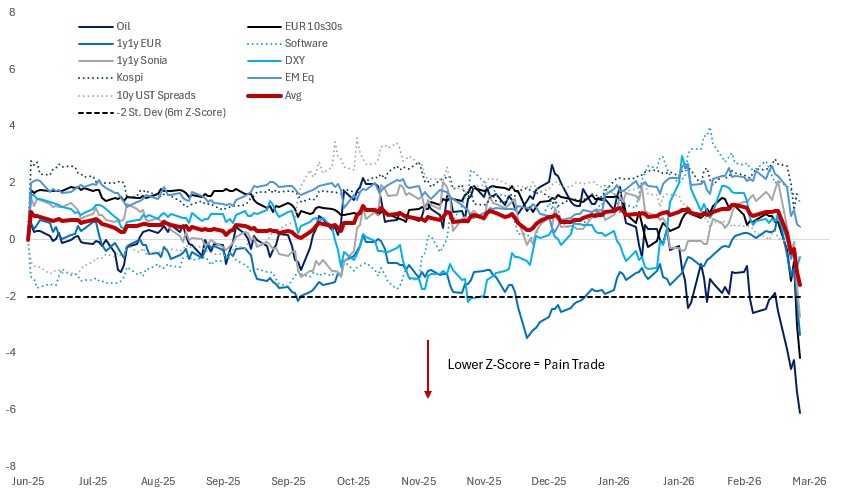

“EVERYONE IS SHORT THE INFLATION TAIL RISK”…was the headline from my note a few weeks back. It has taken a new conflict in the Middle East to awaken markets and investors to this reality. The fog of AI disintermediation – which had been the dominant narrative – is clearing…and the market is now re-calibrating, with inflation fears front-of-mind. This re-calibration has been sharp and painful for much of the macro community, particularly in global rates. Whilst the fundamental outlook had been improving since the beginning of this year (suggesting a more hawkish direction for rates), a confluence of other factors (AI disintermediation fears, credit concerns, expectations of a Warsh-led cutting cycle) had led global rates markets in a dovish direction instead. So, the starting point was already stretched…then you layer on top a meaningful inflationary shock – AIS data for the Strait of Hormuz shows a near total collapse in commercial vessels from ~138 ships/day on average to just 2 at the time of writing – leading crude oil prices to surge above $90/barrel. When this crucial bottleneck for trade is closed, not only does crude movement slow, but finished fuels and refinery feedstock shipments are also impeded because most refined products flow through the same chokepoint. This compounds the impact: crude markets may be able to divert via other routes or storage deliveries, but refined products have fewer flexible arbitrage and rerouting options, especially short-term. That’s why NW Europe jet fuel prices hit ~1,416/tonne (the highest in years) and the price premium for Asia jet fuel briefly hit $200/barrel (compared to ~$25 normally) this week. This is physical tightness…when product cracks explode while crude lags, it’s the bottleneck pricing the true disruption. The Iran conflict has served as a circuit breaker that has snapped the market’s complacency, leading to positional unwinds in widely held carry-orientated trades. This week’s sharp price action was evidence of where those speculative positions had accumulated…1y1y rates (EUR, US, UK)…software stocks (IGV)…RoW equities…and EUR 10s30s yield curve. As always, it’s difficult to predict exactly how much further this deleveraging can continue, but the risk frameworks for most funds imply a quicker, rather than extended process of unwinding positions. Whilst this conflict has served as a catalyst, I do not expect markets to return to trading the prior narrative, even if we see a quick de-escalation – nor do I see much value in fading the moves here. The reduction in front-end rate cut pricing is fully justified in my mind – the market was over-indexing to…accelerating labour market weakness (yet to materialise)…a Kevin Warsh Fed which would cut rates regardless (complicated to deliver)…and AI disintermediation fears (overbaked). Instead, the risk now is that the conflict continues longer than most expect (Polymarket odds for a ceasefire by 31 March sit at 27%, dropping throughout the week) leading to a sustained increase in Crude Oil and Natural Gas prices, further complicating the job of central bankers who have been unsuccessful in bringing inflation back to target. The adjustment higher in yields is something I have been calling for in recent weeks and is justified by the fundamentals, and I expect it to continue.

