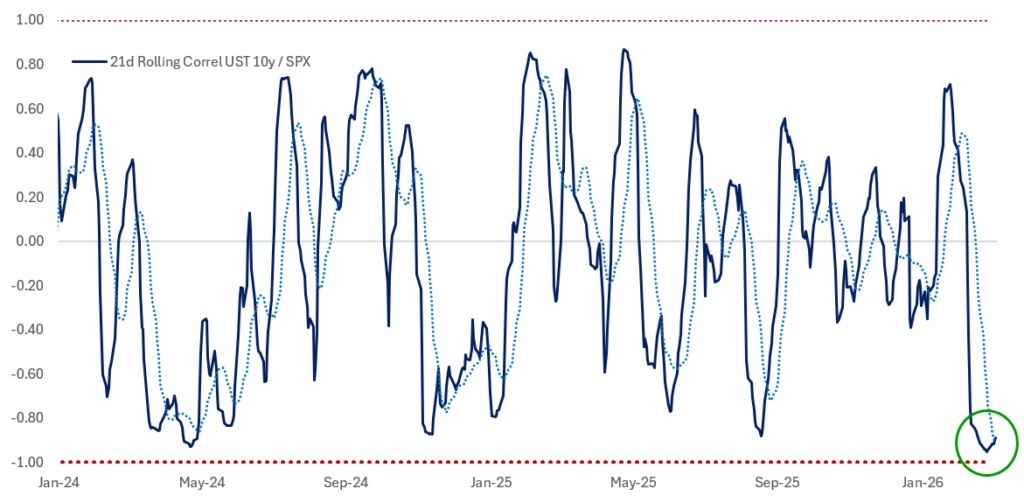

THIS DOES NOT MEAN THE ECONOMIC CONSEQUENCES OF THE CONFLICT CAN BE AVOIDED. Disruption to global energy and trade flows is already material…a substantial rise in headline inflation now looks inevitable…and supply chain disruptions will reverberate around the global economy for months. Higher prices are likely to weigh on consumer confidence, while the uncertainty shock will dampen hiring and investment decisions. It also seems likely that at least some central banks will respond by tightening policy…however, the absence of both a post-pandemic reopening boom and strong fiscal support means the pass-through of this shock into core inflation should be far more limited than in 2022. Inflation expectations remain the key channel through which this could go wrong and are the critical risk to watch. In my base case, I expect one to two hikes in Europe, Australia, and Japan, with the BOE and the Fed remaining on hold, leaving global front-end rates with some room to rally, though not dramatically. The more important point for broader fixed income is that as front-end rates find a clearing level, the belly of the yield curve can price the negative growth implications. The turn in stock-bond correlations in the last week, reflected in the chart above, represents a fundamental shift in how the market trades the next phase of the conflict. I turned bullish on fixed income last week, and the performance since then reflects an emerging dynamic in which duration becomes less sensitive to upside moves in oil as growth concerns begin to dominate, but remains asymmetrically sensitive to downside in oil or de-escalation as a driver of lower yields. I expect fixed income to continue to rally, led by the belly of the curve.

EQUITY MARKETS SHOULD NOW START TO PERFORM…because if my analysis above is correct, the sizeable tail risk associated with worst-case escalation is receding. That includes the risk of further structural damage to energy infrastructure, a months-long commitment of US ground troops – with the attendant risk of a quagmire – and prolonged disruption to global trade. Whilst rates markets will remain focused on the spot outlook, forward-looking equity markets should begin to rally as they grow more comfortable with the contours of the conflict and its implications. Institutional positioning remains relatively light with high gross, but low net exposure, and periods of peak negativity often coincide with ‘under-owned’ rallies. In these phases, equities look through near-term disruption and instead focus on forward earnings, which are likely to remain resilient over the medium term, alongside potential easing in financial conditions driven by lower yields. Stocks don’t just rally once uncertainty has fully resolved…they move as its boundaries become clearer, downside risks are defined, and the focus shifts decisively toward future earnings.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/