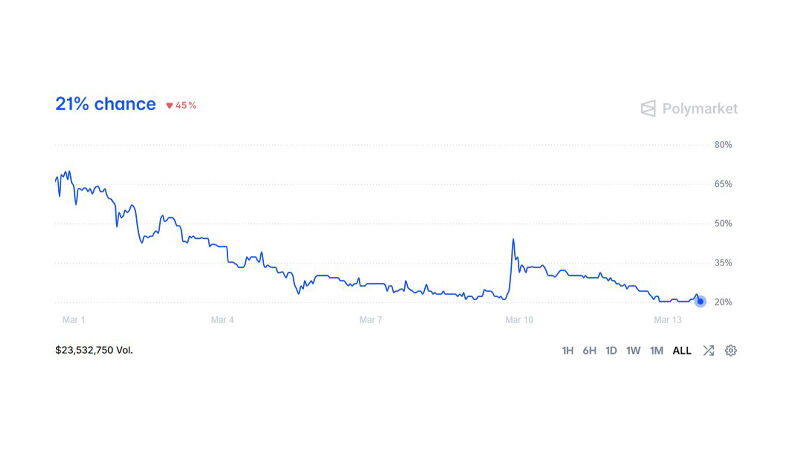

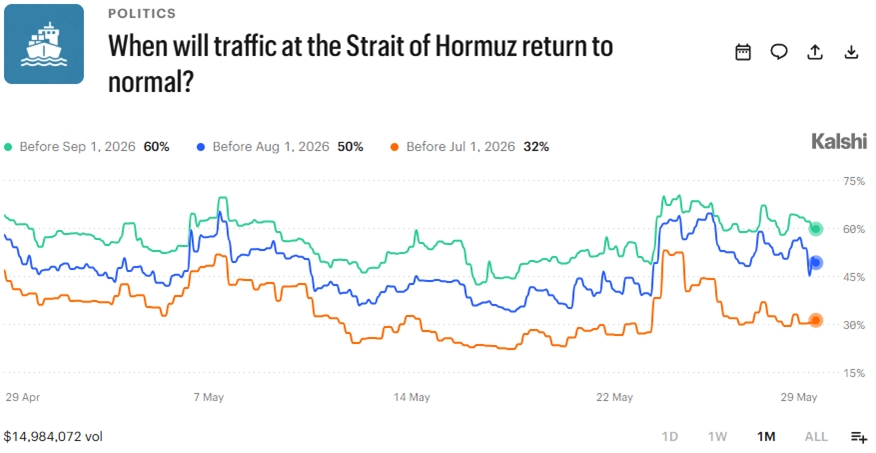

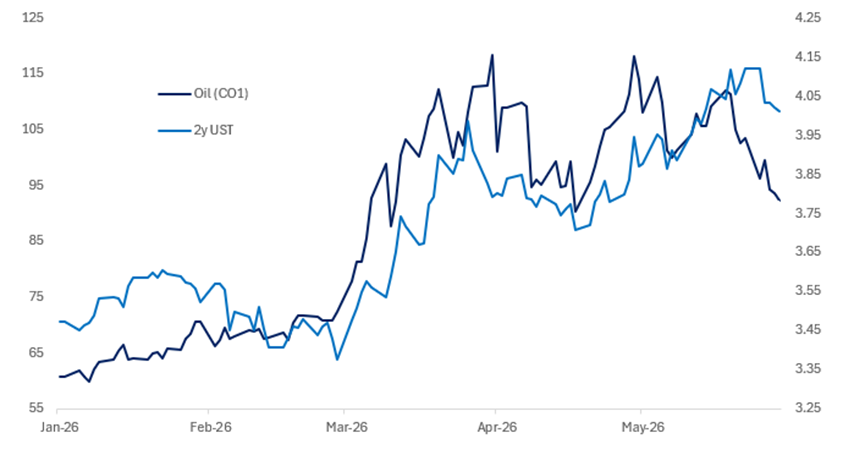

SINCE THE INITIAL NEWS OF PROGRESS ON US-IRAN NEGOTIATIONS, FRONT MONTH OIL FUTURES HAVE DECLINED ~12%…and I expect this to continue as we converge on the likely announcement of a memorandum of understanding between the two parties. While markets appear optimistic that an MoU will extend the ceasefire, there is considerably less confidence in the speed with which the Strait of Hormuz can return to normal operations. This reflects three key concerns: uncertainty over the timeline for reopening, logistical bottlenecks created by the accumulation of trapped vessels, and the lingering risk of mines disrupting shipping traffic, which may continue to weigh on insurance availability and overall risk appetite. My sense is that any agreement is likely to incorporate an aggressive timeline for reopening the Strait, reflecting the political sensitivity of US gasoline prices and their importance to public perceptions of President Trump’s handling of the Iran situation. Moreover, I am optimistic that the physical restoration of tanker flows could happen relatively quickly, as the core infrastructure for movement through the Strait remains intact and the backlog of vessels can be cleared through staggered convoys, prioritization of outbound crude cargoes and the rapid return of insurers once state guarantees or naval escorts reduce perceived tail risk. Some mine-sweeping is likely required, but this can be achieved through international co-operation and route verification can act as a mitigating factor in the meantime. In addition, there have been reports that the deal could contain a 30-day timeline for a return to “normal” transit through the Strait, which would be an upside surprise relative to prediction market pricing which implies only a 32% chance that traffic returns to normal before 1 July and 50% probability by 1 Aug. The broader point here is that the current premium in physical oil creates a strong incentive for physical commodity traders to find a way to get tankers through the strait shortly following a greenlight from the agreement. This is also in line with the interests of the US and Chinese Presidents. Of course, there will be bottlenecks, but the first order bottom line is that if we see a large volume of tankers freely flowing through the Strait in a short space of time, markets will be surprised to the upside. This will be the driving force in macro markets in the short term.