6m Z-Score: Macro Pain Trades

Source: Bloomberg, Citadel Securities, past performance is not indicative of future returns

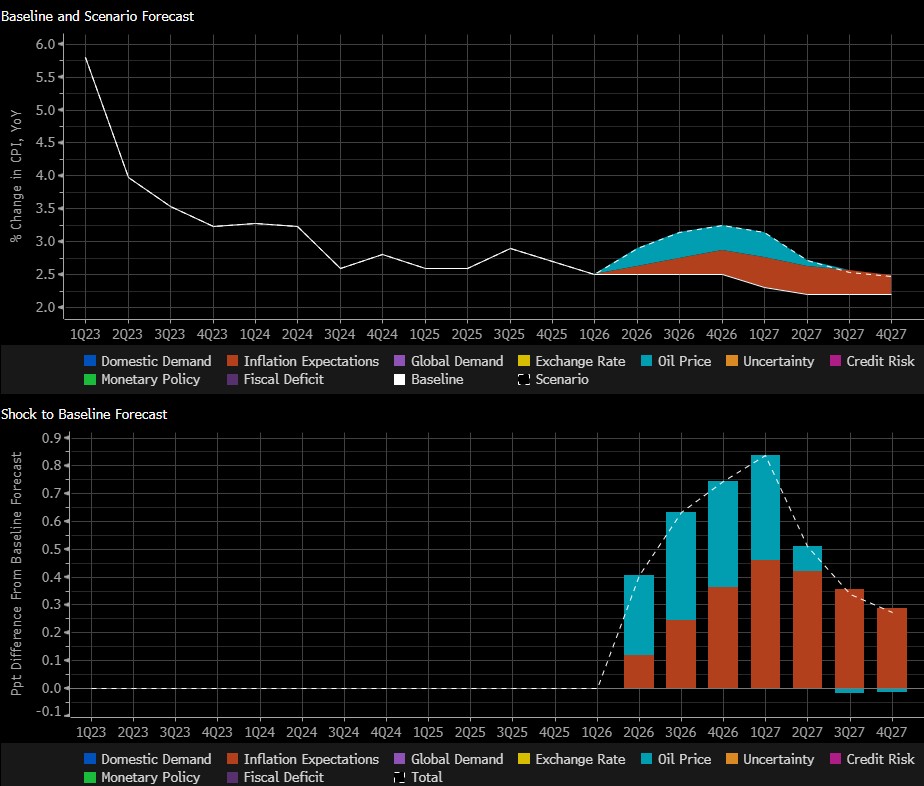

THE FIRST ORDER ISSUE WHEN ASSESSING AN OIL SHOCK IS PERSISTENCE. A short-lived spike in prices feeds quickly into headline CPI, particularly through gasoline…retail gasoline prices are already up ~10%. However, if the move reverses quickly, the disinflationary impulse tends to show up just as symmetrically…the macro impact is largely transitory and mostly confined to near term headline volatility. A sustained oil shock is more problematic. Research, including Fed estimates, suggests that a sustained 10% increase in oil prices lifts US headline inflation by roughly 0.15% on the low end (FOMC estimate) to around 0.3% (using more conventional estimates). Taking the midpoint (0.225%) and applying it to the 26% rise in oil prices since end-February implies a ~0.6% increase in headline inflation if sustained. Using the Bloomberg SHOK model, and holding all else equal, the roughly $20 oil increase observed so far would add 40bp to headline inflation by end 2026, taking it to around 2.9%. However, if inflation expectations were to rise by just 0.5%, the impact of the oil shock nearly doubles…the model implies an additional 35bp increase in headline inflation via the expectations channel, lifting the total effect to 75bp relative to baseline, pushing headline inflation to 3.26% by end 2026. This framework assumes all else equal, which is unrealistic. Financial conditions are already tightening (from very easy levels), volatility has risen, and the dollar has strengthened, which provide partial offsets to the inflation impulse. That said, it’s important to frame the upside risks clearly. I have repeatedly argued that the US inflation process remains vulnerable given its elevated starting point…reflecting tariffs and the easing impulse from financial conditions and fiscal policy…all in the context of strong growth. Importantly, the growth hit from oil in the US is much smaller than in past spikes…the US is now a net energy exporter, which builds natural resilience. The Bloomberg SHOK model implies only a ~0.05% drag on US GDP growth from a $20 oil shock. In contrast, the hit is ~0.19% in Europe and ~0.16% in the UK – with a broadly similar inflation impulse across those economies. In sum, the inflation risk from a sustained oil shock is meaningful, particularly if expectations become unanchored, while the growth drag in the US is modest relative to Europe and the UK. The contrast is important: an upside inflation surprise of 25–30bp in Europe, which would take inflation toward ~2.25–2.3% by end-2026, is unlikely, in my view, to justify a tightening bias, despite markets now pricing ~37bp of ECB hikes by end-2026. Meanwhile, the US still has ~40bp of cuts priced by end-2026, which looks stretched. If the ECB is hiking, I struggle to see the Fed cutting. And vice versa.

