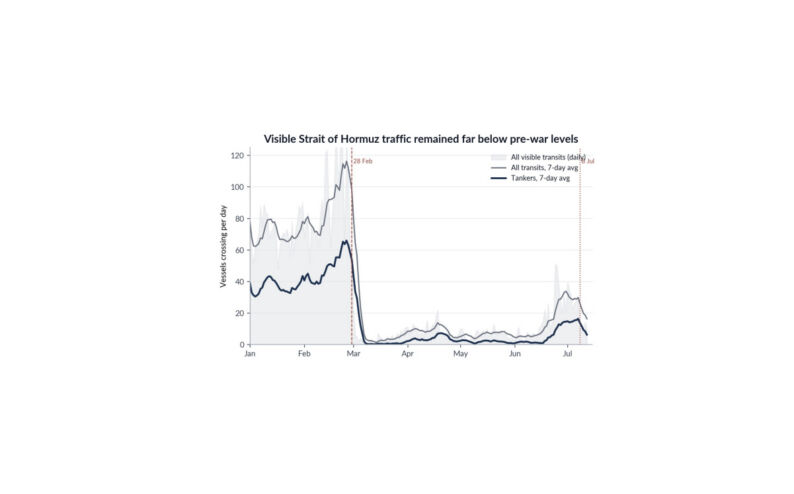

“A ROUTE TO RESOLUTION” WAS THE HEADLINE FROM THIS NOTE LAST WEEK…which outlined my out-of-consensus view that some sort of ceasefire was possible. As it turns out, events moved more quickly than even I expected. Whilst the situation remains tense, the intention from President Trump is clear: he is keen to bring an end to this war and seems satisfied with what it has achieved. Similarly, the Iranian regime survives, possibly with control of the Strait of Hormuz…their only remaining source of influence and power (perhaps much more important than nuclear weapons). The contours of what follows will become clearer in the coming weeks, but for markets, the most relevant point is that we appear to have substantially truncated the tail of the worst-case scenario. The US has made a deliberate turn toward de-escalation and has actively pushed for it through backchannel routes after largely achieving its objectives. China’s role in pushing Iran to agree to the ceasefire should not be underestimated here – whilst remaining outside of the military entanglement, it remains a strategic partner to Tehran, and reports suggest it has pushed for de-escalation. Ultimately, incentives for both the US and China (and much of Europe and Asia) are aligned in bringing an end to this conflict, given the already significant cost to their economies. Elevated gas prices across the US will take time to normalise and will no doubt have a negative effect on US consumer sentiment; equally, with around 10% of its oil supply constrained, China will be reluctant to further hinder efforts to revive economic growth, especially if the global economy tips into recession, a significant risk for its export-oriented model, leaving it exposed to further disruptions in global trade. We now have both superpowers pushing for a resolution and reopening of the Strait…and they have leverage over the other regional actors on either side of the conflict. My expectation is that despite numerous challenges, talks will extend to find some form of diplomatic solution with the Strait likely to fully reopen in due course. This remains the single-minded focus for markets.