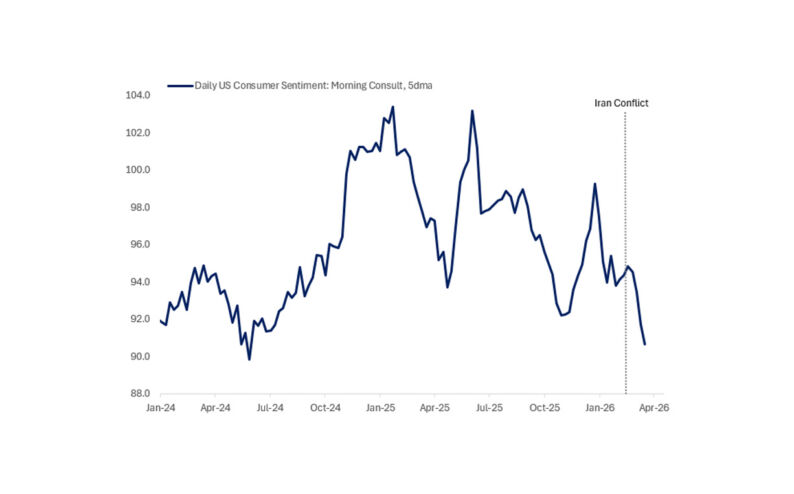

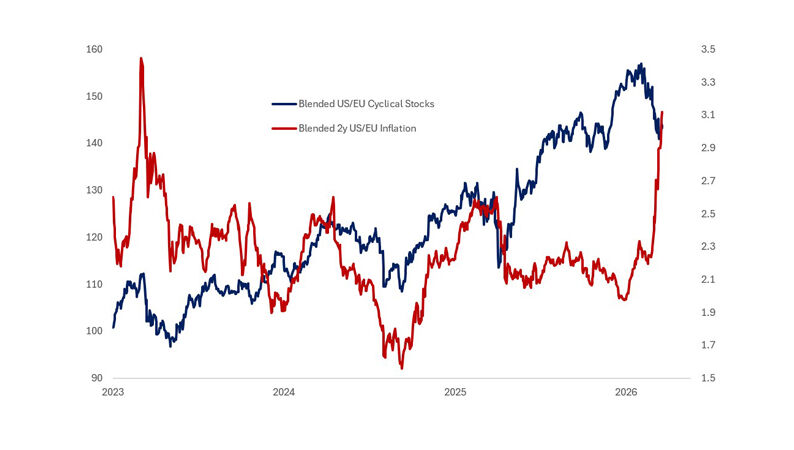

THE COMPLEXITY FOR POLICYMAKERS IS GRAPPLING WITH A ONCE-IN-A-GENERATION AI TRANSFORMATION ALONGSIDE SIGNIFICANT SUPPLY-SIDE SHOCKS. The central challenge is to distinguish cyclical developments from structural change, a theme I have discussed before, because the appropriate policy response depends on that distinction. New Fed Chair Kevin Warsh has been a vocal advocate of the productivity gains that AI could deliver, and the conventional narrative is straightforward: higher productivity lowers costs, eases inflationary pressure, and supports stronger growth. But as I have argued for some time, AI may prove inflationary before it becomes deflationary…and well before any measurable productivity gains appear. A thoughtful recent paper by Simone Lenzu of the New York Fed makes a similar point, arguing that AI blurs the traditional distinction between cyclical fluctuations and structural change, making standard macroeconomic indicators harder to interpret. The transition to AI may initially raise costs through implementation expenses, worker retraining, and organisational disruption, while also changing labour demand, production processes, and pricing behaviour in ways that weaken the relationship between slack and inflation. Traditional indicators such as unemployment rates and output gaps may therefore become less reliable guides for policy. At the same time, expectations of future AI-driven productivity gains can boost investment, spending, and asset prices long before those gains are visible in the real economy, creating the potential for a widening gap between market expectations and realised economic performance, something we are arguably witnessing in equity markets today. And if AI does ultimately deliver meaningful productivity gains, it could raise both the economy’s growth potential and the equilibrium real interest rate, forcing central banks to reassess what constitutes neutral monetary policy, or r*. At a fundamental level, AI should not be viewed simply as a positive productivity shock: it has the potential to reshape inflation dynamics, growth expectations, interest rates, and financial stability simultaneously, making economic data harder to interpret and monetary policymaking considerably more difficult. The current phase of the AI transformation could produce a (perhaps temporary) combination of higher inflation, weak measured productivity, and elevated asset prices. Add to that a higher starting point for inflation, reflecting factors such as tariffs and the Iran war, alongside constrained labour supply from sharply reduced immigration – and a jobs market that is starting to look as if it’s inflecting upwards – then inflation quickly becomes the predominant risk for markets.

