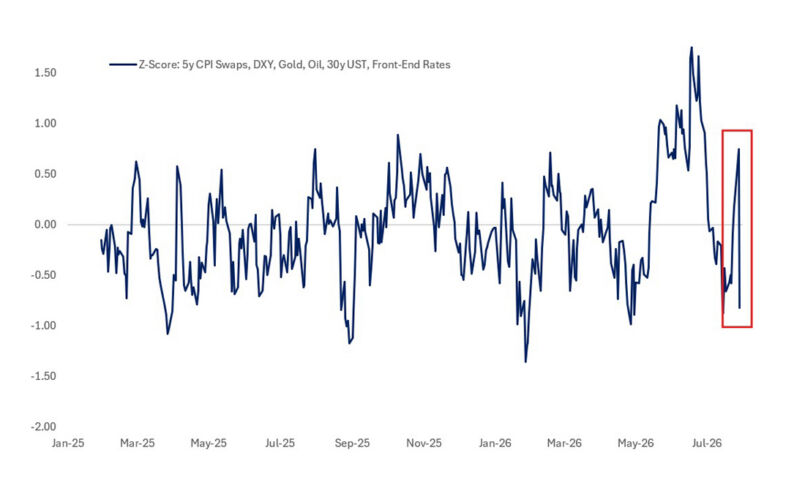

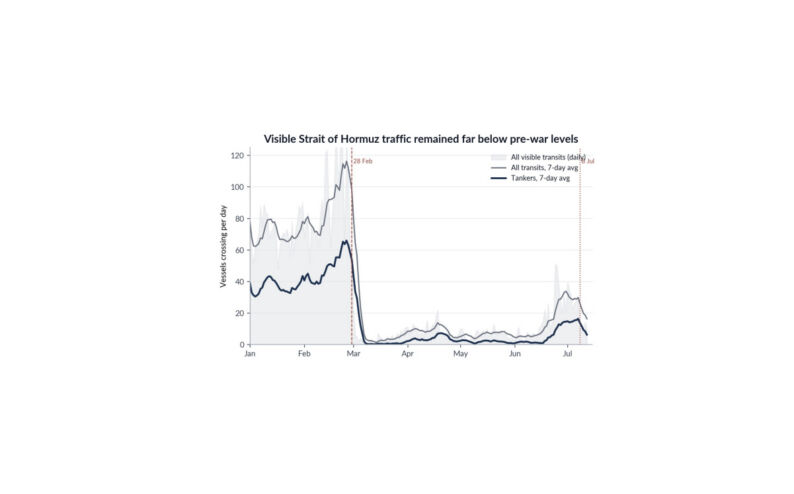

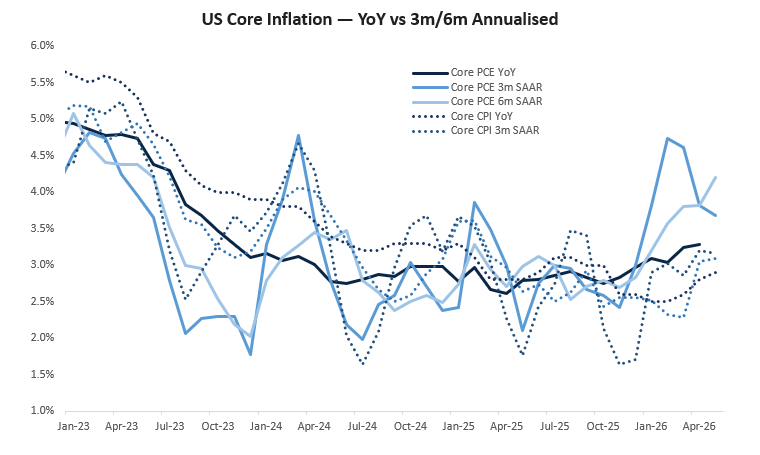

Financial conditions have started to tighten in response to a US economy that continues to signal “more growth, more inflation”. This week’s CPI data confirmed that inflation remains uncomfortably high for the Fed…Core CPI came in at 0.21% MoM (below consensus, driven by a soft-core goods print)…however, core services ex-housing accelerated to 3.7% signalling concern not only from energy and tariffs. Incorporating the hotter-than-expected PPI data, Core PCE is now likely to be above 0.30% for May, taking the YoY figure close to 3.4%…materially above the FOMC’s 2% target. Nominal GDP is now tracking north of 6% and alongside a supportive fiscal backdrop and the almighty AI infrastructure boom (more on this below) the labour market is starting to inflect upwards. Given constrained labour supply from the significant changes to immigration policy under the Trump administration, the risk of rising wage growth cannot be dismissed. Moreover, continued uncertainty around a clear end to the Iran conflict means the supply chain and energy price shocks are more likely to be persistent over the medium term. Despite the official closure of the Strait of Hormuz, hundreds of commercial vessels and tankers have reportedly continued transiting via “dark routes” along the Omani coast, often sailing at night with AIS/GPS signals switched off and under US surveillance and air cover. This has kept a portion of Gulf oil exports moving and prevented a complete supply shock. However, volumes remain below normal, transit risks and insurance costs are elevated, and many vessels are still delayed, meaning the arrangement alleviates but does not eliminate pressure on global energy markets. Even if an MoU is agreed, energy prices are unlikely to fall quickly…inventories and SPRs have been drawn down during the disruption and rebuilding them creates fresh demand that can take months to satisfy. At the same time, shipping, insurance, and supply chains need time to normalise, while producers are unlikely to ramp output aggressively until they are confident the agreement will hold. An MoU can remove some geopolitical risk premium, but tight physical balances and restocking demand mean prices are more likely to ease gradually than collapse. I also think that any “big bang” good news momentum for markets has been lost due to the repeated false starts on this issue. In aggregate, this is not an environment in which the Fed can cut rates…in fact, far from it. The market has started to wake up to this reality in recent weeks…as have various members of the FOMC in their speeches. Notwithstanding any external shocks, the next move is likely to be a hike, almost certainly within the year. Is the ~20bps of hikes priced for 2026 enough? Over to you, Chair Warsh.

