By Thomas Sozzi

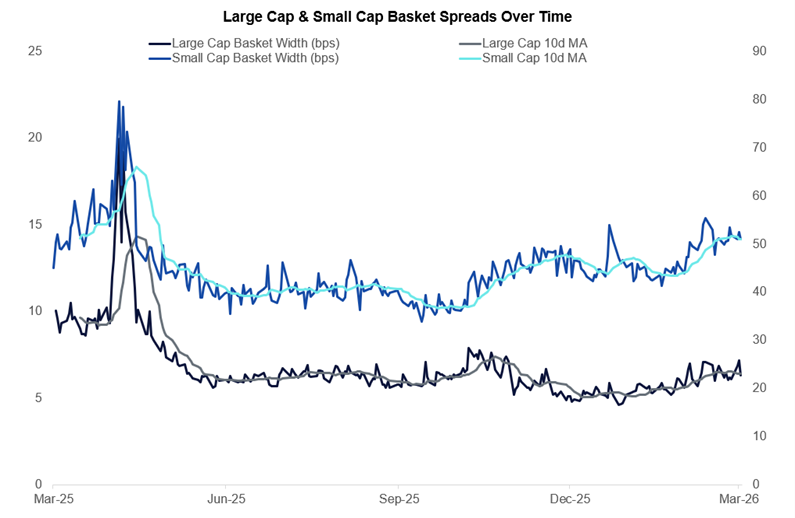

Basket Spreads Drift Wider Across Market Caps

Large cap index basket bid-ask spreads have pushed out to their widest levels since last October/November (currently in the 70th percentile over the past year), marking a notable deterioration in underlying liquidity conditions even as headline index levels continue to remain stable. The move in small cap basket spreads is even more striking, which are now sitting at their widest since the tariff-induced volatility spike last April (88th percentile over the past year). This underscores a sharper retrenchment in risk appetite and balance sheet deployment further down the market-cap spectrum.

Source: Citadel Securities internal data; as of 3/4/2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