Source: Citadel Securities, Bloomberg

WHAT DOES THIS MEAN FOR MARKETS? Our estimates imply that a full normalisation of flows through the Strait of Hormuz by end-July would be worth around -12.5bp in 10y rates, +1.75% in the S&P 500 and -0.5% in the broad dollar. Extending the same analysis to oil would mean prices falling to around $82/bbl. If those macro moves are delivered, they would lead to a further easing in US financial conditions, which should add to the existing growth tailwinds in the US economy and feed back into equity markets through stronger earnings growth. Zooming out, the rally in risk assets has been underpinned by a combination of easy fiscal and monetary policy and robust corporate earnings growth, though performance has remained narrow. Scott Rubner notes that 67% of the S&P 500’s rally since the end of March has come from just 10 companies. I think a reopening of the Strait could catalyse a meaningful breadth expansion as investors rotate into non-tech cyclical sectors. Retailers, homebuilders, and airlines should be among the beneficiaries of energy and rate relief, particularly against a still-strong demand backdrop. As a result, the conditions remain in place for risk assets to continue moving higher. The bigger risk is that, if economic growth continues to strengthen as I expect, alongside ongoing AI capex spending, a more classical inflation process could quickly take hold, creating pressure on the Fed to respond by hiking rates. That risk is not imminent, but it is the key one for investors to watch. The other risk is valuation-induced pressure on equities. Here though, the reality is that we are still working through years of demand for chips, which has been at the epicentre of equity market outperformance, and earnings continue to keep pace with prices. Valuations are simply not stretched enough to suggest an imminent correction.

S&P 500 Breadth – Very Few Names Have Outperformed the Index

Rolling 30-Day Stock Returns – SPX Return, 30-Year Lookback

Source: Bloomberg as compiled by Citadel Securities, GMI, as of May 29, 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/