Source: Bloomberg, Citadel Securities, data as of Jun-26

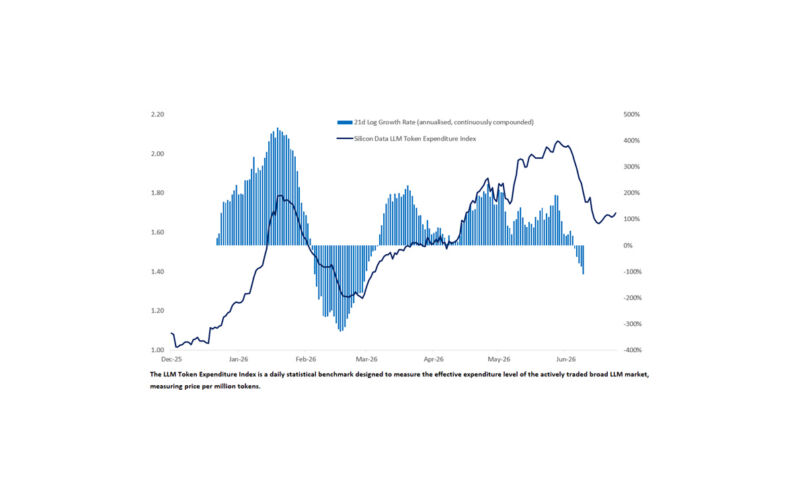

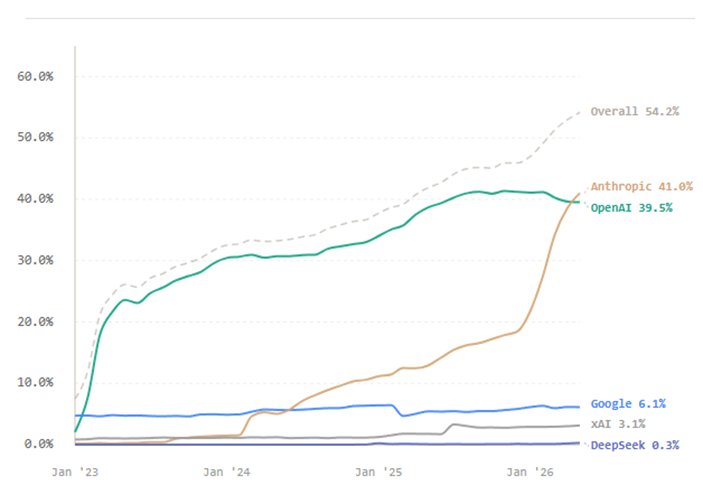

It’s becoming increasingly clear that the market is becoming more discerning around the true costs of AI deployment…and that the “tokenmaxing” phase is likely behind us. This week’s headlines that OpenAI is considering a drastic cut to token pricing are a good illustration of this point: demand for AI appears to be becoming more price sensitive – firms typically do not cut prices aggressively when they are facing unconstrained demand. Some of this may reflect increased competition from Anthropic rather than a broader reduction in demand, but either way the implication for the broader AI theme is more nuanced…and potentially more concerning. The risk is not that AI proves unimportant, but that it becomes increasingly commoditised: a hugely valuable technology that generates significant revenue, yet requires relentless investment in compute, data centres, power, and depreciation, while competition and pricing pressure constrain how much of that revenue ultimately reaches the bottom line. There are echoes here of the airline industry, where an indispensable service can still be a difficult business if high capital costs and intense competition keep compressing margins. Frank Flight’s recent note – Tokenomics – makes an important point in this context…the future of AI adoption is unlikely to be a world in which every user, workflow, or enterprise application migrates toward the most compute-intensive frontier model. Instead, we are likely to see a more bifurcated market, where frontier AI remains highly valuable for a narrower set of firms and use cases that can monetise genuinely difficult problems at scale, whilst much of the broader economy adopts cheaper, simpler, and more efficient models that are ‘good enough’ to augment productivity without requiring frontier-level inference costs. To be clear, this does not mean the frontier is abandoned; it simply means the frontier may become less universal than the current narrative implies, concentrated among firms with the balance sheets, research depth, proprietary data, and operating domains to turn expensive inference into measurable economic returns. Ultimately, this matters for frontier labs, semis, and hyperscalers because current valuations are still being underwritten by exceedingly strong revenue growth and the expectation that AI adoption keeps scaling aggressively. So far, the maths work because the revenue trajectory has validated the capex cycle. But, if the end state for much of AI is more basic models, narrower frontier usage, and less ambitious enterprise adoption than the market currently assumes, then the new revenue path could undershoot – token optimisation, not tokenmaxing. In that scenario, valuations would begin to look much more stretched, not simply because multiples are high, but because forward earnings may be revised lower as growth disappoints and depreciation, infrastructure costs, and competitive pricing pressure become harder to absorb.