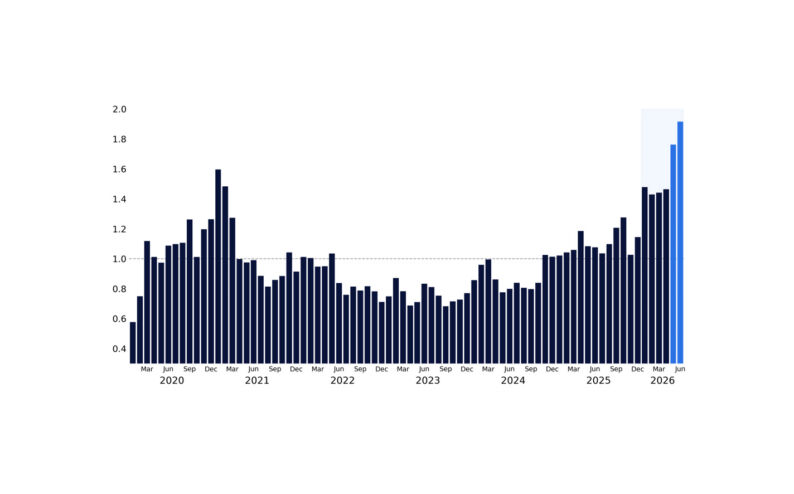

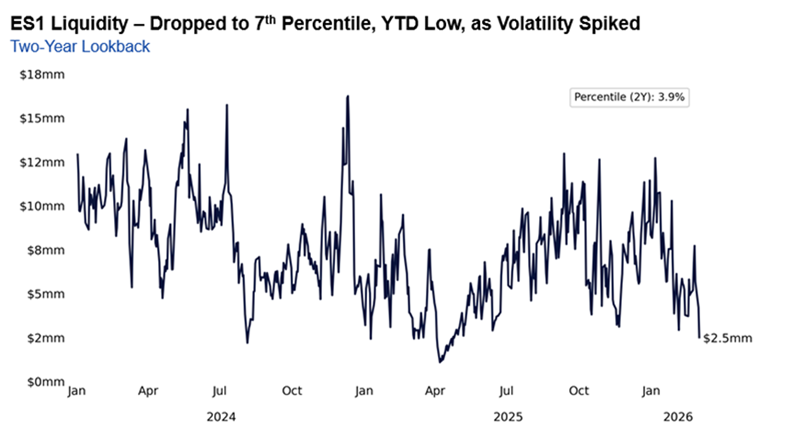

Futures Depth Falls to Two-Year Lows

Futures are signaling the same shift in liquidity conditions. As Scott Rubner, Head of Equity and Equity Derivatives Strategy, pointed out earlier this week, ES1 top of book liquidity has fallen to the 4th percentile in the past two years. With lower notional size existing on the touch, even modest directional flows could generate outsized impact.

Source: Bloomberg as compiled by Citadel Securities, GMI, as of March 3rd 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

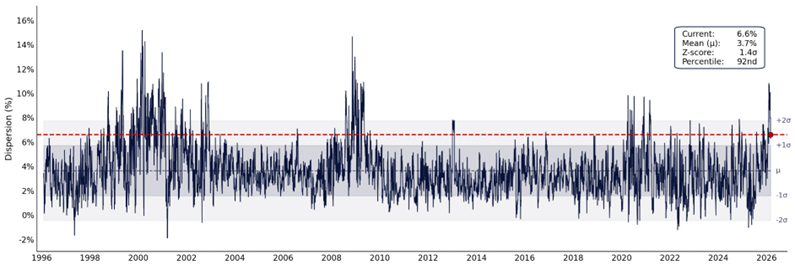

Index Calm Masks Elevated Single-Stock Dispersion

Our Global Market Intelligence team has also been highlighting that single-stock dispersion is at extreme levels. Over the past 30 days, the S&P 500 is down 1.5%, while the average stock in the index has moved 8.1% in absolute terms, placing the 6.6% dispersion spread in the 92nd percentile over the past three decades. One month ago, this spread surged to 10.8% – a 99th percentile event and a 3.5σ outlier over the past thirty years.

S&P 500 Dispersion – Still Elevated, But Off the Highs

Two-Year Lookback

Source: Bloomberg as compiled by Citadel Securities, GMI, as of March 4th 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

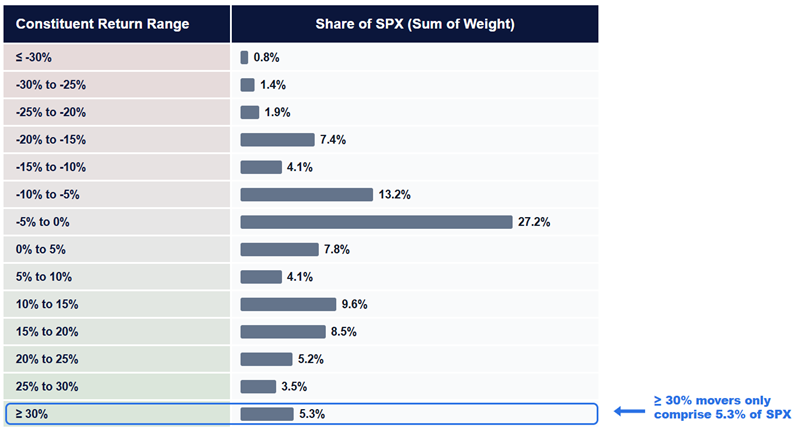

Beneath the surface, they also note that we have seen a much wider distribution of SPX constituent returns to start the year, however these moves are occurring in names with smaller index weights, limiting their contribution to headline performance, and masking the chaos under the hood.

SPX Constituent Returns – Extreme YTD Rallies Have Limited Index Contribution

Sum of Weight (%) Per Constituent Return Range

Source: Bloomberg as compiled by Citadel Securities, GMI, as of March 2th 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

Taken together, the signals we are seeing between 1) widening basket spreads, 2) depleted futures depth and 3) the stark contrast between relatively muted index-level volatility and elevated underlying constituent volatility points to a market that is simmering on the surface, but starting to boil underneath.

If an exogenous market shock were to occur and index-level price movement catches-up with the larger, underlying constituent moves we have witnessed, the recent deterioration in liquidity conditions could make the tape more vulnerable to sharp, flow-induced moves.

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/