Bloomberg: SHOK Model Projected Oil Price Impact on Headline Inflation

Source: Bloomberg, past performance is not indicative of future returns

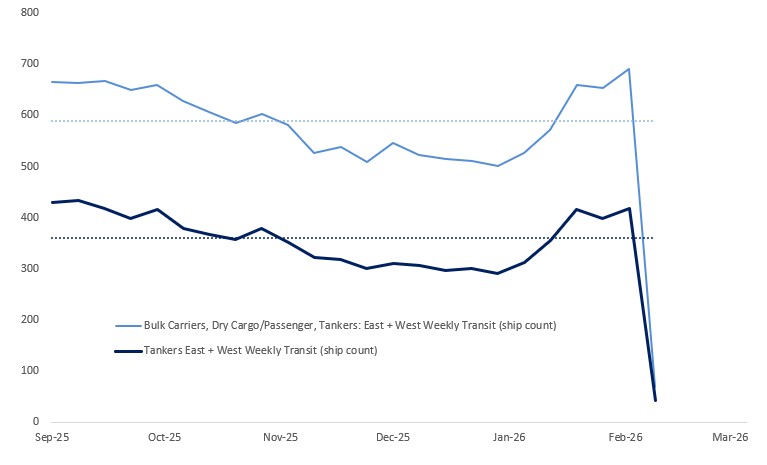

WHAT HAPPENS NEXT? With up to 30% of global oil supply transiting the Straits of Hormuz, there is no doubt we are facing some fat tails in the event of a prolonged conflict that closes the straits for months (rather than weeks). Should this key passage remain closed, the extent of disruption to the flow of both oil and refined products could rapidly become extremely disruptive for the global economy. Markets are not (yet) pricing this risk fully. The base case is a rapid degradation of Iranian military infrastructure in the face of US and Israeli attacks, quickly asserting total air dominance to destroy ballistic missile launchers. Interceptor missiles have proven effective against Iranian attacks…but there is a mismatch between the use of these expensive missiles (which will eventually run scarce) and the cheap shaheed drones (likely still in plentiful supply) used by the IRGC. The use of these cheap but lethal drones to both attack GCC countries and target commercial vessels remains the key ongoing risk. Reports suggest that Iran has the capacity to produce 10,000 drones per month…which could mean the disruption continues for some time. Moreover, one should not underestimate the difficulties in insuring (despite suggestions of intervention) and crewing tankers in the climate of these drone attacks. The strategic objectives of this war have remained fluid…but at this point, from an economic perspective, the incentives of the US, GCC countries…and even China are the same – to achieve a swift resolution and mitigate against a large-scale shock to energy markets causing widespread damage to economic growth and inflation. Beyond the more obvious reasons for this conflict (and the one in Venezuela) it’s useful to view them through the lens of US-China relations. In 2025, China effectively leveraged its near monopoly on rare earths to counter President Trump’s tariff policies. The move demonstrated China’s ability to create bottlenecks in crucial supply chains, forcing the US Administration back to the negotiating table. POTUS’ recent actions are a show of military strength against countries in China’s sphere of influence – the combined impact of Venezuela and Iran affects 17% of China’s oil supply. And yet, China has been unable or unwilling to counteract these actions. This creates a dramatically different backdrop ahead of April’s Summit between Xi and Trump…with a stronger hand for Trump providing greater scope for a deal on improved US terms.

Ship Passage Through Strait of Hormuz

Source: Bloomberg, Citadel Securities, past performance is not indicative of future returns

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/