Model Adoption Rate: Share of U.S. businesses with paid subscriptions to AI models, platforms, and tools (Ramp AI Index)

Source: Ramp AI Index, data as of Jun-26

I foresee a more challenging time ahead for risk assets as these concerns collide with a Fed hiking cycle that could start as soon as September. Tightening episodes have a long history of taking the wind out of large equity bull markets, particularly when they arrive after a period in which investors have crowded around a single dominant growth theme and extrapolated its economics too far into the future. Historical parallels are never perfect, but the combination of an energy price shock, a powerful speculative narrative in equities, and a central bank forced to lean against inflation does bring to mind both 2000-01 and 1973-74, with the former offering the cleaner comparison on technology and valuations…and the latter providing the better analogy on oil, inflation, and policy constraint. In 2000-01, the internet was clearly transformative, but valuations reflected expectations that were simply too ambitious…too many companies, growing too quickly, earning returns that proved unsustainable. Once the Fed’s tightening, higher oil prices, and slowing growth began to bite, the gap between technological promise and near-term earnings reality became impossible to ignore, with the Nasdaq ultimately falling almost 80% from peak-to-trough and the broader market also suffering a very material drawdown. In 1973-74, the catalyst was less about a single technology theme and more about the collision of an oil shock, accelerating inflation, and a Fed that had limited room to support growth…though the lesson for equities was similar in the sense that rich starting valuations, rising input costs, and tighter financial conditions proved to be a toxic mix, with stocks falling by more than 45% during the bear market. The useful lesson across these episodes is that markets are usually most vulnerable when the secular story remains compelling, but the macro backdrop turns against the equity narrative at precisely the moment when valuations require continued earnings upgrades, benign discount rates, and investor willingness to look through near-term cyclicality. If AI revenue growth continues to validate this capex cycle, the market may be able to look through a lot of the pressure. This week’s blockbuster SpaceX IPO was a reminder of how powerful ideas (not just AI) combined with world-class engineering can generate tremendous enterprise value and shareholder enthusiasm. But…for the AI narrative itself…if the tokenmaxing splurge fades, frontier adoption proves narrower than expected, and forward earnings estimates start to come down just as oil prices and the Fed are tightening financial conditions, then the valuation cushion for AI-linked stocks and risk assets more broadly may prove much thinner than it currently appears.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/