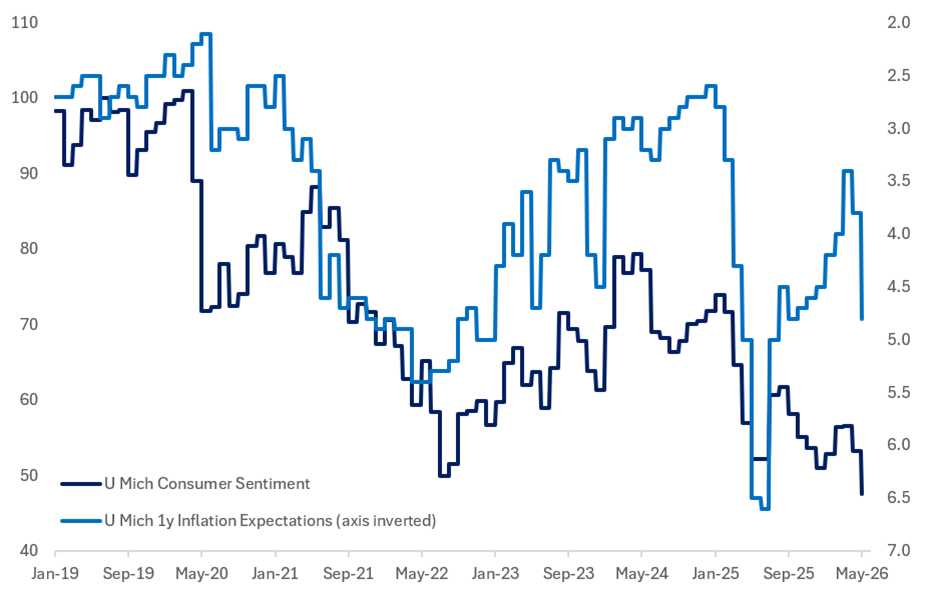

Source: Univ of Michigan Survey of Consumers

THE SIZEABLE TAIL RISK ASSOCIATED WITH WORST-CASE ESCALATION IS RECEDING…and forward-looking equity markets are responding as I had anticipated with a bullish turn – I expect this to continue. Energy markets will move from a phase of heightened volatility around different outcomes to one where natural gas and crude oil find new clearing prices. Reports suggest that cargoes of crude are still trading in the mid-$100s per barrel, and Forties Blend, one of the most liquid and heavily traded physical crude streams in the world, hitting ~$147 per barrel simply reflects the current realities on the ground. This will take time to recalibrate, and we cannot expect a full normalisation anytime soon. Most estimates are centred on mid-May/early-June as the first realistic time to see relief in physical markets, given the time lags associated with seaborne cargo. This likely means some central banks will end up hiking, with the inflation expectations channel remaining a concern…and we are likely to see at least a few months of elevated headline inflation. However, some will recognise that the probability of a worst-case scenario is lower, which should mean that a cautious response is warranted. I broadly expect ~2 hikes from the ECB, with the Fed and BoE likely to prefer remaining on hold. This is somewhat more dovish than current market expectations, so should be enough to support global front end yields. Moreover, there is a risk that the market responds to uncertainty-related declines in sentiment data, and that the impact of elevated gas prices drags down core retail sales in coming months. The key question is whether this will ultimately feed into hiring and investment decisions. I take some comfort in the stabilisation of FCI, largely driven by the bounce in equity markets… but if we do price a near-term growth hit, I expect that it will be most pronounced in fixed income markets, which tend to focus more on the spot data. Equities and rates can therefore rally together for now.

Source: Morning Consult

Legal Entities Disseminating this Material: This material is disseminated in the United Kingdom by Citadel Securities (Europe) Limited (“CSEL”) regulated by the Financial Conduct Authority (“FCA”) (Registered company number: 05462867); in the European Union by Citadel Securities GCS (Ireland) Limited (“CSGI”) and its Paris Branch regulated by the Central Bank of Ireland (“CBI”) (Registration Number: C173437); in Hong Kong by Citadel Securities (Hong Kong) Limited (“CDHK”) licensed by the Securities and Futures Commission of Hong Kong (“SFC”), in Japan by Citadel Securities Japan Co., Ltd (“CSJC”) registered as a Type 1 financial instruments business operator with the JFSA; and in the United States of America by Citadel Securities LLC (“CDRG”) registered with the Securities Exchange Commission (“SEC”) and Financial Industry Regulatory Authority (“FINRA”), Citadel Securities Institutional LLC (“CSIN”) registered with the SEC and FINRA or Citadel Securities Swap Dealer LLC (“CSSD”) registered with the SEC, Commodities Futures Trading Commission (“CFTC”), and National Futures Association (“NFA”). Unless governing law permits otherwise, you must contact a Citadel Securities entity in your home jurisdiction if you want to use our services in effecting a transaction in any financial instruments or securities, including derivatives.

FOR INSTITUTIONAL USE ONLY; FOR PROFESSIONAL CLIENTS AND ELIGIBLE COUNTERPARTIES ONLY. This material is not intended as and does not constitute investment research. Contents of this material will be strictly limited to non-specific, generic information (i.e. macro events/topics) and are not subject to the Markets in Financial Instruments directive (MiFID II) or FINRA research rules. This material does not constitute an offer, solicitation, invitation, or inducement to purchase, acquire, subscribe to, provide, or sell any financial instrument or otherwise engage in investment activity.

https://www.citadelsecurities.com/privacy/

Please see additional important disclosures, including disclosures that may be relevant to your country of residence or business at: https://www.citadelsecurities.com/disclosures/citadel-securities-fimm-sales-trading-disclosures/